開年受挫,特斯拉Q4業績能否扳回一城?

Futu Research | Tesla's 23Q4 Earnings Forecast: Gross Margin Is Expected to Remain Under Pressure

#睇業績用富途牛牛 #

I. Tesla's business concerns

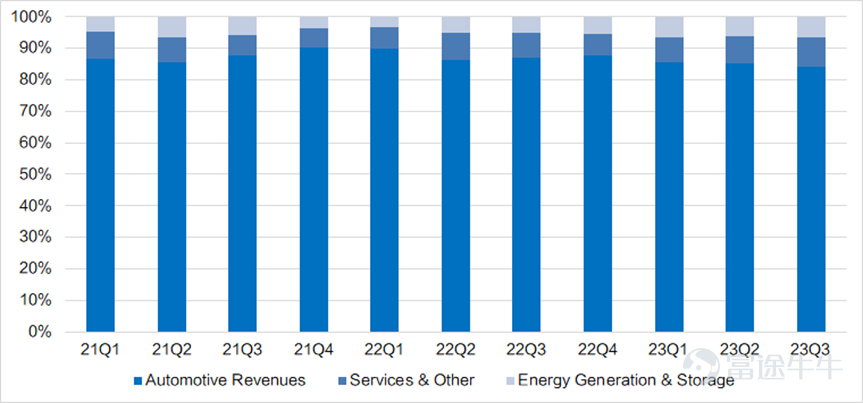

Tesla's business structure is mainly divided into three business divisions: automotive business, energy business, service, and others.

The automotive sector includes sales revenue from electric vehicles, rental revenue, and sales revenue from automobile supervision points;

Services and other departments include non-warranty after-sales service, paid charging services, used car sales, etc.

In terms of business revenue, electric vehicle sales and related automobile-related services account for more than 95% of revenue.

Tesla's other businesses, such as FSD, DOJO, and robotics, are very imaginative in the medium to long term, and have contributed a lot of valuation to Tesla, but electric vehicle sales are still the core basic market.

Figure: Tesla's main business revenue structure (%)

Source: Bloomberg, Futu Securities

The focus of Tesla's earnings report for this quarter is:

1) Revenue side: Since sales data for the fourth quarter have been released, the decisive factor in revenue will be changes in ASP bicycle revenue. Due to Tesla's different price adjustment strategies in each region in the fourth quarter, the final change in ASP determines whether revenue exceeded expectations.

2) Profit side: Gross margin is still the most concerned data. There were many factors affecting gross margin in the fourth quarter, both positive and negative. There is uncertainty about the actual performance of gross margin.

3) Target guidelines for 2024: This includes 2024 sales targets, Cybertruck production progress, plans for next-generation automotive platforms, etc.

II. Revenue growth is unlikely to exceed expectations

In the fourth quarter, Tesla's production and sales were slightly higher than expected, producing about 495,000 vehicles, and delivering more than 484,000 vehicles, up 11% from the previous month. This increased overall delivery volume in 2023 by 38% year-on-year to 1.81 million units, exceeding its previously set target of 1.8 million vehicles. Although the delivery volume reached a record high, unlike the previous performance, which greatly exceeded expectations, the fourth quarter had only just reached the target, and the market's response to this news was rather lackluster.

At the same time, the high sales volume in the fourth quarter was affected by some consumers buying cars in advance in order to enjoy tax breaks. Since January 2024, the new US battery purchase regulations have officially come into effect. This change has caused Tesla's all-wheel drive version of the Cybertruck and some Tesla Model 3 models to lose the $7,500 tax credit.

Figure: Tesla's quarterly sales volume (units)

Source: Bloomberg, Futu Securities

From the perspective of bicycle revenue, Tesla's bicycle revenue in the fourth quarter is expected to drop slightly from month to month due to the price reduction strategy. In the fourth quarter, Tesla implemented a price reduction strategy for the two main models, the Model 3 and Model Y, in the US. Starting in October, the starting price of the standard model 3 was lowered from the previous 40,400 US dollars to 389,900 US dollars, the starting price of the long battery life version fell from 47,400 US dollars to 459,900 US dollars, and the starting price of the high-performance version fell from 5324 million US dollars to 50999 million US dollars. However, the price increase implemented for the mainstream models of China's Model3 and ModelY played a partial hedging role, and the price increase was small (but the price was cut again in the first quarter).

