Futu Research | Netflix (NFLX.O) 23Q4 Outlook: Rapid growth in advertising monthly active users, optimistic about Q4 subscriber growth.

#Check earnings with Futubull#

$Netflix (NFLX.US)$Will release the 23Q4 financial report after the market closes on January 23, 2024, Eastern Time, How should we interpret this financial report?

1. Two key factors in Netflix's performance prediction: subscribers and ARM.

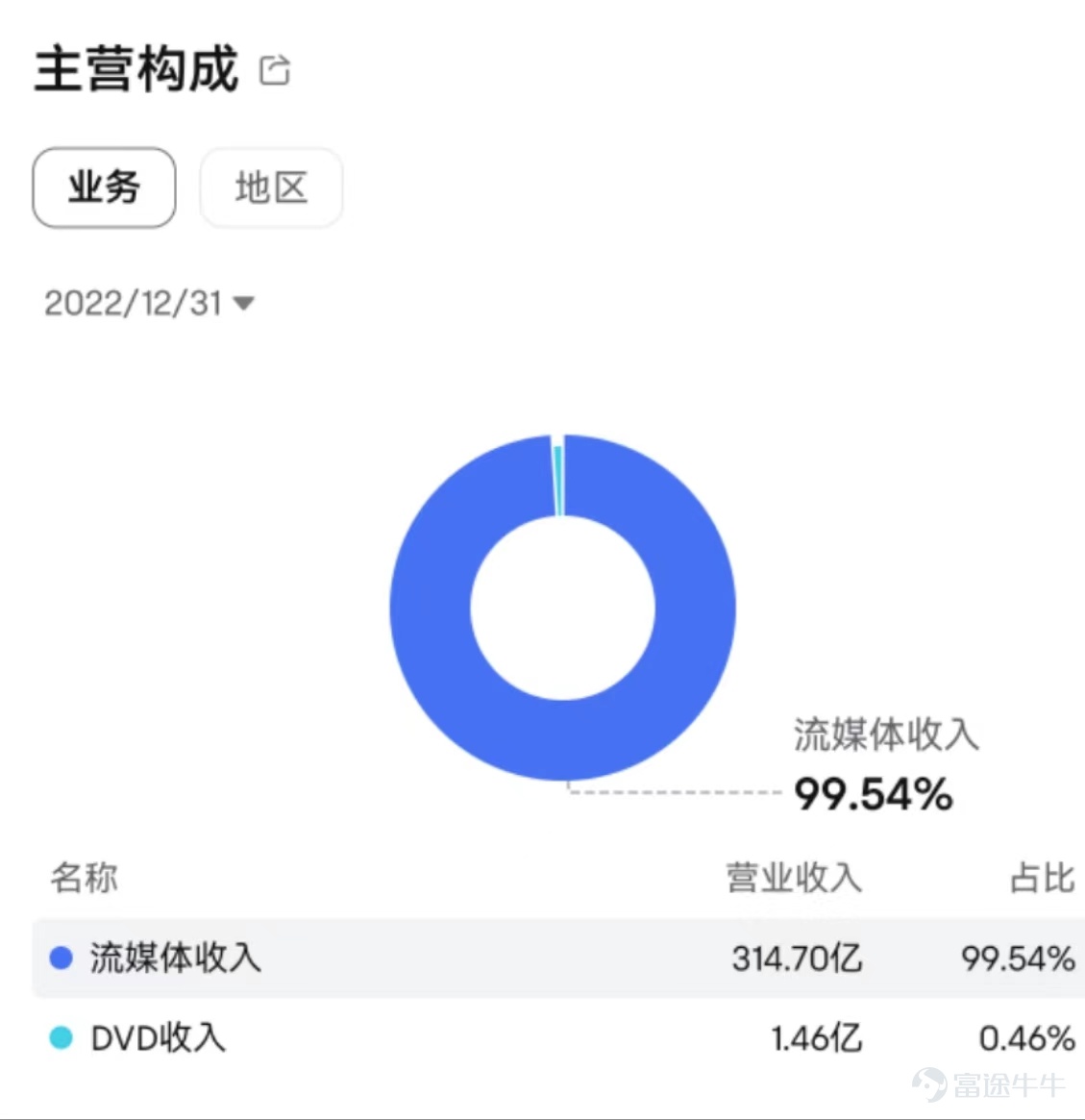

Netflix is the world's largest streaming media company, with streaming media subscription revenue as its main business income, accounting for as high as 99.54% of total revenue, while other DVD income can be almost ignored.

