熱門中概股延續漲勢

Yan Cai: Is it time for the internet giants to turn the tide?

Earlier, Yan Cai had already summarized the overall situation of the US stock industry in the first quarter.Yan Caijun published a series of articles to conduct an in-depth analysis of the current economic situation in the US and the emerging trends focusing on the industry.

If we wanted to summarize the first quarter of the US technology industry, through the financial reports of key companies, Yan Caijun thought it could be summarized into the following 4 key points:

▷ The macro environment is becoming more and more complex. High inflation has had a big impact on many industries, and the 2C Internet is under overall pressure

▷ Omicron toxicity declined, social activities gradually returned to normal, and stocks benefiting from the pandemic fell to the altar

▷ The competitive environment on the Internet has deteriorated, and “volume” has seriously deteriorated

▷ The 2B-side business is generally stable. In particular, the cloud computing industry is still growing rapidly

These three issues have actually affected the fundamentals of various US stock companies. We can see signs of greater or lesser degree from the published company results, and further affected the profit expectations of US stocks.

In the process of the Federal Reserve's interest rate hike and pressure valuation process, the emergence of several factors led to a situation where US stocks lost their performance, causing Davis to double hit.

So, what is the overall situation of the domestic Internet industry, which has been under high pressure of antitrust and regulation for over a year? Which industries are still under pressure? What are some other highlights, let's take a look.

1. The overall situation of the domestic Internet industry: user dividends have peaked, and under anti-monopoly, they all show their ingenuity

The overall situation was mainly analyzed based on QuestMobile's April report, mainly targeting some changes in various domestic internet tracks throughout the current round of the epidemic.

First, let's look at the active daily average market for mobile internet. Compared with the beginning of the first round of the epidemic in '20, this round of the epidemic did not show a rapid increase in penetration rate and duration; there was a more moderate increase.

In terms of the 20-year epidemic, at the MAU level, Internet users have penetrated rapidly. In just 4 months, the number of users increased by 22 million, which is equivalent to releasing the last wave of Internet dividends. There have been no significant changes in '22. Basically everything that can be covered has been covered, further verifying the end of the internet dividend by penetrating new users. However, this doesn't mean that Internet companies don't have a chance, because different apps still have enough room to penetrate; it's just that they need to consider how to bring the company's own unique services and value to users, rather than washing up those blank Internet users.

Look at the length of useThis is also the same situation. Overall, the average daily time for a single user in '22 was 20 to 30 minutes higher than in '20. The peak caused by the 20-year nationwide lockdown did not occur in '22, and the length of time in '22 was more of a moderate increase.

MAU and the average daily length of time per user have both increased moderately, but when the two are multiplied, it is possible to derive the additional space added to the Internet. MAU in April '22 increased by 1.02% compared to December '21, the average daily time for a single user increased by 6.20%, and the total user market increased by 7.47%. It can correspond to the advertising market, live streaming, and games, which can actually bring about revenue growth.

Looking at each industry, if you also look at the comparison between 20 and 22, every industry sector has grown to varying degrees. I have to admit that the Internet has indeed further entered our lives under the catalyst of the epidemic.

Among them, MAU's outstanding monthly performance is the local lifestyle sector. The main reference here should be Meituan and local fresh food e-commerce and community group buying businesses. MAU increased by 34.7%, and monthly length increased by 48.4%. The average daily time spent on a single user in this section doesn't seem significant. More attention should be paid to MAU changes. Because people only use it when needed, the track's advertising revenue share is not too high, and the advertising format is not presented in the form of information flow.

Short videos have increased the most in user time, and we can also feel this in our daily lives, so advertising revenue for short videos has increased rapidly in the past two years. All year 21, bytes$ByteDance (FT0001)$The advertising revenue was RMB 280 billion (although the company refuted the rumor), which was $183 billion for the full year of 2020, an increase of 53% over the previous year.

The only decline was office software. The monthly length of time dropped by 33.8%, more because children did not take online classes and compared to the complete lockdown, this round of the epidemic spread.

II. Internet industry policy-level analysis: regulation is nearing its end, repair can be expected

Since 2021, the global market has continued to monitor anti-monopoly, data security, and personal privacy policies in the Internet industry, including China, Europe, and America. The market's risk appetite for the Internet industry as a whole continues to decline with the gradual implementation of regulations. From the decline in the expected growth rate to expectations about whether the industry is still worth existing at the worst, combined with various public opinion wars on soft technology and hard technology, etc., all put a lot of pressure on the stock price of China Internet as a whole.

