半導體投資該如何入門?

[Industry Nuggets] Laying off employees, cutting orders, and removing inventories, what step has the semiconductor cycle reached?

In 2022, the semiconductor industry as a whole underwent drastic changes. Whether it was a sharp decline in industry demand or mixed political geopolitical factors, all contributed to the arrival of a “cold winter” in the global semiconductor industry. However, every major downturn in the semiconductor industry ends with the arrival of new technology. With the emergence of more and more new terminal markets such as automobiles, industrial automation, 5G infrastructure, artificial intelligence, and cloud computing, chip demand and supply will also become more diverse, and the semiconductor cycle trough will eventually pass.

Are the three quarterly reports thunderous?

What is the semiconductor industry cycle like?

How are cycles tracked?

How to tap bullish stocks in the sector?

Is the semiconductor industry showing an anti-globalization trend?

Niu You's opinion: How to invest in semiconductors?

The three-quarter report was thunderous, and the peak of performance came early?

Recently, all major chip giants have released financial reports for the third quarter. Many giants' financial reports have fallen short of expectations. Some companies have even warned that the relationship between supply and demand is changing. The main reason is that they are concerned about a wider cooling of the chip market in the future.

In the early morning of November 3, Qualcomm's Q4 net profit for fiscal year 2022 was 2,873 billion US dollars, and the Q1 revenue guide for fiscal year 2023 was 92 to 10 billion US dollars, all lower than market expectations; Texas Instruments announced its quarterly report on the 25th. Although revenue and net profit continued to increase, the company said that Q4 revenue may have fallen short of expectations. Currently, only the automobile market is in strong demand; SK Hynix announced its Q3 financial report on October 26. Affected by the decline in demand for memory chips, the company's profit for the third quarter fell 60%, and next year's investment will be cut by more than 50% year-on-year; Samsung Electronics announced financial reports on the 27th In Q3, operating profit fell 31.4% to 10.85 trillion won, and smartphone production is being cut. Furthermore, TSMC has announced a 10% reduction in its investment budget for 2022, and predicts that the chip industry will experience a recession in 2023 due to inflation and rising costs, and that it will be “more cautious” about future demand performance.

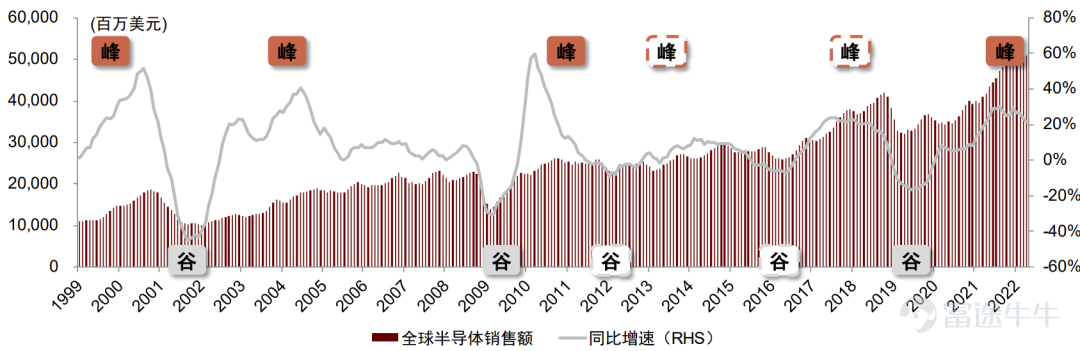

Semiconductor industry cycle

Semiconductors are an industry with both growth and cycles. There are differences and similarities in every cycle. On average, 4-5 years will go through a semiconductor cycle, showing the characteristics of “bulls are long and short” (1-3 years on the rise, 1-2 years on the downside). A complete semiconductor cycle is divided into seven steps, namely 1 demand explosion - 2 shortage price increases - 3 investment expansion - 4 gradual release of production capacity - 5 shrinking demand - 6 overcapacity - 7 price falls. The first 4 steps are in the most prosperous stage of the semiconductor industry. All major semiconductor-related companies will make a lot of money, and the next 3 steps will begin the stage of transition from prosperity to decline.

From the perspective of secondary market investment, during the upward and downward stages of the cycle, the SOX index usually experiences a “double blow to Davis” and a “double kill for Davis”; in the process of the cycle bottoming out, the SOX index is often 3-9 months ahead of fundamentals; in every cycle, there are opportunities for individual stocks to significantly outperform the SOX index. Referring to historical data, 2022 is in the downward phase of the cycle. The current valuation is already at the bottom of history, and the time to lay out the next cycle may not be far off.

Looking back at several cycles since 2000:

(1) The peak in 2000 was mainly due to the “Internet bubble” driving the expansion of Internet companies and spawning a surge in demand for semiconductors, which exceeded supply. The 2001 trough was mainly due to the collapse of the “Internet bubble” and a sharp decline in demand for semiconductors, which fell significantly below supply.

(2) There was little new supply on the global supply side in 2002 and 2003. Under the steady growth rate of shipments of personal computers, feature phones, etc., the demand side gradually recovered, causing (3) global supply to fall short of demand in 2004, and there was another peak.

(4) The 2009 financial crisis caused demand for semiconductors to plummet, supply exceeded demand, and there was a trough.

(5) When the supply-side decline in 2009 caused global demand to recover in 2010, supply was smaller than demand, and there was a peak. The 2011 European debt crisis caused demand to decline to a certain extent. At the same time, due to the centralized release of supply that year, supply exceeded demand, and there was a trough.

