台積電業績高增長,半導體能否一掃頹勢?

The challenges of TSMC

TSMC is about to become the global semiconductor sales champion of 2022.$Taiwan Semiconductor (TSM.US)$, the challenges it faces are also growing.

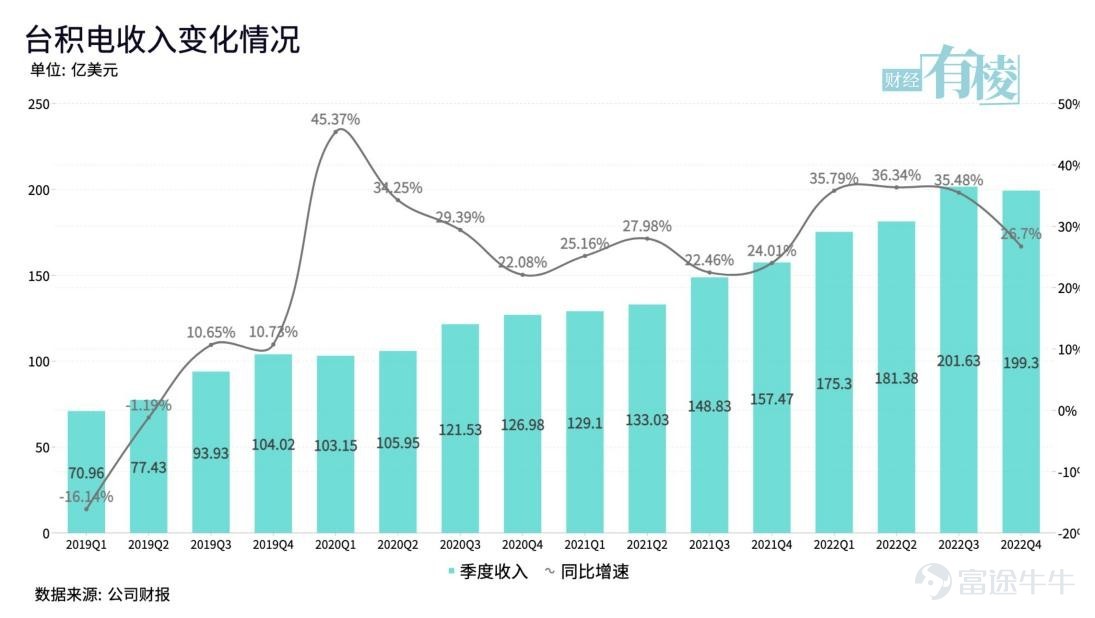

On January 12, Taiwan Semiconductor announced its Q4 performance for last year. Revenue reached NT$625.53 billion (all amounts in New Taiwan Dollars unless otherwise specified), up 2% quarter-over-quarter (a decrease of 1.5% in USD terms), and a year-over-year increase of 26.7%. Net profit was NT$295.9 billion, an increase of 5.4% quarter-over-quarter and 78.0% year-over-year.

Thus, Taiwan Semiconductor achieved revenue of NT$2,263.89 billion for the whole year of 2022, a year-over-year increase of 42.6%. The gross margin was 59.6%, and net profit reached NT$1.017 trillion, a year-over-year increase of 70.4%, surpassing the NT$1 trillion mark for the first time.

During the earnings call, President C. C. Wei provided an outlook for 2023, predicting a roughly 4% decline in global semiconductor output value excluding memory, with the semiconductor foundry industry expected to drop by about 3%. Taiwan Semiconductor anticipates slight growth for the full year, but the first quarter will see a quarter-over-quarter decline of 12.2%-14.2%.

A double-digit decline is actually quite significant, with the last occurrence being in Q1 2019. How to address the industry's 'chill' is the first challenge Taiwan Semiconductor faces. Another challenge is that 'the semiconductor supply chain is shifting from globalization to localization'.