The streaming media industry is primarily driven by content, and high-quality video content is the fundamental guarantee for the company's growth. Under the principle that content is king, the growth of subscribers and ARM (revenue per subscriber) will become the main drivers of the company's performance growth.

Figure: Composition of the main business

Data source: Futubull

Therefore, for Netflix, the key to predicting performance is to track the growth of subscribers and ARM.

2. Where is the driving force behind the company's new user growth?

The company currently promotes the growth of subscribers through two main methods:

(1) Continuously cracking down on shared accounts.

(2) Attracting new users to subscribe through low-priced advertising packages.

The company expects the number of new subscribers in Q4 to be basically the same as Q3's 8.76 million. Considering the effectiveness of continuously combating paid shared accounts, the strong season for content in the fourth quarter, and the optimistic performance of advertising package subscription user data, we expect:

The company is expected to exceed expectations in new subscriber additions in the fourth quarter.

The logic for exceeding expectations in new subscriber additions can be inferred as follows:

(1) Continuous promotion of paid sharing has driven user growth.From the current data, there are very few users who unsubscribe due to crackdowns on shared accounts, with some shared accounts directly converting to full-paying users, demonstrating very good user stickiness and high retention rates. According to data disclosed by the company in early 2023, there are as many as 0.1 billion shared accounts globally, including 30 million users in the USA and Canada. It is estimated that 50% of shared accounts will become paid sharing users or full-paying users.

Currently, the company is still implementing a phased approach to promote paid sharing policies, with expectations that some users will gradually convert to full-paying users or additional paying users in the following quarters, considering the strong content in the fourth quarter as a good conversion opportunity.

(2) Rapid growth in advertising paid users.According to the company's latest data, the monthly active users of advertising members at the beginning of 2024 has exceeded 23 million, with a growth of 8 million in less than 3 months, accelerating growth. Advertising members were launched in 12 markets including the USA in November 2022, with 15 million monthly active users in November last year, and 5 million in May last year. Within the advertising members, 85% of users watch for more than two hours daily. Considering the 23 million MAUs disclosed in January 2024 (which may convert to 9.2 million to 11.5 million subscribers), we expect the end of 2023 advertising layer subscribers to reach 10 million.

Diagram: Growth of advertising paid users

Source of information: Company's official website

Can the company's ARM achieve growth in the fourth quarter?

The company's ARM was under pressure in the third quarter.In Q3 2023, the company's ARM declined by 1% year-on-year and 6.5% quarter-on-quarter, mainly due to the company's lack of price increases this year. Additionally, the majority of new users come from regions with relatively low subscription prices, and an increase in low-priced advertising package users has to some extent hindered ARM growth.

It is expected that ARM will remain flat year-on-year in the fourth quarter.Although the company announced in the third quarter a price increase of about 10%-20% for basic and premium member packages in certain regions of the USA, UK, and France, considering the relatively small coverage area and the increase in the proportion of advertising packages which will reduce part of the ARM, it is expected that the price increase will help alleviate the downward pressure on ARM. However, the impact on ARM improvement in the fourth quarter is limited.

Therefore, our determination regarding ARM is largely in line with the company's guidance. It is expected that ARM will remain roughly flat year-on-year in the fourth quarter, with the company's fourth-quarter revenue continuing to be mainly driven by user growth.

Figure: Member package pricing

Source of information: Company's official website

Fourth, the company is expected to perform well in Q4 2023, but the stock price has already partially absorbed some of the growth expectations.

The company's revenue is expected to exceed expectations.The company's guidance for Q4 2023 expects revenue to increase by 11% to $8.7 billion, with Bloomberg consensus at 10.8%. Considering the strong content lineup in Q4 and the effective crackdown on shared accounts, the number of new users is expected to further increase. Additionally, pricing strategies will effectively alleviate the pressure on ARM. The company is expected to exceed revenue expectations.

The company's operating margin is steadily expanding, and annual cash flow for 2023 is expected to increase to $6.5 billion.The company expects an operating margin of 20% in 2023. Reduced content expenditure due to strikes will drive FCF to reach $6.5 billion. By 2024, the company expects cash content expenditure to reach $17 billion, and the operating margin to expand to 22%-23%.

In terms of valuation, calculations indicate that the free cash flow in 2025 corresponds to a current stock price of 27.4x, and net income in 2025 corresponds to a current stock price of 24.5x. The current stock price has risen to a reasonable valuation level, essentially pre-digesting the Q4 performance growth.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

8

9