車市「價格戰」 硝煙再起,你怎麼看?

A new round of price war: why is it starting? When will it end?

A new round of price war begins again. When can it end?

Since entering August, many car companies have begun a new round of price war. First, the ID3 promotion continued until the end of August, then SAIC Volkswagen announced a collective price reduction of 9 SUVs, reaching a maximum drop of 60,000 yuan. Then, the “price killer” Zero Run announced that the price of pure electric models would be reduced by up to 20,000 yuan. Euler also followed suit. The price of the 2023 Good Cat and Good Cat GT was reduced by 22,000 yuan, then Hezhong Auto announced that the price of the 2024 Nacha S would be reduced by 49,000 yuan.

August 9, BYD$BYD Company Limited (002594.SZ)$After the press conference for 5 million new energy vehicles, promotional offers ranging from 3000-8,000 yuan were also launched in a low-key manner, further reducing the 99,800 yuan Qin Plus price to 96,800 yuan.

On August 11, Extreme Krypton suddenly officially announced that the price of Extreme Krypton 001 was reduced by 3-37,000 yuan, and the price was adjusted to 269-349,000 yuan.

August 14, Tesla$Tesla (TSLA.US)$It was announced that the starting prices of the long-life and high-performance versions of the Model Y were reduced by 14,000 yuan, starting at 299,900 yuan and 349,900 yuan respectively. Meanwhile, Model 3 introduced a limited time insurance subsidy of 8,000 yuan.

At a time when the two new energy giants, BYD and Tesla, are also adjusting prices, is a new round of price war in the automobile market about to begin?

Today, let's take a different look at why the price war will definitely start again and when it can end.

01

The goals at the beginning of the year were aggressive

The reality is too skitty

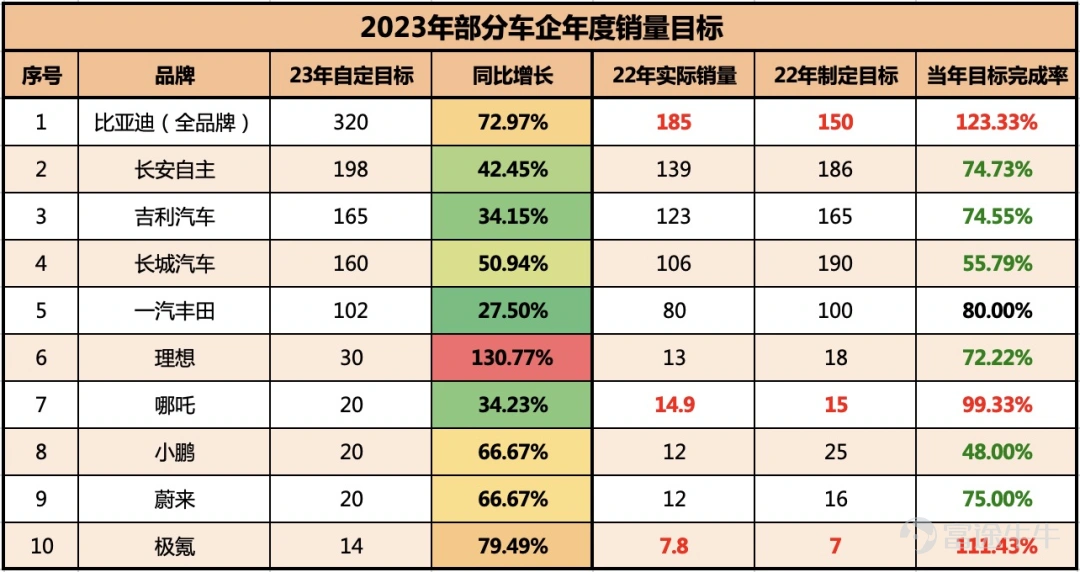

In 2023, at the beginning of the year, major car companies took the courage to increase sales in 2022 and set aggressive sales targets for 2023.

According to the author's incomplete statistics, the sales target of the 10 brands has already exceeded 10 million units, which can account for 50% of the 20 million annual sales volume, and this does not include the sales volume of many traditional brands such as Volkswagen and Honda.