In the conference call, Taiwan Semiconductor also mentioned that 'labor and other factors have caused the cost of building factories in the U.S. to be 4 to 5 times higher than in Taiwan.' However, 'the second new factory in Japan and the automotive chip plant in Europe are under consideration, provided there is sufficient support from customers and local governments.'

Is Taiwan Semiconductor, which prides itself on its technological superiority, getting a bit complacent?

01 3nm Technology Expected to Take on a Significant Role

As of this quarter, Taiwan Semiconductor’s quarterly revenue has maintained positive growth in New Taiwan Dollar terms for 12 consecutive quarters; in USD terms, it has maintained positive growth for 11 consecutive quarters, while this quarter saw a 1.5% decline quarter-over-quarter.

This is mainly due to the continuous depreciation of the New Taiwan Dollar against the US Dollar, with the New Taiwan Dollar falling 9.48% against the US Dollar in 2022.

The 'strong US dollar' has also dampened global economic performance, with continued sluggish demand in the smartphone market causing Taiwan Semiconductor's HPC (high-performance computing) quarterly revenue share to exceed that of smartphones for the third time this year.

Looking at the entire year, among Taiwan Semiconductor's five major revenue sources, HPC and automotive platform revenues have seen positive annual growth rates, while smartphone, IoT, and digital consumer electronics platform revenues have all experienced negative annual growth rates.

Among these, high-performance computing and smartphones combined account for over 80%, having the largest impact on performance.

Global smartphone shipments have been declining since 2022, with high inventory levels among end manufacturers leading to reduced chip demand. Although last quarter saw a boost in smartphone revenue share due to stockpiling momentum from new iPhone main chips, the overall market is still in a destocking phase, resulting in another decline this quarter.

High-performance computing mainly consists of data centers and graphics cards, but the former's high growth is no longer present, while the latter remains affected by the sluggish PC market, making the outlook less than optimistic. Rising inventory levels can be observed in NVIDIA's earnings reports, one of Taiwan Semiconductor's major customers.

In terms of process technology, Taiwan Semiconductor's 5nm accounted for 32% in Q4, while 7nm accounted for 22%, with a combined share reaching 54%. For the full year, compared to 2021, the revenue share of 7nm decreased by 4 percentage points, while that of 5nm increased from 19% to 26%.

The 7nm segment saw a decline in revenue share due to a slowdown in high-performance computing demand.

During the earnings call, Taiwan Semiconductor also noted that the capacity utilization rate for 7nm and 6nm is no longer at the high levels seen in the past three years, estimating that it will take several quarters to adjust, with expectations for demand to recover in the second half of this year.

Taiwan Semiconductor also stated that N3 (3nm) entered mass production in the fourth quarter of last year, and N3E (enhanced version 3nm) will enter mass production in the third quarter of this year, expected to contribute 4%-6% of revenue, higher than the contribution from 5nm in its first year of mass production, with the number of customer product design cases being more than twice that of 5nm.

At the end of December last year, Taiwan Semiconductor Chairman Morris Chang also mentioned that the yield rate for 3nm mass production is equivalent to that of 5nm, and starting from the first year of mass production, it generates more revenue annually than 5nm. He estimated that 3nm technology will unlock approximately $1.5 trillion in end-product value globally within five years.

So, what exactly are the revenue expectations for Taiwan Semiconductor's highly anticipated 3nm technology in 2023?

Taiwan Semiconductor’s 5nm process began mass production in 2020, accounting for 8% of its total revenue that year, which was $47.44 billion, or approximately $3.8 billion. Taiwan Semiconductor has provided a 'slight growth' outlook for 2023, suggesting that it should remain below $100 billion. Assuming $100 billion, 6% would equate to $6 billion.

Therefore, revenue from the 3nm node is expected to fall between $3.8 billion and $6 billion, but can this target be achieved?

On January 10, Taiwan's Electronic Times reported that nearly all major chip companies—Apple, Qualcomm, MediaTek, NVIDIA, AMD, and others—have placed orders with Taiwan Semiconductor for nodes under 5nm.

