廣告收入再度下滑!谷歌業績你如何評價?

Google's revenue and profit were poor in the fourth quarter. Advertising revenue declined for the second time since the IPO, but cloud revenue increased 32% | Financial News

After the US stock market on Thursday, February 2, digital advertising and search giant Google's parent company$Alphabet-A (GOOGL.US)$Financial results for the fourth quarter of 2022 were released.

Since revenue and EPS for the fourth quarter fell short of expectations, earnings fell 3.6% year on year for the third consecutive quarter. Advertising revenue fell 3.6% year on year in the fourth quarter, the second decline since the IPO listing in 2004. YouTube became a weak point in earnings for three consecutive quarters. Google's stock price once rose 1% after the market, then quickly fell more than 4%. Although Google Cloud's revenue fell short of expectations, it increased 32% year on year, and continued to be the growth engine.

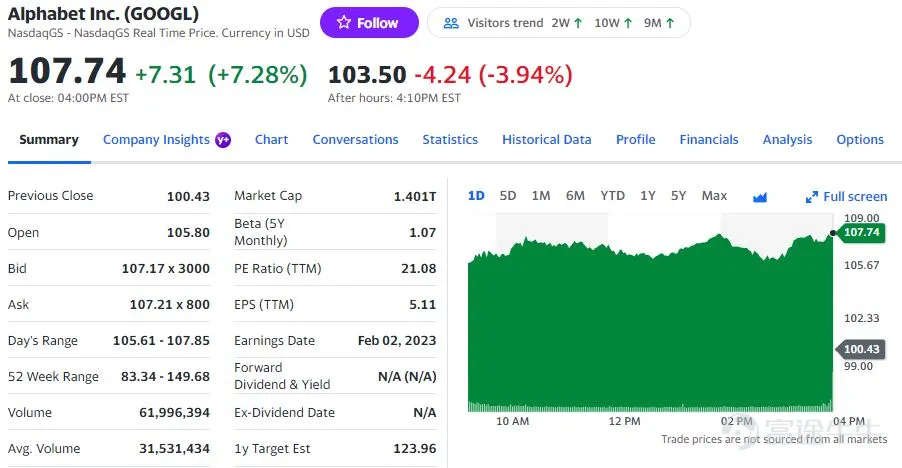

Google Class A stocks (GOOGL) rose more than 7% on Thursday, rising three consecutive days to the highest level in four and a half months since September 12 last year. So far in 2023, it has risen 22%, and fell 39% in 2022, and the NASDAQ fell 33% during the same period. Despite a rebound in stock prices in January, Google fell about 27% over the past 12 months, the information technology sector of the S&P 500 index fell nearly 17% during the same period, and the S&P market fell 9%.

Among the 51 analysts covering the stock, 47 suggested “increasing holdings”, 4 suggested “holding”, and none recommended selling. The average target price was $123.22, which means there is still room for 14% growth.

Google's fourth-quarter revenue and EPS fell short of expectations, with earnings falling year-on-year for the third consecutive quarter

Financial reports show that Google's parent company's total revenue for the fourth quarter of last year was 76.05 billion US dollars, lower than analysts' expectations of 765 US dollars, but it achieved a 1% year-on-year increase from 75.3 billion US dollars in the same period last year, but it was clearly inferior to the double-digit increase during the pandemic.

Earnings per share for the quarter were 1.05 US dollars, lower than market expectations of 1.18 US dollars. They fell more than 31% from 1.53 US dollars in the same period last year, to the lowest since the fourth quarter of 2020, and fell for three consecutive quarters.

Net profit was 13.624 billion US dollars, down 34% year on year.Profit declined for the third consecutive quarter, and the downward trend accelerated. Net profit in the second quarter of last year fell 14% year on year, and net profit in the third quarter fell 26.5% year on year.

Operating profit for the quarter was close to US$18.2 billion, down 17% from the previous year; operating profit margin was 24%, compared to 29% in the same period last year. However, traffic acquisition costs (TAC) paid to partners in the fourth quarter were $12.93 billion, lower than market expectations of $13.32 billion. After deducting TAC's impact on profits, revenue was US$63.1 billion, which was basically in line with expectations, an increase of nearly 2% over the previous year.