However, we have discussed many regulations in the past. Basically, they have all been dealt with, and with the release of “Certain Opinions on Promoting the Standardized and Sustainable Development of the Platform Economy” and the occurrence of events such as the Politburo meeting of the Central Committee, the Financial Stability Conference, and the National Committee of the Chinese People's Political Consultative Conference (CPPCC) thematic consultations, judging from the level of the conference, it has been confirmed twice that the entire peak of Internet regulation has passed.

We've always discussed that we need to see the three bottoms appear: policy bottom, low expectations, and bottom performance

We believe that the two meetings of the Financial Stability Board and the Politburo Conference are the highest in terms of level. Looking back at some of the policies introduced one after another, none of them actually moved out of the framework proposed by these two meetings. It's just that each unit doesn't seem to know how to promote the healthy development of the platform economy; they only know how to fight hard. But the overall tone is getting better.

As for the latter expectations, which we have discussed before, the expectations for different industries are different:

▷ In the game industry, regular distribution of version numbers has been achieved

▷ E-commerce industry, logistics response. The Yangtze River Delta epidemic has been brought under control and has been achieved

▷ In the internet finance industry, the Ant Financial incident had an end, which was not realized

▷ In other service industries, the matter of DiDi has been decided, registration is open, and rumor has it that it will be realized

We can see that after the policy is finalized, expectations have actually begun to appear in many industries, indicating that everyone can begin to look forward to a process of gradual restoration of fundamentals and begin to see a reversal in expected performance at what stage.

According to this rhythm, along with the introduction of a series of measures for steady domestic growth and steady consumption, in fact, if you anticipate boldly, the inflection point in performance will occur in the third quarter. This is also one of the main logic of the market recently. The results for the first quarter are clear. The poor performance in the second quarter is basically certain, but it is only necessary to confirm the extent of the poor. Everyone is focused on how quickly the damaged performance can be repaired in the third quarter.

3. E-commerce industry: growth is slowing down, cost reduction and efficiency are showing results, and live e-commerce is improving

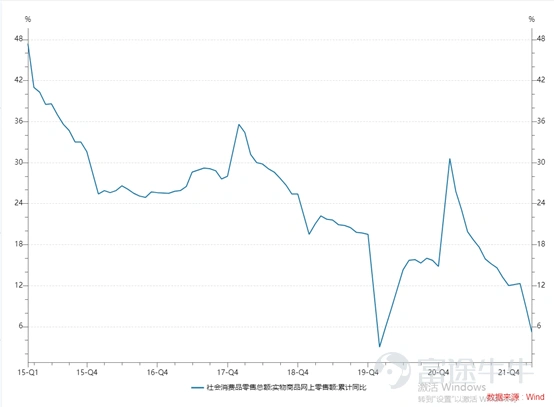

In the first quarter, the national consumption market didn't work. Social zero in March was 3.4 trillion dollars, and April was 2.95 trillion yuan. The sum of the two is equal to the overall data for January-April. Compared to the previous year, it was -7.17%, not to mention that this is probably the result after refinement.

Looking at online physical retail, the cumulative year-on-year for January-April was 5.20%. The growth rate fell to its lowest point outside the first outbreak of the epidemic, and continued to decline. If you look at April alone, the growth rate was -5%.

The market market is very poor. E-commerce is relatively better than the market through increased penetration, but it is still difficult to avoid the consequences of sedimentation. Therefore, judging from the GMV of various e-commerce companies in the first quarter, it was either a decline in GMV, or a decline in GMV growth in size.

▷Alibaba$Alibaba (BABA.US)$FY22Q4 Tmall and Taobao's GMV achieved a low single-digit decline. CMR remained flat year over year, and the monetization rate increased

▷JD$JD.com (JD.US)$Product sales revenue (also known as self-operated GMV) grew 16.62% year-on-year, compared to 22.10% in the previous quarter

▷Pinduoduo$PDD Holdings (PDD.US)$The annual GMVQ1 growth rate was 31.02%, compared to 46% in the previous quarter

▷Kuaishou$KUAISHOU-W (01024.HK)$The Q1 e-commerce GMV growth rate was 47.67%, compared to 35.67% in the previous quarter. Kuaishou acceleration reflects the reason why the company's fundamentals in the e-commerce sector have improved, and its size is relatively small. Q1GMV is 175 billion.