(6) Shipments of downstream terminals such as smartphones and tablets increased steadily from 2011 to 2014. The steady increase in demand for semiconductors caused supply to fall short of demand and peaked; (7) The centralized release of supply in 2015, supply exceeded demand, and there was a trough.

(8) Supply was released to a certain extent in 2016-2018, but demand grew faster, driven by terminals such as high-performance computing servers and mining machines, which led to a peak in 2018. Demand for personal computers and mobile phones slowed and memory prices fell in 2019, and there was a trough.

(9) Beginning in 2020, demand grew rapidly due to factors such as Huawei's collection of goods, the “shift wave” of 5G smartphones, and online work from home. Supply was less than demand, and there was a peak.

How are semiconductor cycles tracked?

Semiconductor sales, memory prices, inventory levels, wafer foundry capacity utilization, semiconductor equipment sales, silicon chip shipmentsQuarterly/monthly data is an effective indicator for tracking the semiconductor cycle, and it is possible to determine which stage the semiconductor cycle is in through cross-verification of multiple indicators. 2021 may be the peak of this cycle. According to the rules of the 2015-2019 cycle, it will take 4-6 quarters to complete processes such as inventory digestion.

Furthermore, the Philadelphia Semiconductor Index is also one way to invest in the semiconductor sector, which can capture beta in the semiconductor sector. According to the rules after 2010, the Philadelphia Semiconductor Index shows the characteristics of “bulls long and short bears”. The beginning of every upward cycle is first driven by valuation, and then by performance, that is, the capital market's investment pace in the Philadelphia Semiconductor Index is ahead of the fundamentals of the global semiconductor industry, usually 3-9 months ahead of the fundamentals of the global semiconductor industry. The Philadelphia Semiconductor Index covers 30 of the world's highest quality semiconductor companies and is the “barometer” of the global semiconductor industry. The Philadelphia Semiconductor Index is also one of the easiest and most effective ways to invest in beta in the global semiconductor sector.

The semiconductor cycle is difficult to predict, how to choose the best from the best?

Semiconductor companies are also subject to the ups and downs of the regular chip cycle associated with the laws of supply and demand. As the entire semiconductor industry goes through a cyclical process, companies in the industrial chain inevitably have to experience the law of survival of the fittest. Mergers and acquisitions between companies have continued, some companies have withdrawn from the historical stage (the most famous being the bankruptcy of Japanese storage supplier Erpida), and the revenue rankings of semiconductor manufacturers have fluctuated.

There are about 1,000 listed companies in the semiconductor industry as a whole with a market capitalization of about 500 billion US dollars. According to the 30 semiconductor companies behind the Philadelphia Semiconductor Index, the world's major semiconductor manufacturers mainly include Applied Materials, ASML, Brooks Automation, KLA, Lam Research, Tereda, Nvidia, Intel, AMD, Marvell, Texas Instruments, ADI, Broadcom, Skyworks, Qualcomm, Qorvo, Microchip, Micron, Ansenmei, NXP, Lattice, Silicon Labs, MPS, Power Integrations, IPG Photonics, Wolfspeed, II-VI, Entergris, TSMC, Amkor After experiencing a sharp rise in the semiconductor index to a 20-year high last year, the Philadelphia semiconductor index has fallen sharply this year.

Variable black swan: the anti-globalization trend of semiconductors is obvious

In addition to the impact of the global economy and the slowdown in market demand, the industrial policies of countries or regions around the world, as well as the ongoing Russian-Ukrainian war, have also become constraining factors affecting the semiconductor industry supply chain. Even based on considerations of political geopolitical relationships, the anti-globalization trend of the industry is becoming more and more obvious. Since the beginning of this year, industrial policies have been introduced and implemented frequently in various regions of the world, and various semiconductor companies have also launched a series of ambitious plans to expand production.

The US formed a chip alliance and introduced the US chip bill, which seems to indicate that the “American-made dream” is gradually being realized; major European chip giants have also accelerated their investment arrangements. In particular, the stimulus of the European Chip Act has attracted the implementation of some new projects. South Korea introduced the “Special Semiconductor Law”, which focuses on supporting the country's cutting-edge strategic industries, involving investment support, talent supply, development of system semiconductors, and increasing self-sufficiency in materials, components, and equipment to enhance core competitiveness. From the perspective of economic development, there is nothing wrong with every country in the world introducing industrial support policies, but putting too much emphasis on the interests of small groups is bound to be unhelpful to industrial globalization.

Niu You's opinion: How should semiconductors be invested?

Write at the end

After reading the above, I'm sure all of you have a certain understanding of the semiconductor sector and industry cycle. Here's the question:

(1) When do you think this semiconductor cycle will reach an inflection point?

(2) What do you think is the future development trend of the semiconductor industry?

(3) Which chip giant are you most optimistic about? Why is that?

(4) At the moment, what are your semiconductor investment strategies?

You can choose a question to discuss in the comments section, and you will have a chance to get high-quality answers66 pointsRewards~~

Reference materials

Will the global semiconductor industry enter its biggest recession since 2000?

The semiconductor boom continues to decline! Leading companies cut their investment in half and called for a vacation

CICC: Revisiting the semiconductor cycle has any implications for us?

A complete cycle in the semiconductor industry is divided into 7 steps. Which step has it reached now?

“Tekki” semiconductor cycle, “running water” chip companies

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (15)

to post a comment

40

28