In 2022 as a whole, Google's total revenue was US$283 billion, an increase of 10% over the previous yearThere was a sharp 41% year-on-year increase in 2021, annual revenue calculated at a fixed exchange rate increased 14% year-on-year last year, and revenue calculated at a fixed exchange rate increased 7% year-on-year in the fourth quarter of 2022.

Earnings per share in 2022 were $4.56, down nearly 19% year on year, and EPS increased nearly double year on year in 2021. Operating profit last year was US$74.8 billion, down nearly 5% year on year, up 91% year on year in 2021; last year's operating profit margin was 26%, down from 31% in 2021.

Cloud revenue increased 32% year over year, and last year's growth rate declined quarterly, but operating losses were cut in half, and YouTube advertising revenue continued to be poor

Looking at it by business,The cloud business that the market is most concerned about and is seen as Google's next growth engineFourth-quarter revenue was 7.32 billion US dollars, lower than the forecast of 7.43 billion US dollars, but increased 32% year on year, maintaining double-digit growth, and the total amount was double that of the end of 2020.

However, the year-on-year growth rate of cloud revenue is declining quarterly, increasing 43.8%, 35.6%, and 37.6% in the first three quarters of 2022; increasing 46%, 54%, 45%, and 44.6% respectively in the 2021 quarter.The operating loss of the cloud business in the fourth quarter of last year was 480 million US dollars, halving the year-on-year loss。

Google Cloud includes infrastructure and data analysis platforms (GCP, or Google Cloud Platform) for enterprise customers, and productivity and collaboration tools (Google Workspace), which account for nearly 10% of total revenue. There is still a big gap with Microsoft, the leader in the cloud field.

Last week's earnings report showed that Microsoft Cloud's revenue increased 22% year-on-year to 27.1 billion US dollars in the fourth quarter of last year. Constellation Research analyst Ray Wang pointed out that Google Cloud must grow by more than 50% each year to catch up.

Ads are also a major revenue driver for Google that Wall Street is closely watching. Google's advertising revenue in the fourth quarter of last year was 59.04 billion US dollars, lower than the forecast of 60.64 billion US dollars, down 3.6% from the previous year.

This is the first year-on-year decline in Google advertising revenue since the outbreak of the epidemic in Europe and the US. It is also the second decline since the company's IPO listing in 2004.The previous decline occurred in the second quarter of 2020, when the outbreak had just broken out.

Among them, the YouTube video platform's advertising revenue was 7.96 billion US dollars, falling 7.8% from the previous year, falling 7.8% from the previous year. The third quarter of last year was the first decline in history since the department's results began to be announced in 2019.

Previously, analysts believed that Google's core advertising business would maintain single-digit growth until the end of 2023, mainly damaged by the macroeconomic slowdown and fierce competition from TikTok.

Losses in the innovation business continue to expand, and the focus on artificial intelligence is reiterated. Future financial reports will include DeepMind in the company's costs

Financial reports show that revenue from Google search and other businesses was 42.6 billion US dollars, down 1.6% from the previous year. This shows that compared with the third quarter, the spending of some advertisers fell further in the fourth quarter.

The revenue generated by Google's online business, or Google partner website through the AdSense program, was 8.48 billion US dollars, falling nearly 9% year on year over expectations, and falling year on year for two consecutive quarters. This department was targeted by antitrust lawsuits from the US Department of Justice.

The third part of the financial report — “Other Bets” (Other Bets) was once Google's science and technology innovation division, targeting forward-looking product development and venture capital, including autonomous driving startup Waymo, artificial intelligence DeepMind, intelligent medical Verily, venture capital funds Google Capital and Google Venture.

The revenue of this business in the fourth quarter of last year was 230 million US dollars, an increase of nearly 25% over the previous year; the operating loss was 1.63 billion US dollars, which is wider than the operating loss of 1.45 billion US dollars in the fourth quarter of 2021.