If we look for reasons from the top down, we can find that some are inevitable, and some have inflection points:

1. With the gradual increase in the penetration rate of physical e-commerce, the fastest growth period has actually passed. Next are areas that are more difficult to penetrate, such as fresh food and miscellaneous food

2. The overall macroeconomic problem is that consumption is too poor. The above data has already been reflected, leading to an unusual data where the growth rate is falling too fast. This part is avoidable; the core factor is the problem with the overall economic growth rate. The country's policy of steady growth and stable consumption has gradually been introduced; in fact, the bottom of expectations has already appeared

3. Logistics was interrupted in various regions due to the epidemic. With the end of the epidemic, logistics in various regions recovered, which helped merchants deliver goods and confirm revenue. An inflection point has now appeared

Therefore, combining the above three factors, one factor is unavoidable. The reflection is that in terms of performance, the growth rate of each e-commerce company's GMV will inevitably decline after reaching the trillion dollar level. This is already reflected in the valuation level, and everyone's valuations have declined. The inflection point of the other two factors has already appeared, so what is certain is that the end of May will be the bottom of the overall e-commerce sector's performance

From a revenue perspective, GMV's growth rate has declined, but each company is increasing its own take-rate to a greater or lesser extent, which is reflected in the revenue level that revenue can still maintain a better growth rate than the general market in the industry

▷ Alibaba's Chinese retail customer management segment revenue was 0% year over year vs. GMV fell by a single digit

▷ If Pinduoduo Q1 excludes 1P revenue, the revenue growth rate is 39.4% vs. GMV's growth rate of 31.02%. The take rate was 3.59% compared to 3.37% in the same period last year

▷ Kuaishou e-commerce revenue increased 54.64% year over year vs. GMV grew 47.67%. Although Kuaishou e-commerce's take rate has never been raised, it was 1.07%, compared to 1.02% in the same period last year

Another trend. What we need to pay attention to this quarter is that e-commerce companies no longer define themselves as e-commerce, but have become more retail companies with an omni-channel layout, including e-commerce in the far, middle and near market

▷ Alibaba's Taobao and Tmall are far away; Taocai cuisine is considered medium; Gaoxin retail is close

▷ JD Mall is far away, JD is close to home

▷ Pinduoduo's original business is far away; Duoduo grocery shopping is in the middle

▷Meituan$MEITUAN-W (03690.HK)$Meituan's Preferred Choice is China. Meituan Grocery Shopping and Meituan Flash Shopping are close

As mentioned earlier, it is difficult to grow after online physical retail accounts for zero of the head office and reaches a relatively high penetration rate. Mainly, it is difficult to increase the share of far-field e-commerce. Therefore, major e-commerce businesses have begun to penetrate midmarket e-commerce and near-market e-commerce, including fresh food and retail in the same city.

Therefore, the revenue of each e-commerce business should be viewed as a whole, reflecting the development of each business under an omni-channel layout. Far-field e-commerce provides cash flow and profits for midfield and near-field burnout. This phenomenon appears in every e-commerce company.

If you look at it as a whole,

▷ Ali's retail revenue in China increased 7% year over year, including direct management and others increased 14% year over year

▷ JD's retail revenue increased 17.08% year on year. Dada began and listed in the current period. Dada's revenue increased 21% year on year, JD Home GMV increased 74.4% year on year, and revenue increased 80.18% year on year

▷ After Pinduoduo Revenue proposed the 1P business, revenue increased 39.4% year-on-year, including revenue from trading services including Duoduo Grocery Shopping +90.7% YoY

▷ Meituan's new business revenue increased 47.02% year on year. Among them, Meituan Grocery Shopping's order volume in the first quarter increased 120% year on year, and the number of daily orders reached an all-time high. The number of Meituan Flash Shopping orders and GTV increased 70% and 80% respectively in the first quarter, and the average daily order volume in the first quarter exceeded 3.9 million

This part of the new business is losing money, so while seeing a high growth rate, we also need to pay attention to the most mentioned cost reduction and efficiency issues this quarter, how to control costs, and how to reduce losses. Here, we will directly analyze the cost reduction and efficiency issues of each company at the company level, because it falls on every business, and it is difficult to split it up.

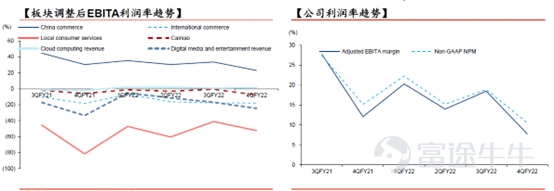

First, Ali himself. After China's commercial adjustment, the EBITA margin fell 7% year over year. According to the company's explanation, investment in Taocai and Taotte led to a decline. However, at the same time, the CFO mentioned during the conference call that losses caused by Taotte and Taocai declined month-on-month.