Data source: Publicity of various car companies and collated by the data authors of the Passenger Transport Association

Among them, BYD's sales target is the highest at 3.2 million units, an increase of 72.97% over last year's actual target; Changan's own-brand sales target is 1.8 million units, up 42.45% year-on-year from last year's actual completion; Geely's 1.65 million units, up 34.15% year-on-year from last year's actual completion; and Great Wall Motor's target is 1.6 million units, an increase of 50.94% over last year's actual target. FAW-Toyota's target is 1.02 million vehicles, an increase of 27.50% over last year. This growth target is already the slowest growth target currently counted.

Most importantly,The target achievement rate of many brands in 2022 is already less than 80%, yet they still have to achieve a year-on-year increase of more than 50% in 2023, reflecting their very optimistic expectations. We can also see this kind of situation in 2017 or early 2018.

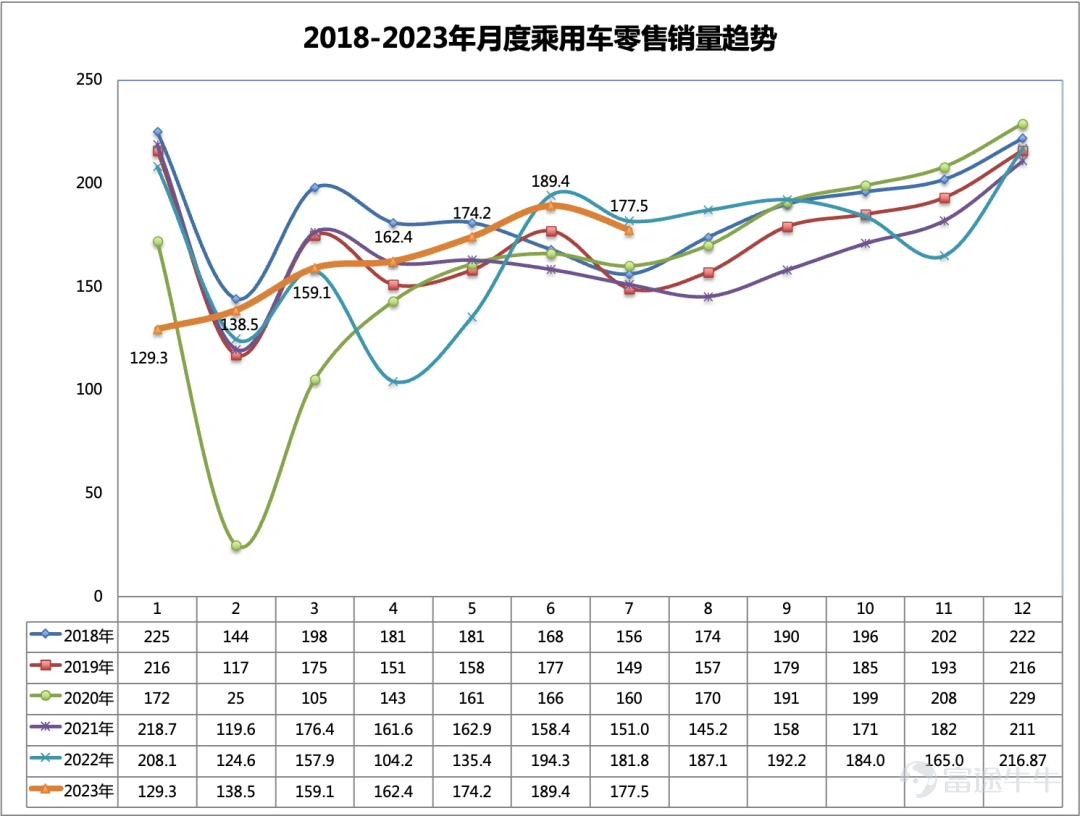

But the market is cruel,The passenger car market's performance this year fell far short of expectations, not even as good as some of the years affected by the pandemic. According to data from the Passenger Transport Association, passenger car retail sales volume from January to July 2023 was 11.304 million units, an increase of only 2.18% over the previous year. You need to know that in April-May 2022, passenger car sales fell sharply due to the epidemic.