However, according to a Weibo post by 'Mobile Chip Expert,' Taiwan Semiconductor plans to lower prices for all its 3nm processes, as customers believe current quotes are too high. Apple’s orders will enter mass production in 2023, while those from other clients will only start in the second half of 2024.

Currently, Taiwan Semiconductor charges $20,000 per wafer for its 3nm chips, reflecting the industry adage that 'the more advanced the process, the higher the cost.' The ambitious 3nm node still appears to have a long journey ahead.

02. Production Concentrated in Taiwan

In terms of revenue distribution, 68% of Taiwan Semiconductor’s 2022 revenue came from the U.S., up from 65% in 2021. Among other regions, only mainland China saw a 1% increase, with all others showing declines.

Data Source: Taiwan Semiconductor Financial Reports

This highlights that U.S. customers are Taiwan Semiconductor’s primary focus.

At the end of last year, C. C. Wei first explained the reason for building a factory in Japan, stating it was 'to strategically support the largest supplier who is also a Taiwan Semiconductor customer.' He emphasized that if the largest customer cannot sell their products, Taiwan Semiconductor’s 3nm and 5nm chips will not sell either, so we must support them.

This major customer is naturally Apple, and Sony is indeed Apple’s largest supplier. The logic aligns with what Zhang Zhongmou stated: 'Globalization is dead.' Building factories near major customers should be the result of Taiwan Semiconductor's careful consideration.

During the conference call, an analyst mentioned the issue of 'higher costs in the United States compared to Taiwan,' to which Taiwan Semiconductor responded that labor and various local expenses make costs about 4-5 times higher than in Taiwan. However, Taiwan Semiconductor aims for overseas gross margins to remain above 25% to ensure profitability abroad.

Since 2020, Taiwan Semiconductor’s overall gross margin has consistently remained above 50%, reaching 62.25% this quarter. In comparison, the overseas gross margin is equivalent to being 'halved.'

However, when President C. C. Wei described the overseas factory construction plans, he noted that a second new plant in Japan and an automotive chip plant in Europe are under consideration, but only if customers and local governments provide sufficient support.

The implication is straightforward: the extra costs should be borne by the other party. Taiwan Semiconductor seems to be acting a bit arrogantly.

But Taiwan Semiconductor, which controls the most advanced processes, indeed has this confidence. During the conference call, Taiwan Semiconductor stated: 3nm is in short supply and will begin contributing significantly to revenue from the third quarter.

Taiwan Semiconductor also emphasized that it will continue to expand investments within Taiwan. The 3nm process is already in mass production at the Southern Taiwan Science Park plant, while the 2nm process will enter mass production in 2025, located at the Hsinchu Science Park and Central Taiwan Science Park.

In December last year, Taiwan's Economic Daily News reported that the Hsinchu Science Park Authority stated that Taiwan Semiconductor's 1nm plant would be located in the park and could begin mass production as early as 2028.

This means that the most advanced processes at Taiwan-based plants will always lead overseas plants by one to two generations.

In terms of advanced production capacity, the design capacity of Taiwan Semiconductor's first factory in Arizona is 20,000 wafers per month, accounting for only one-fifteenth of Taiwan Semiconductor’s current advanced capacity (300,000 wafers per month).

Even by 2026, after the second factory in Arizona begins operations, with a combined monthly capacity reaching 50,000 wafers, over 90% of Taiwan Semiconductor’s most advanced production capacity will still be concentrated in Taiwan.

According to statistics from Nikkei, between 2023 and 2026, Taiwan Semiconductor will gradually start mass production of 3nm chips at seven locations within Taiwan. Additionally, 2nm chips will begin mass production at four locations starting in 2025, with cutting-edge production capacity expected to exceed one million wafers per month by 2026.

This also shows that overseas production capacity accounts for only a small fraction of total capacity.

03. Competition is a one-way street.

During the earnings call, Taiwan Semiconductor projected its capital expenditure for this year to range between $32 billion and $36 billion, which is lower than last year. Approximately 70% of these expenditures will be allocated to advanced processes, 20% to special processes, and 10% to areas such as advanced packaging and photomask production.