Alphabet said that since artificial intelligence is critical to achieving the company's mission of “bringing breakthrough innovation to the real world”, the financial reporting format will be changed from January 2023, and DeepMind, which previously included “other bets,” will be integrated into the company's costs to reflect its growing cooperation with Google Services, Google Cloud, and other betting businesses.

Alphabet and Google CEO Sundar Pichai (Sundar Pichai)On the call, the company's focus on artificial intelligence was reiterated, also referred to as:

“Our long-term investment in deep computer science puts us in a very good position when AI reaches an inflection point, and the company is about to make an AI-driven leap forward in search and beyond. Soon, people will be able to directly interact with our newest and most powerful language models in experimental and innovative ways as a companion to search activities.”

Alphabet and Google Chief Financial Officer Ruth Porat emphasized that optimizing the cost structure is the next phase of focus to “support our investment in the highest growth priorities and achieve long-term profitable growth.” The number of employees of the company in the fourth quarter of last year was slightly over 190,000.

Google announced about 12,000 layoffs in January, which is expected to result in employee layoffs and related expenses of 1.9 billion to 2.3 billion US dollars. Most of these will be confirmed in the 2023 quarterly report. Additionally, Google is optimizing global office space and is expected to generate approximately $500 million in exit costs associated with reduced office space in the first quarter of 2023.

Wall Street is concerned about digital advertising trends during the economic slowdown and the threat that AI chat tool ChatGPT poses to Google search

Google, a subsidiary of Alphabet, is the world's largest digital advertising platform. When the macroeconomy faces a risk of stagnation or even recession, advertisers tend to cut spending. However, Google's performance has always been due to other companies that rely on ad revenue, because brands generally believe that advertising on Google's search engine is critical to driving website visits or other consumer behavior.

Digital advertising once accounted for more than 80% of Alphabet's total revenue in 2021. Digital advertising slowed sharply last year as advertisers responded to falling consumer demand and concerns about the economic recession. Market research firm Insider Intelligence lowered its forecast for 2022 digital ad spending by $35 billion, or nearly 6%, in November last year.

Investors are also concerned about the competitive pressure of the artificial intelligence chat tool ChatGPT invested by Microsoft on Google's search engine. According to a research report released by UBS yesterday, ChatGPT, a chatbot owned by OpenAI, was launched in January of this year, that is, just two months after its launch,Monthly active users are estimated to have reached 100 million, making it historyFastest growing consumer apps。

According to the latest report, Microsoft is considering adding the ChatGPT function to the Bing search engine in the next few weeks, and Google is also asking employees to test ChatGPT's competitors, including an artificial intelligence chatbot called “The Apprentice Troubadour,” and explore embedded search engines.

Broker Jefferies believes that Google's core search business “is unlikely to be uprooted by ChatGPT,” maintaining a bullish rating for Alphabet and a target price of 125 US dollars, which means there is still room for an increase of nearly 17%. The reason is that the use cases for search services are very different from natural language AI chatbots, and search has moved from text to multiple modes such as text and images.

Due to excessive recruitment during the pandemic, Google announced last week that it would lay off 12,000 employees, accounting for about 6% of the total number of employees worldwide, making it the third tech giant to announce layoffs in January after Microsoft and Amazon. Analysts such as Jefferies believe that Google may further lay off workers to cut costs and push the market's estimate of its EBITDA profitability upward, which is good news for stock prices.

Google will face many anti-monopoly lawsuits in the future, and legal disputes have also attracted attention. Last week, the U.S. Department of Justice and eight state prosecutors sued Google, claiming it misused its dominance in the online ad tech sector to “eliminate adtech rivals through acquisitions.” As early as 2020, the US Department of Justice filed an antitrust lawsuit against Google's search service and search ads, which will be heard in September this year.

Bank of America analyst Justin Post also maintained an “increase in holdings” rating for Alphabet this week, but the core Google profit margin for the fourth quarter of last year is expected to drop 566 basis points year over year. According to its research report, “Google continues to be viewed as a defensive stock in the industry”. The target price increase of 3 US dollars to 119 US dollars indicates that there is room for an increase of 11%. Layoffs and other cost reduction measures may improve profit margins in the second half of the year.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

6