Compared to Bloomberg's unanimous expectations, Tesla is expected to record revenue of 25.786 billion US dollars in the fourth quarter, up 6% year on year, of which automobile sales revenue is 20.86 billion US dollars, up 12% month-on-month, and Q4 sales increase 11.4% month-on-month. Due to the inconsistent direction of price adjustments in various regions, there is uncertainty about ASP. However, considering that the US region may drive more sales growth this quarter due to changes in tax policies, and at the same time, price cuts will be significant, overall, it is expected that ASP will remain flat or decline slightly from month to month. We believe it is unlikely that Tesla's revenue performance will exceed expectations.

Figure: Tesla Motorbike Revenue (USD 10,000)

Source: Bloomberg, Futu Securities

3. Gross margin is still under pressure

Over the past six quarters, Tesla's gross bicycle profit fell from $17,865 to $8,431, a drop of 53%; the gross profit margin of the automobile business (sales revenue without credit) continued to fall from 18.96% in 23Q1 to 16.33% in 23Q3. Overall gross margin at the company level continued to decline from 19.3% in 23Q1 to 17.9% in 23Q3.

Figure: Gross profit margin of the automobile business (without credit)

Source: Bloomberg, Futu Securities

Tesla's gross margin this quarter was affected by many positive and negative factors:

1) Price cuts for major models in the US - negative, significant

2) In terms of upstream raw material costs, lithium carbonate prices showed an overall downward trend in the fourth quarter — positive, slightly

3) Bicycle depreciation costs increased in the third quarter due to factory shutdowns, and normal production resumed in the fourth quarter — positive, slightly

4) Productivity increases at the Berlin and Texas plants — positive, slight

According to Bloomberg's unanimous forecast, Tesla's overall gross margin for 23Q4 is expected to be 18.09%, compared to 17.9% in the previous quarter. Although there are some favorable factors in this quarter, due to the negative impact of price cuts on gross margin, gross margin is expected to remain under pressure and will remain basically the same as the previous quarter or decline slightly.

IV. Continued risk factors in 2024

1) The competitive landscape is becoming fierce, and the market is concerned about Tesla brand fatigue and lack of new models

Tesla's two most important markets, the US and China, are all facing a worsening trend in the competitive landscape. In 23Q4, BYD sold 526,409 pure electric vehicles, more than 40,000 more than Tesla, officially surpassing Tesla to become the number one selling pure electric vehicle brand in the world.

In the Chinese market, the penetration rate of new energy vehicles in China has reached more than 30% in 2023, and the increase in the pure electric penetration rate has slowed sharply; Tesla's 200,000 to 400,000 middle and high-end price band is in the most competitive range. In '24, the new power brand China is planning to launch a variety of new models.

In the US market, the competitive landscape and penetration rate are slowly changing. Tesla still dominates the market share, but sales data for 2023 shows that established car companies that have transformed into new energy sources, such as Ford and GM, are making efforts to enter the electric vehicle market. Against the backdrop of Tesla's big price cuts last year, mainly hybrids seized Tesla's share. The future decline in Tesla's market share is a probable event.

Figure: Sales volume of electric vehicles of various brands in the US market, in millions

Source: Kelly Blue Book, Futu Securities

Competitors are coming aggressively. In comparison, although Tesla remodeled and upgraded the original model last year, there were few upgrades and changes, and no new explosion-level models were released in the short term. The Tesla brand's fatigue and lack of new models have caused the market to worry that under strong attacks by competitors, it may have an impact on Tesla demand.

2) Cancellation of tax benefits

The US introduced new electric vehicle subsidies in 2023, but the opposite happened in 2024, causing Tesla to lose the Model 3 SR and Model 3 LR subsidies. Germany's electric vehicle subsidy program was originally scheduled to last until the end of 2024, but it ended early at the beginning of this year. In 2023, driven by price cuts and increased subsidies in Europe and the US, the high base of sales growth made growth in 2024 more difficult.

3) Price cuts are expected to continue

At the beginning of the year, Tesla carried out a new round of price cuts in Europe and China. China lowered the price of the Model 3 and Model Y, from 259,900 yuan to 245,900 yuan (RMB); the price of the Model 3 long-range version was reduced by 11,500 yuan to 285,900 yuan (RMB); the model Y rear-wheel drive version was reduced by around 6%; the Model Y rear-wheel drive version was reduced by 7,500 yuan to 258,900 yuan (RMB), a reduction ratio of about 3%.