The other part is the local lifestyle service sector. After the adjustment, the EBITA margin decreased by 30% year on year. The company explained that the home delivery business, that is, the UE for Hungry and Taoshida, has clearly improved, mainly due to optimizing user acquisition costs and delivery costs.

As a result, Ali's adjusted EBITA for the quarter fell 30% year over year, and the margin dropped even more, from 12% to 8%.

The EBITA profit margin trend for other businesses is shown below

In Pinduoduo's case, first of all, the decline in the company's 1P business has led to a decrease in the company's share of low-margin business, and the overall gross margin has improved quite well. In the fourth quarter of last year, Tencent gave Pinduoduo a one-time cloud computing rebate, which led to Pinduoduo's gross profit reaching a remarkable new high. Taking seasonal factors into account, there was indeed a very significant improvement in gross margin. Assuming that the cost structure of the main site remains unchanged, CICC's Internet team estimated that Duoduo Grocery Shopping's gross profit for the quarter was 700 million yuan. Compared with the large-scale contraction compared to last year, the loss for the same period last year was comparable to that of Meituan, about 7 billion yuan.

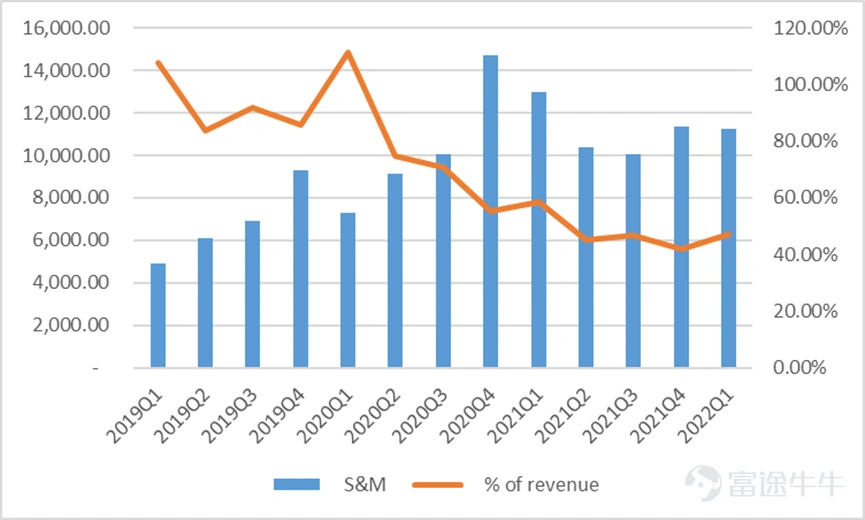

In terms of sales expenses, Pinduoduo maintained its own pace and did not show a very obvious downward trend. Instead, it also increased investment in marketing. The share of marketing and promotion expenses in revenue increased by 6% over the previous month.

R&D expenses also continue to rise, mainly due to the company's 10 billion agricultural research plan, and the company continues to invest in agricultural product cultivation, etc. Pinduoduo's investment in agriculture may not pay off very well, but given their investment in agriculture, supply chains, etc. are good when selling agricultural products, so buying Duoduo groceries can reduce losses much faster than Meituan. This is an advantage.

Therefore, after eliminating PDD's Tencent red envelope factor in the fourth quarter of last year and reducing investment in Duoduo Grocery Shopping Kaesong, Pinduoduo began to focus on the profit level. The profit margin was still relatively steady. The non-GAAP operating margin remained at 15%. It can be said that Pinduoduo was the first to get out of the process of reducing costs and increasing efficiency, stabilizing the company's financial structure to achieve growth in the company's performance.

In Kuaishou's case, e-commerce and advertising are either highly anticipated by the market or are Kuaishou's only growth drivers. Among them, the current advertising model is more mature. Let's talk about this in detail in the advertising section. Let's first analyze Kuaishou's e-commerce business.

First of all, in terms of revenue, Kuaishou's growth rate is really good. It is considered the highest among all companies' e-commerce businesses, mainly due to 2 points:

▷ The overall market space for live streaming is increasing. Compared with Kuaishou, Douyin's growth rate is higher. Open Source Securities expects Douyin's GMV to be 1.2 trillion yuan for the full year of 2022, an increase of 240% over the previous year.

