“藥明系”科笛-B開啟認購,你看好嗎?

IPO | “Pharmacology Department” Kodi B is now offering shares and is expected to go public on June 12

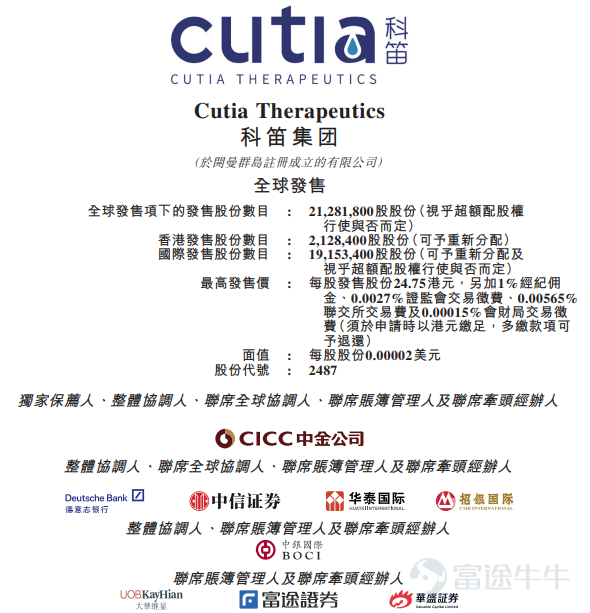

Futu News reported on May 31 that “Pharmacomics” this Wednesday$CUTIA-B (02487.HK)$It was announced that the stock exchange will be held from May 31 to June 5. It is proposed to issue 21.2818 million shares, including a public sale of 2.1284 million shares (10%) and an international sale of 19.153,400 shares (90%). The issue price per share is HK$20.65-24.75, and 200 shares per lot. It is expected to be listed on June 12.

Source: Procurement Book

Company Overview

Kodi B is a dermatology-focused R&D biopharmaceutical company, focusing on a wide range of dermatology treatment and care treatment fields, including localized fat accumulation management drugs, hair diseases and care, skin diseases and care, and epidermal anesthesia. The company has one core product and eight other pipeline candidate products, and also distributes two commercial products developed by overseas partners. The core product CU-20401 (a recombinant mutant collagen enzyme that targets obesity, overweight, or other metabolic diseases associated with localized fat accumulation) was developed as a local fat accumulation management drug for skin disease treatment, while the local fat accumulation management drug market in China is still in the early stages of growth, and there are no approved products yet. As of the last practical date, the company held a patent relating to the core product.

The Kodi Group was founded by Tonghe Yucheng and Zhang Lele. It is a “pharmacology” company. Among them, Yucheng Capital is an investment company that became independent from the venture capital division of Pharmaceutical Kangde. Tonghe Capital is an investment company founded by Chen Lianyong, a former partner of Fidelity Asia Growth Fund. After the merger of the two agencies, Li Ge, the actual controller of Yao Ming Kangde, became the chairman, and Chen Lianyong became the CEO.

According to reports, the company is one of the few participants with comprehensive comprehensive capabilities in China's extensive dermatology treatment and care market. It has a comprehensive product pipeline covering nine products and candidate products, including five clinical stage and four pre-clinical drug candidates to meet market demand. The company's success is due to the company's comprehensive capabilities, customer-centric philosophy and continuous innovation driven by the proprietary CATAME® technology platform, a comprehensive product pipeline, and an experienced management team. It is expected that it will continue to expand its business scale and increase market share by leveraging anticipated growth in China's extensive dermatology treatment and care market.

Industry Overview

On the industry side, according to Frost & Sullivan, China's extensive dermatology treatment and care market increased from RMB 300.4 billion in 2017 to RMB 471.8 billion in 2021, with a compound annual growth rate of 11.9%. It is expected to increase to RMB 670.2 billion and RMB 1,0375 billion respectively in 2025 and 2030, with a compound annual growth rate of 9.1% from 2025 to 2030. Despite rapid growth, per capita annual expenditure on extensive skin treatment and care in China remains low due to a lack of comprehensive, effective and alternative solutions. Meanwhile, Codi-B is committed to providing comprehensive solutions for different treatment fields in China's rapidly developing and extensive dermatology treatment and care market.