Data source: Cartographic by Ride Federation authors

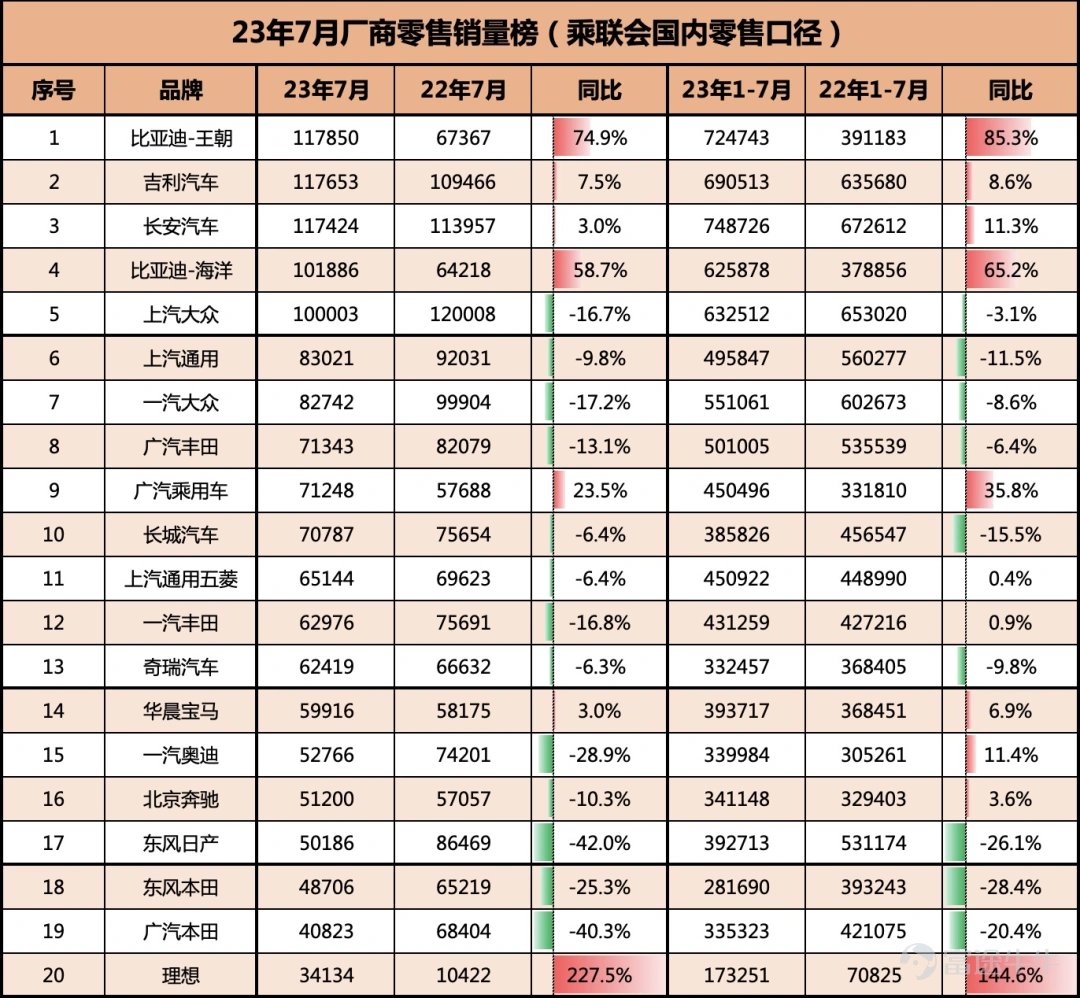

Most brands were too aggressive in setting goals at the beginning of the year, and at the same time, they were also affected by the first round of the price war driven by Tesla's sudden price cuts at the beginning of the year.In January-July of this year, sales of many brands not only did not increase, but the decline accelerated. Among them, the most obvious decline was among several Japanese brands. Dongfeng Honda fell 28.4% year on year, Guangqi Honda fell 20.4% year on year, and Dongfeng Nissan fell 26.1% year on year. Great Wall Motor, down 15.5% year on year, SAIC-GM fell 11.5% year on year. Even Volkswagen, which has remained stable for many years, experienced a year-on-year decline. Among them, FAW Volkswagen (excluding Audi) fell 8.6% year on year, and SAIC Volkswagen fell 3.1% year on year.

Data source: Collated by the author of the Ride Federation

By the end of July, when they see this kind of data, let's not say that the executives of each brand will start to worry; even if any ordinary reader sees the data, they also need to know what will happen — price reduction is the easiest, most direct, and most effective method.