With N3 and N3E yields already equivalent to 5nm (80%), the focus should now primarily shift to 2nm, which is considered another key battleground for technological competition following 3nm.

From the perspective of advanced process technology trends, 2nm is even more critical. Its main technological feature is the use of a gate-all-around (GAA) structure to replace fin field-effect transistors (FinFET), thereby effectively reducing chip power consumption and operating temperatures.

In recent years, Taiwan Semiconductor and Samsung have emerged as leaders in the race for advanced processes, competing around 3nm. Currently, Taiwan Semiconductor holds an advantage in mass production yield rates.

In October last year, Samsung updated its technology roadmap, planning to start production of 2nm chips in 2025 and 1.4nm chips in 2027, attempting an 'overtaking on a curve.' Meanwhile, after 2nm, Taiwan Semiconductor is advancing directly to 1nm, which could represent the physical limit of silicon-based chips.

Intel, which had previously fallen behind, is also catching up by establishing a process iteration roadmap up to 2025, specifically advancing through five process nodes: 10nm, 7nm, 5nm, 2nm, and 1.8nm.

This means that by then, Taiwan Semiconductor, Samsung, and Intel will all enter the 2nm mass production phase, adopting the new GAA transistor structure.

The technology competition among the three has become head-to-head.

Last year, Intel stated that its 3nm process node would officially surpass Taiwan Semiconductor to become the company with the best wafer fabrication technology, with the goal of becoming the world's second-largest foundry by 2030.

Even when building factories in the U.S., not far from Taiwan Semiconductor's Arizona plant (some say just a wall apart), Intel is constructing two 2nm factories; while Samsung’s factory is at 5nm, it plans to introduce 3nm technology by 2026, aiming to build 'the most advanced wafer fab in the U.S.'

In December last year, Taiwan's Economic Daily News reported that the head of the Hsinchu Science Park stated that Taiwan Semiconductor’s 1nm plant would be located in the park, with mass production expected to begin as early as 2028.

Notably, in Q3 of last year, Samsung Electronics’ revenue from wafer fabrication surpassed its flash memory business revenue for the first time, indicating efforts to reverse the downturn in its foundry business.

However, Samsung may face disappointment again in 2022.

In 2017, Intel was dethroned by Samsung, losing the title of the world's top semiconductor sales leader; this year in Q3, Intel outperformed Samsung but failed to reclaim the top spot as Taiwan Semiconductor surpassed both, achieving its first-ever quarterly leadership.

For the full year, there is little doubt that Taiwan Semiconductor will remain at the top.

According to Counterpoint Research data, in 2022, Taiwan Semiconductor's market share increased from 54% in the first quarter to 60% in the fourth quarter, while the market shares of its main competitors remained flat or declined.

Data source: Counterpoint Research

Although this only reflects foundry market share, it indicates that Samsung Electronics' foundry business revenue has been continuously shrinking, while Taiwan Semiconductor keeps expanding.

In the first three quarters of 2022, Samsung's semiconductor division, which includes both foundry and memory businesses, reported a combined revenue of $56.4 billion, compared to Taiwan Semiconductor’s $55.8 billion and Intel’s $49.012 billion.

It can be seen that Intel has lost its competitive edge, while the gap between Samsung and Taiwan Semiconductor is not significant.

According to Samsung Electronics’ earnings warning released on January 6, its Q4 2022 revenue decreased by 9% year-over-year. The market previously estimated its semiconductor division revenue at around 21.5 trillion Korean won ($16.4 billion), meaning the actual revenue should not exceed this figure.

Therefore, Samsung’s semiconductor division is projected to generate $72.8 billion in revenue for 2022, less than Taiwan Semiconductor’s actual revenue of $75.881 billion, making the latter highly likely to claim the top position.

But what comes after reaching the summit? It is believed that various challenges will follow even more closely, especially amid the complex global geopolitical environment and rapidly evolving emerging industries. Taiwan Semiconductor will need greater courage to navigate these changes.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

3