▷ Currently, the GMV is still small. The GMV for the full year of 2021 was 680 billion, the year-on-year growth rate was 78.41%, and the Q1 was 175 billion, and the year-on-year growth rate was 47.67%

Although the growth rate and volume are not as good as Douyin, I have to admit that Kuaishou e-commerce is still developing rapidly, and the gap with Douyin is also due to differences in the total user market. According to Questmobile's estimates, the total user market for short byte videos is currently twice that of Kuaishou. Therefore, if we look at e-commerce GMV = total user time × conversion rate × GMV per order, it is easier to understand the gap in the middle.

In order for GMV to grow rapidly, Kuaishou's monetization rate has not been high, which helps merchants and consumers to establish stickiness first. Until now, the monetization rate of Kuaishou e-commerce is still around 1%. In contrast, Pinduoduo is at 3%, while Taobao and Tmall are close to 4 to 5%.

Therefore, Kuaishou e-commerce is definitely losing money. It is equal to the cash flow earned by advertising and live streaming to take losses from e-commerce. It is mainly used for R&D and sales expenses such as subsidizing merchants and consumers, building e-commerce logistics and capital flow systems, and building back-office and front-office systems. Therefore, this is also an important place for Kuaishou to reduce costs and increase efficiency. This is also one of the market's concerns about Kuaishou's performance this quarter. The growth rate cannot drop too fast, and at the same time, we see that the extent of losses is shrinking.

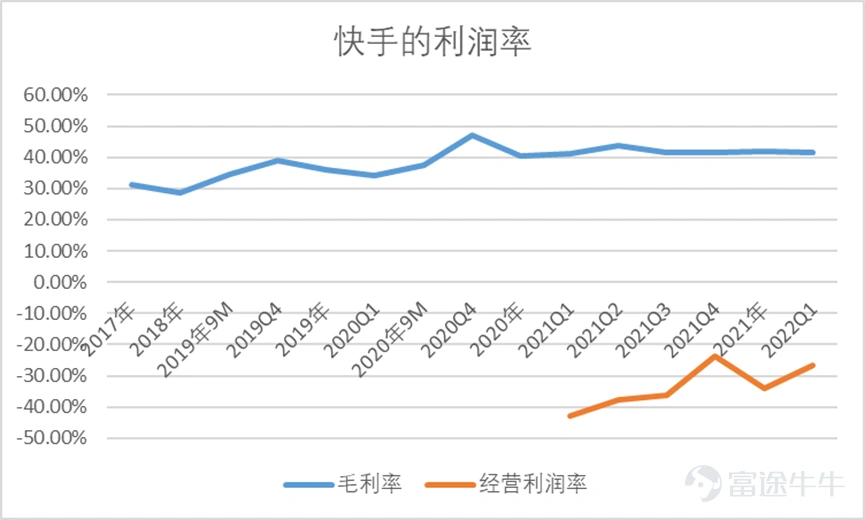

With the revenue share of each business basically stable, gross margin remained stable, but it can be seen that the operating profit margin improved quite clearly in the 1st quarter, narrowing from -42.85% in the 1st quarter last year to -26.79% in this quarter. Also, during the conference call, the company promised to reverse the non-IFRS operating margin this year.

Well, look at Kuaishou's business the other way around. With the company's ability to reduce costs and increase efficiency successfully, the current take rate just happens to be an opportunity for the company to quickly increase e-commerce business revenue, and it is also an opportunity for gross margin and revenue to increase at the same time.

