台積電Q4業績超預期,績後走勢你點睇?

Futu Research | TSMC Earnings Review: Performance Recovery Is Worth Expecting

#睇業績用富途牛牛 #

On January 18, 2024, TSMC released its 23-year Q4 earnings report. Both revenue and net profit exceeded Bloomberg's unanimous expectations. 23Q4 achieved revenue of NT$625.5 billion (US$19.62 billion), down 20% year on year, up 13% month on month, exceeding market expectations of NT$618.3 billion; net profit of NT$238.7 billion (US$7.49 billion), down 19% year on year, but up 13% month-on-month, exceeding market expectations of NT$224.13 billion.

Currently, there are two things that the market is most concerned about TSMC:

First, how is TSMC's performance recovery progress. This is mainly affected by the recovery in consumer electronics and the continued demand for AI;

The second is the progress of the commissioning of TSMC's production capacity, particularly advanced process production capacity;

1. Has TSMC confirmed that it has passed the “bottom of performance”?

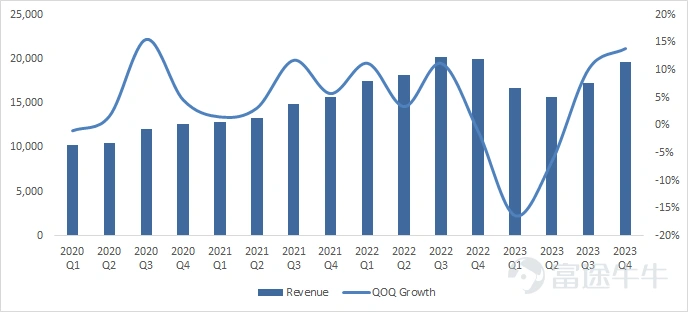

On the revenue side, TSMC's revenue has rebounded for two consecutive quarters since it bottomed out in Q2 in '23. This quarter's revenue increased 13% month-on-month, further accelerating from the previous quarter. Foundry industry revenue for the full year of 2023 fell 13% year on year, TSMC's annual revenue fell 9% year on year, and TSMC continued to outperform the industry level.

So what is driving TSMC's performance recovery this quarter?

Figure: TSMC's quarterly revenue and month-on-month growth rate (million US dollars)

Data source: Bloomberg, Futu Securities

Smartphones and high-performance computing HPC are TSMC's biggest revenue sources. Together, they account for more than 80%. Among them, HPC mainly includes AI requirements such as graphics cards and data centers.Over the past four quarters, due to strong demand for AI and the relative downturn in the mobile phone market, HPC continued to surpass mobile phones.

However, we can see from changes in the revenue structure this quarter that the share of high-performance computing was relatively stable this quarter, while the share of revenue contributed by smartphones rose rapidly to 43% from 39% in the previous quarter, increasing 27% month-on-month.

Figure: 23Q4 TSMC's revenue share and growth rate by industry

Data source: Company announcement, Futu Securities

TSMC's largest customers include Qualcomm and Apple, and revenue is closely related to the demand in the mobile phone market.According to Canalys data, the global smartphone market grew 8% in the fourth quarter of 2023, ending seven consecutive quarters of decline and beginning a steady recovery. Apple released the new iPhone 15 in the third quarter, contributing to more revenue growth.

Despite being affected by negative factors such as increased competition, Apple's sales performance was still good last year, driven by price reduction promotions. In 2023, iPhones shipped close to 235 million units, surpassing Samsung to become the number one mobile phone brand in the world.

This shows that with the gradual recovery of consumer electronics, the main driving force for TSMC's revenue growth is beginning to be driven by AI-driven HPC demand to be driven by both AI and smartphones. We believe that with the elimination of inventory in the consumer electronics industry chain, orders from the company's mobile phone customers are expected to continue to pick up in the coming quarter.

Figure: Global smartphone shipments in the current quarter (million units)

Data source: Wind, Futu Securities

2. Structural changes in advanced manufacturing processes have brought about a marked increase in average price

We further split revenue in terms of shipment volume and single-wafer revenue:

1) Judging from the shipment performance, TSMC's wafer shipments in 2023Q4 were 2,957 thousand wafers, an increase of 1.9% over the previous month. The increase in shipment volume has also led to an increase in inventory turnover. The number of inventory turnover days in the current quarter dropped from 96 days in the previous quarter to 85 days.

As demand for incremental advanced packaging brought about by AI chips continues to be strong, production of the first fab in Arizona was delayed until the first half of 2025 due to lack of skilled labor and high costs.The current situation is that production capacity is still unable to meet strong customer demand, and the shortage of supply may continue until 2025.

Figure: TSMC's Shipments (Thousand Tablets) vs. Single Wafer Revenue (USD)

Data source: Bloomberg, Futu Securities

2) Looking at single-wafer revenue, Q4 single-wafer revenue continued to rise to $6,651, up 12% month-on-month and 23% year-on-year, increasing for 16 consecutive quarters.

The increase in unit prices is related to changes in the process structure, and TSMC's advanced process revenue is still the company's biggest source of revenue.Specifically, 3nm's share of revenue increased significantly this quarter, mainly due to the seasonal release of new Apple models. Currently, 3nm is only the iPhone A17Pro/M3 Mac; while 7nm is mainly due to the release of AI and other demand, which has increased the demand for 7nm processes.

Figure: TSMC's operating revenue by process (NT$1 billion) and share

Data source: Company announcement, Futu Securities

3. Gross margin pressure still exists

Despite the unit price increase driving gross margin, TSMC's gross margin fell to 53% month-on-month. This gross margin performance was unsurprising, and was basically in line with the market's previous forecast of 51.5%-53.5%.