02

The target completion rate is too low

Price cuts are needed to guarantee performance

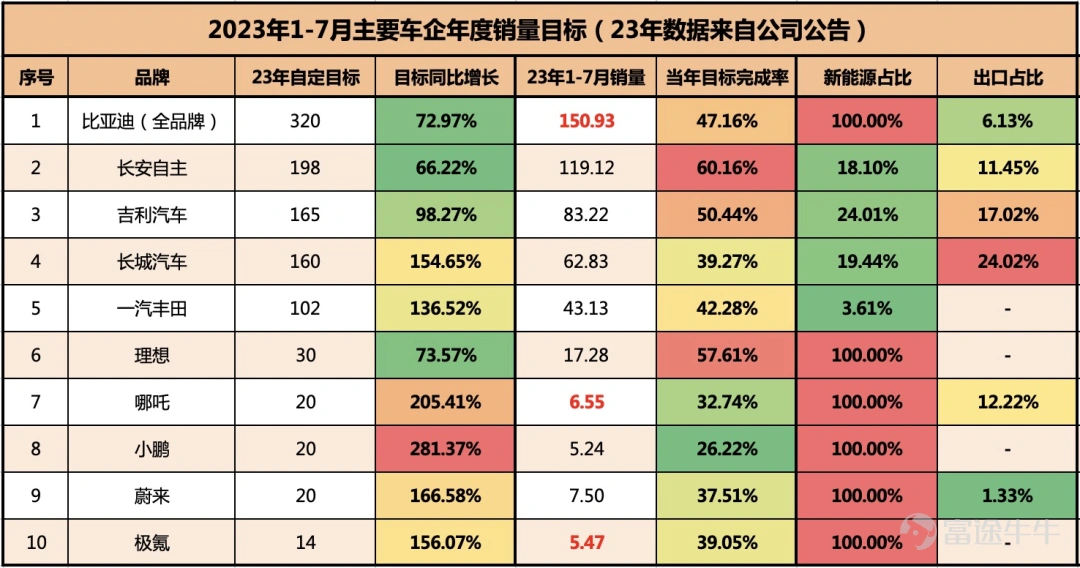

Combined with the data announced by each brand in January-July (including data from the Ride Federation),We'll find that in January-July, 58% of the time has passed, but only a few brands have achieved a mission completion rate of over 50%.

Data source: Company Announcements and Passenger Transport Association Sales Volume collated by the author

Changan announced that the sales volume of its own portion was 1.1912 million units, with a target achievement rate of 60.16%. It is the only brand that has achieved the target of 60% or more among the many brands currently counted.

Ideally, the target achievement rate is 57.61%; Geely is third, with a target achievement rate of 50.44%; BYD is fourth, with a target achievement rate of 47.16%.

There are even 5 brands whose target achievement rate is less than 40% (namely: Great Wall, Jidong, NIO, Nacha, and Xiaopeng). Under such circumstances, if no new cars are launched, what can car companies do without price cuts?

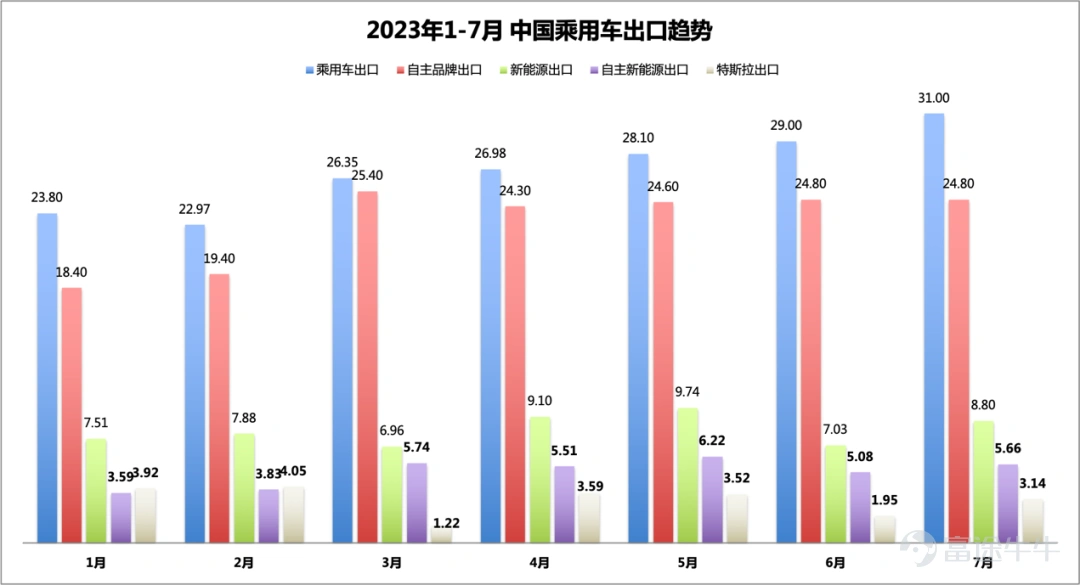

Exports became a lifesaver and one of the main response ideas for major brands in the first half of the year.