Source: Procurement Book

In 2021, per capita expenditure on treatment and care for a wide range of skin diseases in the US, Japan and South Korea reached RMB 1,828.0, RMB 1,417.3, and RMB 1,406.9, respectively. In contrast, China's per capita expenditure for extensive dermatology treatment and care in 2021 was RMB 334.0, which still lags far behind developed countries, which means that the market potential is huge.

Furthermore, according to Frost & Sullivan, the market size of local fat accumulation management drugs is expected to grow because (i) some localized fat accumulation drugs are expected to be approved in China; (ii) the approval and availability of local fat deposition drugs continues to increase due to increased safety and convenience of treatment; (iii) the number of obese and overweight people who can receive fat accumulation management drugs in China is estimated to continue to increase; (iv) patients receiving drugs for fat accumulation management drugs generally show high repurchase rates to maintain expected results; (v) physicians of various product manufacturers Explanation and promotion have led to a continuous increase in the clinical penetration rate of the product; (vi) the clinical use of the product in hospitals will increase the credibility of the product and the number of users.

The market size of localized fat accumulation management drugs that can be used as labels is expected to increase from RMB 86.7 million in 2023 to RMB 514 million in 2025, with a compound annual growth rate of 143.6% from 2023 to 2025. The market size is expected to reach RMB 2,440 billion in 2030, with a compound annual growth rate of 36.5% from 2025 to 2030. According to Frost & Sullivan, in 2021, the target patients for women and men with fat accumulation in China were 170 million and 182 million, respectively, and are expected to reach 211 million and 224 million respectively in 2030. The target market for core products accounts for only a very small portion of the overall broad dermatology treatment and care market in China.

Financial situation

In terms of financial conditions, in 2021 and 2022, Kodi B received revenue of RMB 2,038,000 and RMB 11.366 million respectively. The revenue came from customers located in Greater China. The vast majority of revenue came from hair diseases and care products (CU-40102, CUP-MNDE and CUP-SFJH), skin diseases and care products (CU-10201), and several skincare products (daily skincare products) such as masks, creams, toners, sprays, serums and gels. The sharp increase in revenue was mainly due to increased sales of the company's hair disease and care products and daily skincare products. The company expects to continue to generate most of its revenue from these sources and expand revenue streams after commercialization of products and candidate products.

Source: Procurement Book

During the period, the company achieved gross profit of RMB 1.6 million and RMB 7.9 million respectively, with gross margins reaching 79.0% and 69.8% respectively. The increase in gross profit was mainly due to (i) increased earnings; and (ii) changes in product portfolio structure.

The R&D costs for the period were RMB 111 million and RMB 181 million. The increase in R&D costs was mainly due to (i) an increase in the number of R&D personnel in 2022, (ii) an increase in share-based payment expenses due to new grants under the Pre-IPO Stock Incentive Plan in 2021 and December 2022, and (iii) an overall increase in the company's clinical and pre-clinical R&D activities, as the company promoted more candidate products during the development phase.

Cornerstone investors

In terms of Cornerstone investors, a number of Cornerstone investors agreed to subscribe for the number of shares available for purchase at the sale price, totaling approximately HK$181 million (assuming an offer price of HK$22.70, which is the median of the offer price range). These cornerstone investors are Harvest, Sun Hung Flute Venture Capital, and So-younghk. The company believes that Cornerstone Placement will help enhance the company's image and show that such investors are confident in the Group's business and prospects.

Use of funding

In terms of fund-raising purposes, the net proceeds from Cordi-B's proceeds amount to approximately HK$413 million (assuming no over-allotment rights are exercised, based on the median issue price of HK$22.70). According to the prospectus, the company plans to use the net proceeds from the stock sale for the following purposes: about 45.0% will be used for the company's core product CU-20401; about 22.0% will be used to disburse the continuous R&D activities of the company's main products CU-40102 and CU-10201, including planned clinical trials and preparation of registration documents; about 18.0% will be used to disburse ongoing research and development activities for other candidate products in the company's pipeline, including planned clinical trials and preparation of registration documents; about 10.0% will be used for technology development and business development for pipeline expansion; and about 5.0 percent will be used for technology development and business development for pipeline expansion; and about 5.0 percent will be used for technology development and business development of the company's main products CU-40102 and CU-10201; and about 5.0 percent will be used for the continuous development of the company's main products, CU-40102 and CU-10201; % will be used for working capital and other general business purposes.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

5

20