SnowflakeQ2業績超預期,股價飆升

Snowflake's Full-Year Guidance Beats Expectations, Shares Surge Over 17% in After-Hours Trading | Earnings News

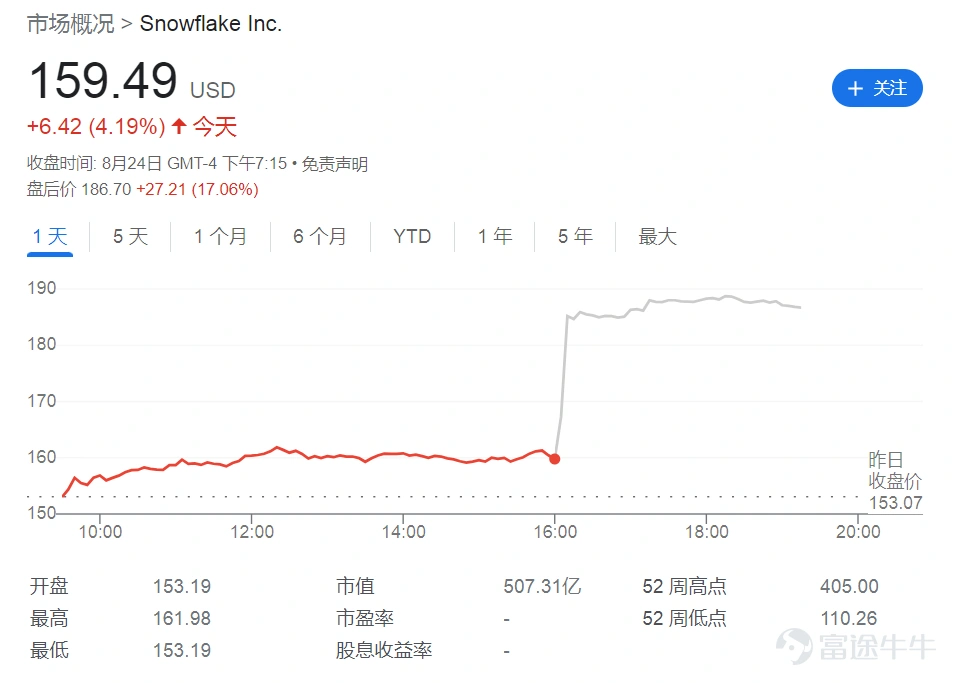

On Wednesday, August 24, Eastern Time, cloud computing and data analytics software company$Snowflake (SNOW.US)$Released its Q2 earnings report post-market, which covered the period up to July 31, 2022. Due to better-than-expected full-year guidance, Snowflake shares surged over 17% in after-hours trading.

On Wednesday, Snowflake closed up 4.19% at $159.49 per share. Year-to-date, it has fallen more than 50%, underperforming the Nasdaq's 21% decline during the same period.

Looking specifically at Snowflake’s core financial metrics for Q2:

Second quarter revenue was $497.2 million, surpassing analysts' expectations of $467.9 million.

Second quarter product revenue reached $466.3 million, exceeding the expected $438.1 million, representing an 83% year-over-year increase.

Remaining performance obligations for the second quarter totaled $2.7 billion, reflecting a 78% year-over-year growth.

Net revenue retention rate for the second quarter was 171%.

As of the end of the second quarter, the company had 6,808 customers.

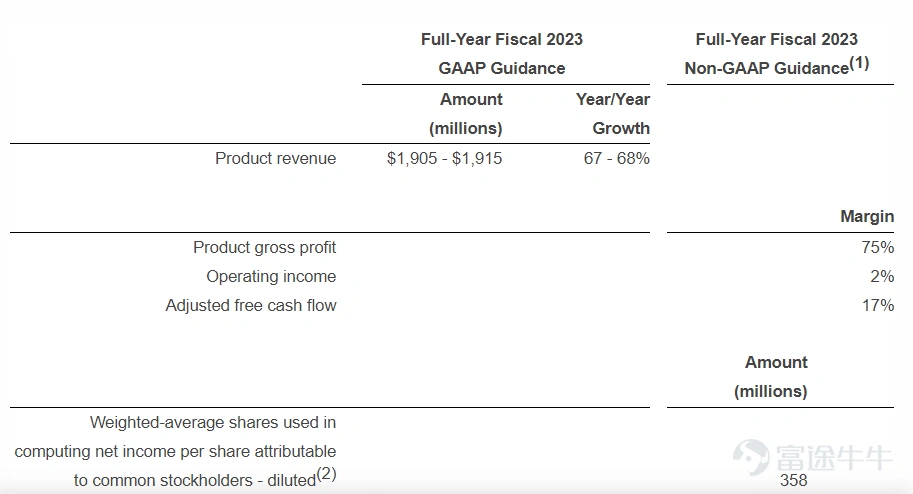

In addition, Snowflake also issued full-year guidance:

Product revenue for the full year is expected to reach $1.91-$1.92 billion, higher than the analysts’ forecast of $1.90 billion.

The adjusted operating margin for the full year is projected at 2.0%, up from the prior guidance of 1.0%.

Third-quarter product revenue is expected to be between $500-$505 million, compared to analysts' expectations of $501.1 million.

Regarding this, Snowflake Chairman and CEO Frank Slootman stated:

In the second quarter, product revenue increased by 83% year-over-year to reach $466 million. Our non-GAAP product gross margin exceeded 75%, and we continued to generate non-GAAP operating income and free cash flow. Snowflake’s next area of innovation aims to transform how cloud applications are built, deployed, sold, and transacted. We look forward to executing on this growth opportunity.

Snowflake is a major U.S. cloud computing company that has drawn significant attention. When the company first went public in the U.S. stock market in 2020, 'Oracle of Omaha' Buffett participated in the IPO subscription – marking his very first time doing so in over fifty years, despite his typically lukewarm stance towards tech stocks.

Although Snowflake's sales had grown more than 100% year-over-year for six consecutive quarters prior to December 2021, its growth momentum began showing signs of fatigue this year. Product revenue grew 84% in the first fiscal quarter, and this quarter, product revenue increased by 83% year-over-year – the lowest growth rate since its IPO in 2020 and the second consecutive quarter of declining product revenue growth.

However, despite the macroeconomic 'headwinds,' Snowflake’s earnings report was quite impressive. Not only did it prove that Buffett did not 'misjudge,' but it also showed that demand for cloud computing services remains relatively strong, which might be good news for other cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud.

Previously, Brian White, an analyst at investment bank Monness Crespi Hardt, stated that the data warehousing company was 'well-positioned' in terms of long-term trends, but at the time, he anticipated a potential slowdown in revenue growth. Therefore, the analyst maintained a 'neutral' rating on the stock.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

2