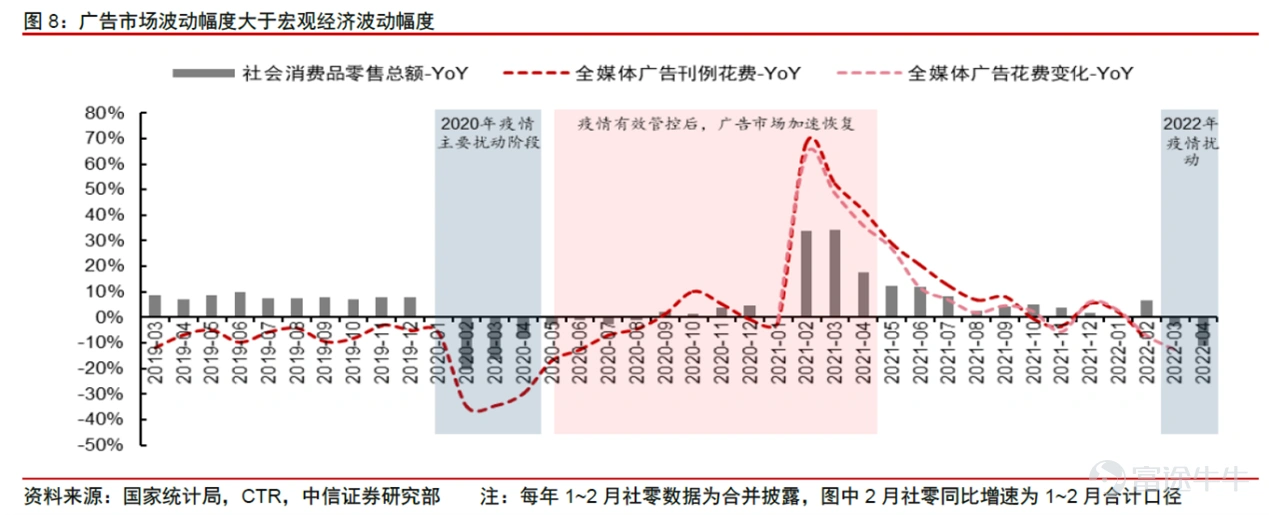

4. Advertising industry: continuing to benefit from the downturn in the economy

Through the calculation formula of Internet advertising, we can see that advertising revenue = DAU × average daily usage time per user × AD load × CPM. Currently, the overall volume of Internet advertising is basically only increased by AdLoad and CPM prices, because the number of Internet users has basically reached its peak.

▷ The overall TAM growth rate has declined. It is expected to be only about 10%, and the advertising market is growing in single digits

▷ The two dynamic increments are one less (number of DAUs and user time), and the other one is currently growing at a very slow rate because the length of time has basically reached its peak. Therefore, the Internet advertising market is greatly affected by macroeconomic growth

However, we also need to see that the penetration rate of internet advertising is still increasing, and there is room for growth in the advertising market. Because currently the ratio of TAM to China's GDP in the advertising industry is only 0.89% (2021), the US is 2.5%, and Japan is 1.6%

According to iResearch's report, e-commerce ads have the highest share of online advertising, which is expected to be 40.1% in 2021, while short video ads have the highest growth rate because user time is growing the fastest, and CPM prices are currently the highest advertising type.

Therefore, from the perspective of growth rate, Douyin and Kuaishou still have quite a bit of room to expand their advertising revenue, but the process with the highest growth rate has come to an end. Currently, only two short video giants have also grown in advertising volume. Douyin had advertising revenue of 280 billion dollars in '21. Although rumors have been refuted, this volume is expected to be about the same. Kuaishou's annual advertising revenue in '21 was 42.6 billion.

From the perspective of DAU x single user market = total user time, under the same adload and cpm situation, Kuaishou's advertising revenue should reach half of Douyin's, or 100 billion dollars. The difference between these is the difference in user spending power and recommendation algorithms. Kuaishou's advertising is not expensive.

However, the advertising industry is also the one with the most obvious marginal changes in the economic recovery process. In particular, marginal changes on the profit side will be particularly obvious:

▷ Internet advertising mainly determines the price by matching supply and demand between advertisers' advertising needs and advertising inventory

▷ There is not much room for growth in MAU and length of time per user of mobile internet, and the increase in advertising inventory is limited, resulting in limited supply-side growth of advertising inventory

▷ As the economy improves or expectations improve, demand increases and supply is limited, so it becomes a sellers' market, and prices soar

▷ The marginal cost of internet advertising is very low, because people use apps not to go up to watch ads, but they have their own needs

Therefore, the flexibility on the profit side is far higher than on the revenue side. Of course, the profit flexibility of offline advertising is not small. We can see from Weibo and Audience's revenue and profit YOY.

According to the May News Zero data released two days ago, consumption shows some signs of recovery. Overall social zero declined 6.7% year over year, better than market expectations of 7.1%. The online retail response is growing 7%. According to Kuaishou and Ali's sharing during the conference call, the company will still benefit merchants in the short term, so the e-commerce sector is expected to respond more slowly than the advertising sector. The recovery in consumption will directly lead to the release of profits in the advertising industry, so the bottom of advertising performance is in May, and growth resumed in June.