The decline in gross margin was mainly due to the increase in depreciation amortization driven by mass production of 3nm. Depreciation and amortization expenses increased month-on-month in the current quarter, which in turn increased the company's fixed unit costs.

Figure: TSMC's quarterly gross profit (million dollars) and gross profit margin

Data source: Bloomberg, Futu Securities

Looking at the capital expenditure situation, TSMC's capital expenditure for the fourth quarter was US$5.24 billion. Under weak overall demand, capital expenditure for the quarter continued to decline. The capital expenditure in 2023 was US$30.45 billion, below the guideline value of US$32 billion. The main reason was that the company made appropriate adjustments based on the market environment; the reduction in capital expenditure led to a significant recovery in free cash flow in the fourth quarter.

Figure: TSMC's free cash flow (NT$ billion)

Data source: Company announcement, Futu Securities

4. So what is the return on investing in TSMC?

We calculate TSMC's return on investment based on “EPS growth* valuation+shareholder return”:

1) EPS growth: split from the two dimensions of quantity and price

In terms of average price, benefiting from structural improvements in advanced manufacturing processes below 7nm, the year-on-year average price increases in the Q1-Q4 quarter were 12%, 12%, 17%, and 23%, respectively. We expect this trend to continue in 2024, and conservatively anticipate that the average price per wafer will continue to increase by 10% in 2024 for the following reasons:

① With the upcoming launch of N3E, N3P, and N3X of the N3 series (loose N3E to reduce costs, N3P to enhance performance and chip density, and N3X with higher voltage tolerance), 3nm is expected to increase by more than 2 times year-on-year in 2024 (6% revenue share in 2023), and 3nm's revenue share is expected to rise to double digits.

② Demand for AI remains strong. The company expects the long-term CAGR of AI-related sales to be around 50%, which will lead to an increase in demand for 5nm and 7nm. Production capacity for high-performance computing is also expected to shift from 7nm to 5nm. 2nm is scheduled to begin mass production in 2025, and 2nm process technology will help TSMC seize future AI-related opportunities.

In terms of production capacity, we look at it from both the demand side and the supply side. On the demand side, growth in 24Q1 will be mainly driven by HPC due to seasonal decline in mobile phones, but it is expected that demand for mobile phones will resume growth throughout the year.

Judging from the company's supply capacity, although the company's current production capacity is still unable to meet demand, the shipment volume level in the latest quarter shows that production capacity has declined sequentially for 4 consecutive quarters, showing signs of gradual increase. Shipments are expected to continue to increase in the future as production lines continue to be put into operation (Tainan N3 Fab production expands; the Japanese production line targets the 12/16/22/28nm process and is expected to be mass-produced in 24Q4; the production line in Arizona in the US is expected to mass-produce 4nm chips at 25H1; mass production of 2nm is planned to begin in 2025).

According to Gartner's forecast, the number of wafer shipments in 2024 will increase 15% year over year. We conservatively estimate TSMC's 2024 shipment volume level based on an average 15% increase in the industry's shipments.

However, profit margins are still being suppressed by the expansion of production capacity. According to the company's guidance, capital expenditure in 2024 is expected to be US$28.32 billion, the median value is the same as the previous year, and 70-80% will be spent on advanced technology. This means that as future capital expenditure increases and 3nm mass production rises, depreciation and amortization will continue to affect the company's gross profit margin to a certain extent, but the company's leading edge in wafer manufacturing will also expand further.

Judging from the company's guidelines, gross margin for 24Q1 is expected to remain low at 52%-54%, indicating that investment in mass production and capital expenses will continue to put some pressure on the company's profit side. Gross margin is expected to drop slightly to 52% in 2024.

Based on the above assumptions, it is expected that in 2024, TSMC will enter a performance repair track of increasing volume and price, driven by demand for AI high-performance computing and rising average prices. It is expected that in 2024, revenue will increase 27%, and net profit will grow to US$32.4 billion, an increase of 20% over the previous year.

2) Shareholder returns

TSMC paid a total of US$9.35 billion in dividends in 2023, with a dividend return of around 1.6%. The cash flow from free activities in 2023 was NT$292.15 billion, or US$9.25 billion, which is equivalent to using all of the free cash flow in 2023 as dividends.

TSMC has increased its capital expenditure significantly in the past few years, but now it has moved to a stable stage. Dividends are expected to grow steadily in the future as cash flow improves. Since TSMC raised its dividend per share from NT$3 to NT$3.5 per share in the third quarter of 2023, this means that the cash dividend will increase by at least 20% in 2024, and the dividend return will increase from 1.6% to 1.9%.

Overall, TSMC's earnings report once again confirms the semiconductor industry's recovery, while also showing signs that AI demand has been strong for a long time.

3) Finally, let's take a look at how the company is valued?

As of January 19, 2024, TSMC's market value was US$586.2 billion, and PE (TTM) was 22x. Assuming there is no change in valuation, investing in TSMC means a return of at least 22% (EPS growth of 20% +2% shareholder return). The current valuation corresponds to 18x the 2024 net profit. If the impact of realizable assets and liabilities is deducted, the current valuation corresponds to 16x the 2024 net profit. If shareholder returns continue to rise in the future and profit margins are higher than expected, there is room for further correction in the valuation. However, it should be noted that there are risk factors such as geopolitical risks, the expansion of production capacity by competitors such as Samsung and Intel, advanced process conversion falling short of expectations, and delays in starting production lines.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

14

9