In January-July of this year, China exported 1.88 million passenger cars, an increase of 102.27% over the previous year, of which 1,617,000 were owned brand exports. Independent brand exports accounted for 85.9% of all passenger car exports, an increase of 93.0% over the previous year. Passenger car exports already account for 14% of China's total passenger car production, while this figure was less than 10% last year.

In January-July, China exported 570,000 new energy vehicles, an increase of 139.6% over the previous year; of these, 356,000 units of autonomous new energy were exported, accounting for 62.5% of new energy exports, an increase of 194.4% over the previous year.

Data source: Collated by the author of the Ride Federation

Among these, SAIC Motor exported 571,000 vehicles, up more than 40% year on year, and Chery exported 471,000 units, up more than 100% year on year. Even Chery's export volume had already surpassed domestic sales volume (accounting for 52.8% of export sales), Changan exported 215,000 units, Great Wall exported 151,000 vehicles, Geely exported 141,000 vehicles, Dongfeng exported 122,000 vehicles, and JAC and BYD exported 100,000 vehicles.

Even the joint venture, Guangqi Honda, has begun planning to produce a right-hand rudder version of the Odyssey and export it to Japan.

However, for most Chinese brands other than Chery's surprise, the domestic market still accounts for more than 80% of total sales. If domestic sales volume and market share cannot be guaranteed, the pressure to achieve annual goals is as great.

So,We will see that Euler (Great Wall), Nana, and Krypton, which have a target completion rate of less than 40%, have begun to drop prices one after another, and the price reduction is generally over 20,000 yuan. Even NIO and Xiaopeng cut prices in disguise through a new pricing system for new cars. The purpose is to achieve the sales target set at the beginning of the year as much as possible.

03

New energy brands are under a lot of pressure

It became a futile act to follow leading price cuts

In the field of new energy, the two leaders, Tesla and BYD, are like two mountains. Their every move will affect the changes in the entire new energy market.

At the beginning of the year, Tesla launched a price war, redefining the value benchmark of 200,000 to 300,000 yuan of pure electric new energy; after the Spring Festival, the BYD Champion Edition redefined the value benchmark for plug-in hybrid models of 100,000 to 300,000 yuan. As a result, every brand other than Ideal has been brought into round after round of price wars.

The Zero Run C11 extended range version brought the B-class new energy SUV into the competitive gradient of 150,000 to 200,000 yuan. The price of the launch of the Xiaopeng G6 completely rivaled the Tesla Model Y and detonated the market step by step, making Tesla's position in the 200,000 to 300,000 yuan pure electricity market begin to feel challenged. Deep Blue also drew on the idea of Zero Run. Using superior space and configuration, the S7 also reached the price range of 150,000 to 200,000 yuan. For the first time, the NIO ET5 travel edition allowed NIO to let go of the 300,000 yuan bottom line that luxury brands used to stick to. After divesting their charging and switching rights, the new ES6 also began to be somewhat cost-effective.

Although Ideal was not greatly affected overall, they also launched the L9 Pro version, which is priced at 429,000 yuan, and the L7 Air version, which does not include airborne suspension, to further expand their price space.

Of course, in addition to the “strategy of following the leader” and the reason the target completion rate is too low, there are also two factors that cannot be ignored: First, fuel vehicles are also cutting prices to protect sales volume. The starting price of A-class joint venture fuel vehicles has reached 77,900 yuan, and the overall price of B-class joint venture fuel SUVs is below 180,000 yuan, even the former “price increase” Toyota's Highlander and Sana, not only have there been no price increases or even started to have quite a few discounts.