Therefore, the poor performance in the first quarter can actually be felt when the social network deteriorated in the first quarter. The second quarter was compounded by outbreaks in some core first-tier cities, which worsened the situation. In particular, e-commerce advertisements declined significantly due to the inability to ship and launch them:

▷Tencent$TENCENT (00700.HK)$Advertising revenue fell 18% year over year in the first quarter, with social advertising falling 15% and media advertising falling 30%. The commercialization of the video account is in progress. The current level of commercialization of video accounts is insufficient, which is the reason for lowering the gross margin of the advertising business. Therefore, returning gross margin to the previous level requires an increase in video channel revenue volume, which is expected to occur in Q4.

▷ Alibaba's advertising revenue is placed in the customer management sector, and it is expected to grow by a low single-digit year-on-year rate. The low single-digit year-on-year decline in the 2nd quarter, and the response rate was very fast. The response is expected in June. The 3rd quarter depends on the extent to which promotional fee measures have restored the consumption growth rate.

▷PDD's advertising revenue increased 28.68% year-on-year in the first quarter

▷Kuaishou$KUAISHOU-W (01024.HK)$Ad revenue increased 32.65% year over year in the first quarter, mainly due to DAU and Feed contributions. AD load and price are negative contributions due to weak demand. Recurring advertising was affected by more than 10% and less than 20% in the second quarter. The impact of external circulation was quite serious, mainly because advertisers were pessimistic about the future.

▷B station$Bilibili (BILI.US)$Advertising revenue increased 45.63% year-on-year in the first quarter, mainly contributed by the increase in the number of active users and the increase in length of time. The contribution of advertising ARPU ranged from 1.07 to 1.18 yuan, compared to 1.95 yuan in the fourth quarter of last year. It still shows that the decline in advertising demand has led to a decline in advertising prices. The company believes that the restoration period will be in the second half of the year.

Generally speaking, advertisements are divided into two categories. According to Kuaishou's definition, they are divided into internal circulation advertisements and external circulation advertisements.

Internal circulation refers to advertising within the ecosystem to facilitate transactions within the ecosystem. Basically, it is mainly e-commerce advertising. This area was repaired the fastest. Kuaishou and Alibaba's revenue both showed a relatively clear recovery in the second quarter, mainly to deal with the 618 promotion and active promotion after not selling for a period of time due to supply chain issues. External circulation advertising is placed by external advertisers within the ecosystem, such as games, brand advertisements, etc. This part is not easy to directly drive transactions to generate revenue, so the response speed will be slow. Typical examples are Kuaishou's own external circulation advertising and Station B advertising business.

But overall, we see several downstream industries in the advertising industry:

▷ The largest e-commerce, internal circulation advertising is already being repaired

▷ In the game industry, after version numbers are normalized, high-quality games will inevitably be accompanied by a high level of purchase volume, and the continuous buying behavior associated with long-term operation due to lack of editions

There is no doubt that advertising is being repaired. What we need to consider more at this point in time is which company has the greatest marginal effect. According to the analysis, it is still the first company in the e-commerce business sector to be promoted.

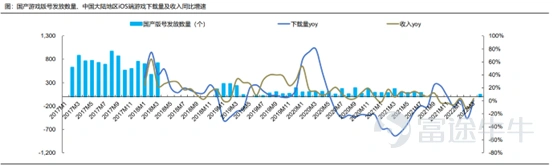

5. Game industry: the industry ushered in an unfreeze, and games went overseas to show results

The growth factors in the domestic game industry are whether versions are distributed or not, and the estimated number of editions. The overall trend is that there will be fewer and fewer editions, so the domestic market is already a stock market with a slow growth rate.

At the same time, the market share of leading manufacturers is gradually increasing, and competition for new games is particularly intense in the stock market. The market share of the two giants, NetEase and Tencent, reached 80% of the ban in 2021. Among the top 100 domestic iOS mobile games in '21, games that have been online for 5 years or more accounted for 43% of the overall turnover, and the trend is gradually increasing, mainly due to long-term games such as Wang Zhe Rongyao, Chicken Eater, and Dream Journey to the West.

After taking the dividends of the 2020 pandemic, the growth rate of the game market in '21 returned to single digits. In particular, the mobile game market recorded the lowest growth rate of 8% in history.

Also, look at the mobile game market revenue issue from two perspectives: user size and average revenue per user, or ARPU.

Mobile game users only increased by 2 million in '21, a year-on-year growth rate of 0.23%, and the total number of users reached 656 million. Considering the age distribution of users, this number of users has basically reached the ceiling in a short period of time. Of course, with the intergenerational changes, more and more people will become Internet natives, so the number of game users will definitely continue to increase. This is a big story for the next 10-20 years, so that's another story.

