Futu Research | Where is Meituan's maximum valuation?

As of January 4, 2024,$MEITUAN-W (03690.HK)$the market value hit a new historic low, with a total market cap of 484.25 billion Hong Kong dollars (443.3 billion RMB).

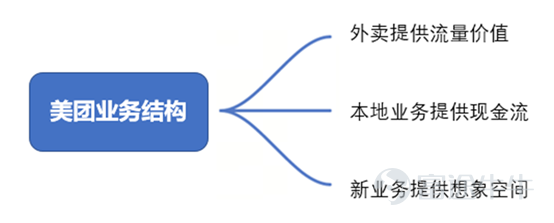

From Meituan's current profit model, it is mainly divided into two divisions: core local business and new business.

(1) The core local business sector mainly includes dining delivery, in-store hospitality, as well as Meituan Flash Purchase, homestays, and ticketing.

(2) The new business sectors mainly include Meituan Selected, Meituan Buy Vegetables, dining supply chain (Quick Donkey), online car-hailing, bike sharing, electric bike sharing, power bank, restaurant management system, and many other new business layouts by the company.

As the company's core business, the takeaway business provides traffic value; the profit margin of the home delivery business such as hotel and travel is relatively high, providing cash flow; the new business sectors are immature and mainly provide room for imagination; the core local commercial subsidies compensate for the losses of new businesses.

Figure: Meituan's business structure

Is Meituan currently expensive?

Looking at the balance sheet, Meituan has ample cash on hand. As of Q3 2023, cash and cash equivalents and investment-related financial products have reached 167.1 billion yuan, with interest-bearing liabilities of 22.4 billion yuan. Without considering other realizable assets, Meituan's "market cap - cash and equivalents + interest-bearing liabilities" is approximately 298.3 billion yuan.

As of Q3 2023, Meituan achieved operating cash flows of 8.1 billion yuan, 10.9 billion yuan, and 112 billion yuan for Q1 to Q3, respectively. A conservative estimate of operating cash flows for Q4 is around 10 billion yuan, and the total annual operating cash flow is expected to be around 40 billion yuan. Investment cash flows are mainly used for financial expenditures, and there is limited capital expenditure. In the first half of the year, only 2 billion yuan was used for capital expenditures such as purchasing factories and property equipment. Based on this calculation, the current market cap of Meituan corresponds to a free cash flow multiple of about 8.3x. If all liabilities are taken into account, the corresponding free cash flow multiple is around 11x. Overall, this valuation is very cheap. However, due to the significant discount in valuations of other internet companies and the unfavorable market environment, Meituan's valuation is not considered very low compared to other internet companies.

What is Meituan's future valuation trend?

(1) Quickly boosting shareholder returns can have an immediate impact on valuation support.

Previously, Meituan announced that starting from December 1, 2023, it will occasionally repurchase the company's shares in the public market for an amount not exceeding 1 billion US dollars. Based on a market value of 443.5 billion RMB, the above USD 1 billion repurchase plan is approximately 1.6% of the current market value. In the current environment with a 10-year US Treasury bond yield of around 3.9%, compared to the repurchase scale of Alibaba and Tencent, the return to shareholders from Meituan's repurchase is limited, making it difficult to support the current valuation.

(2) The growth of overall profit/earnings per share (EPS) will determine the long-term valuation central level.

Meituan maintained an aggressive stance in the third quarter, shifting from cost reduction to growth in order to cope with competition from platforms such as Douyin in the local life sector. However, the increased cost input also led to a decline in profits. The third-quarter revenue increased by 12.5% compared to the second quarter, but both operating surplus and profit margin declined compared to the previous quarter (profit margin dropped from 6.9% in Q2 to 4.4%). The uncertainty of how the competition with Douyin will evolve in the future, as well as the narrowing losses from new business operations, but the absolute scale of operating losses is still 5.11 billion yuan. In the short term, the unclear timing of turning losses around and whether two solid financial reports can restore market confidence will determine the central level of valuation.

Therefore, the current core trading logic that investors are focusing on for Meituan needs to pay attention to whether the 'return to shareholders' has improved and whether the 'competitive landscape' can be stabilized. This will be crucial in determining the short-term and long-term valuation of Meituan.

Risk reminder:The above valuation logic only applies to very pessimistic overall valuation conditions. When the market environment rapidly improves and the overall valuation quickly increases, the above valuation logic may no longer apply.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (21)

to post a comment

33

53