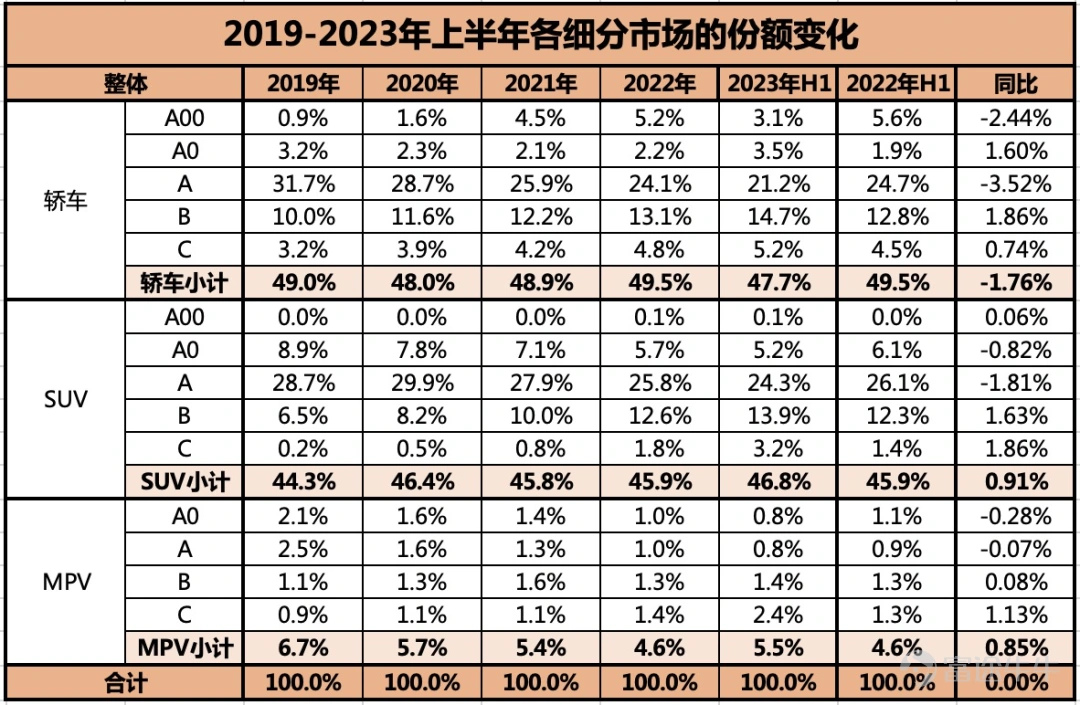

The second reason is that consumption upgrades and consumption downgrades have begun to occur simultaneously in the market.According to data from the Ride Federation for half a year, it shows:Apart from the increase in the market share of the A0 class sedan market in the first half of this year, the market share of the rest of the B-class and below began to shrink.

Data source: Collated by the author of the Ride Federation

In particular, the decline in the market share of A-class cars and A00 class cars is most obvious. Consumers who buy A-class cars are “price-sensitive” customers. On the one hand, the price drop for B-class cars has triggered an upgrade in their consumption, but it is more about consumption downgrading to A0 class pure electric products that can provide the same space. However, consumers who buy A00 class products are “income-sensitive” customers. For some consumers with good income expectations, consumption is enough to upgrade to level A0. More consumers simply choose not to buy vehicles due to poor income expectations.

Under the dual influence of price cuts by market leaders and poor revenue expectations, many new energy brands will surely become the new normal in the new energy market in the second half of the year by following price cuts and further price cuts in order to survive.

The price war is no longer a very unusual thing for the Chinese automobile market. Since 2010, this situation has occurred at least 2 times. In the end of the 2018 price war, joint venture brands represented by Germany and Japan benefited; but this time, new energy brands represented by BYD and Tesla will benefit, and the share of traditional fuel vehicles and traditional joint venture brands will be drastically reduced.

The price war has always started with the “leader” and ended with the “leader”. Currently, it seems that leading companies must complete their annual goals. Whether it's BYD or Tesla, they still have the ability and will to continue to release prices to charge higher sales volumes.

In the short term, this price war will continue until the end of this year, and even in the first quarter of next year, we will be able to see clearly.

You have to see at least a few former giants that have lost more than half of their market share before you see signs of the end of the price war.

Of course, for all OEMs and practitioners, the price war means more serious internal or external sources; but for most consumers, spending less to buy better products is something they are happy to see.

What are your thoughts on this round of price war? Welcome to the comments section to have a chat.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

5

5