In Europe, Tesla also cut prices in Germany, France, and the Netherlands due to the reduction in subsidies. Among them, the German long-range version and high-performance Model Y were reduced by 9% and 8.1%, respectively. Although Tesla hasn't officially cut prices in the US, almost all of Tesla's inventory is discounted by 10% or more.

As Tesla's supply increases and prices drop, the value of Tesla's used cars depreciates faster than rival cars, and the used car market will in turn affect demand for new cars.

Figure: Tesla used car price trends

Source: CarGurus, Futu Securities

This means that the 2024 price war is expected to continue, and pressure on ASP and gross margin will continue. Cybertruck's delivery in 2024 will have a further negative impact on gross margin, as Cybertruck's cash flow will be negative for the next 18 months.

4) Increased labor costs

After the American auto trade union defeated the top three automakers last year, the three major US automakers raised employees' wages by 25%. Under pressure from peers, Tesla also announced wage increases for all American production workers, increasing workers' wages by about 10% (there may be a second salary increase in the future, and the final salary increase is still uncertain). Tesla has around 130,000 employees worldwide, about half of which are in the US. Rising labor costs will have a negative impact on Tesla's gross margin in 2024.

Other short-term risk factors include: the Red Sea attack caused the Berlin Gigafactory to suspend production for two weeks, Hertz cancels orders, and Musk's dispute over voting rights.

4. Valuation pressure is high

In summary, we believe that Tesla's revenue performance is unlikely to exceed expectations, gross margin is under pressure, and there is great uncertainty about the stock price performance after the earnings report.From a valuation perspective, as of 23Q3, Tesla achieved free cash flow of 2.3 billion US dollars and net profit of 7.1 billion US dollars in the first three quarters. Taking into account the increase in sales in the fourth quarter but under pressure on profits, it is estimated that net profit of US$9.1 billion and free cash flow of US$3.2 billion will be achieved for the full year of 2023. As of January 22, 2024, Tesla's current valuation is US$663.7 billion, excluding the impact of cash, realizable assets, and interest-bearing liabilities. The current valuation is equivalent to 70 times 2023 net profit and more than 200 times free cash flow in 2023, which is a high valuation.

Tesla has many risk factors that suppress revenue and profits in 2024. Its guidelines are not optimistic. The possibility that next year's growth can quickly absorb overvaluation is relatively low. Until these risk factors are clarified, it is difficult to lift the suppression of its valuation. In the short term, without the performance support of core tram sales, imaginative businesses such as AI, FSD (Robotaxi), Dojo, and Optimus will also be difficult to monetize and value.

So what are the factors that will help reverse Tesla's current predicament in the medium term?

1) The launch of next-generation production platforms and economical models: Judging from the information currently circulating from Tesla, after the new platform is put into operation, the production cost of vehicles will be drastically reduced, so that Tesla will no longer fall into a gross margin situation. It is also possible that Tesla models under 200,000 will come out, and the introduction of a falling price band will be Tesla's next driving force for performance growth.

2) Cybertruck's production increase exceeded expectations: Musk previously cut Cybertruck's sales expectations, which were affected by 4680 battery production capacity, and delivery volume was limited until production capacity was expanded in 2024. It is estimated that 250,000 vehicles may only be delivered in 2025. Cybertruck's halo effect is sufficient, and the reservation volume is impressive. Currently, it is mainly limited by insufficient production capacity. Judging from US model sales in 2022, half of the top 10 sales models are pickups, and there is a large demand space. For example, delivery exceeding expectations in 24 years will be an effective path driven by performance.

3) Massive growth of FSD users: Tesla's leading edge in the field of intelligent driving is still obvious. FSD driving distance is growing rapidly. It has already exceeded 500 million miles in the third quarter. Combined with sales advantages, it has accumulated a large amount of data that can be used for training. According to the news, Tesla's FSD will soon be launched in China. The price is about 64,000 yuan (RMB), which is twice that of the EAP.

In the long run, over time, Tesla's many new businesses to be monetized are expected to gradually be implemented, and Tesla's business model will also become more and more diverse. Coupled with Musk's strong topicality, Tesla's current predicament needs to wait for more catalysts to be realized.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

38

53