From the perspective of ARPU, ARPU is 344 yuan, and the growth rate is OK, 7.3% compared to the previous year. Therefore, from the trend in the number of users and ARPU, as well as the gradual reduction in the number of superimposed versions, it can be seen that the trend in the entire domestic game industry is to refine, expand, and explore more commercial opportunities for single users.

With the release of the version number at the end of April and the release of the second round of this year in early June, it indicates that the version number has returned to normal distribution, which has been suppressing the game industry, and the risk appetite of the game industry has gradually increased. However, the distribution of edition numbers cannot immediately boost the sales revenue reversal of the entire domestic game market. At the same time, it is compounded by the overall weakening of consumer spending to counter the pressure brought about by the overall game market.

The actual sales revenue of the Chinese game market in May was already the third consecutive month of year-on-year decline. In May, it fell 6.74% to 22.119 billion yuan. Among them, the main decline came from the mobile game market, which fell 10.85% year over year to 16.996 billion yuan. Two reasons:

1. Sales volume of many top games declined year over year

2. The streaming performance of new games is poor and cannot bring about significant growth

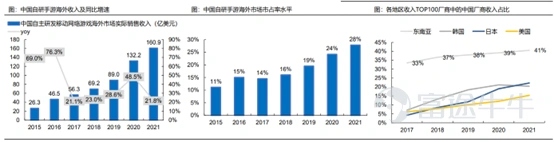

Therefore, in the past year, the theme of the game industry has been to go overseas and go abroad. Therefore, we are focusing on analyzing the overseas market, which is the incremental part of the game industry.

We see that the global game market will clearly grow faster than the domestic game market in '21 and in the next few years.

Among them, mature markets have entered Europe, America, Japan, and South Korea, mainly through the rise of ARPU. Among them, the US market is the most special, where ARPU and DAU both rise.

Emerging markets are growing through increased smartphone penetration, Southeast Asia, Africa, and Latin America.

Therefore, the mature market is currently the main position to go overseas. Because the ARPU there is high, even if the purchase volume cost is not low, through the excellent capabilities of domestic mobile game manufacturers, it can reach a very high LTV and achieve a good ROI.

According to Statista data, the size of the overseas mobile game market in 2020 was 59.9 billion US dollars, an increase of 24% over the previous year.

Statista expects the overseas mobile game market to reach US$99.7 billion by 2025, with a compound growth rate of 11% in 2020-2025

Currently, the overseas market share of mobile games developed by China is gradually increasing. By 2021, it has reached 28%. Among them, in markets with similar cultures such as Southeast Asia, Japan and South Korea, the market share is relatively high. Southeast Asia has reached 41%, and both Japan and South Korea are close to or above 20%. The total volume of turnover reached 16.09 billion US dollars.

According to estimates by Dongwu Securities, by 2025, if China's mobile game market share reaches 35% of Southeast Asia's market share in 2017 under neutral expectations, the corresponding two increases will be 18.8 billion US dollars, corresponding to 125.6 billion yuan.

Currently, among overseas manufacturers, the leading effect is still not particularly obvious. Overseas markets do not follow the pattern where domestic channels are king, because the fixed channels are mainly Google and Apple. Overseas, Tencent and NetEase don't have a particularly obvious advantage. As a result, CR3 and CR5 in the industry remain stable, and rankings such as CR10 are constantly changing.

Among a few of the more advanced game manufacturers that are currently overseas:

▷Tencent$TENCENT (00700.HK)$The goal of going overseas is overseas: domestic = 1:1. Currently, the share of overseas revenue in Q1 in '22 is 24%

▷NetEase$NetEase (NTES.US)$Overseas revenue target is 40-50% of overall revenue, and 22Q1 overseas revenue is 10%

▷37 Entertainment$37 Interactive Entertainment Network Technology Group (002555.SZ)$The goal is for the top three Chinese mobile game manufacturers to go overseas. Currently, overseas revenue is 34%, ranking sixth in May

▷ Perfect World$Perfect World (002624.SZ)$The target is also 1:1 overseas and domestic. Currently, the income from overseas is small

These four are the key companies we are focusing on. Each has its own strengths and weaknesses in going overseas. We will analyze the details in the company's own report. One point to keep in mind is that Outbound is not a direct global release. Going Overseas focuses on Glocal, or Global+Local. Different companies and different games need to be deeply involved in different regions. Therefore, when going overseas, we pay more attention to the European and American markets+the Japanese and Korean markets because of the high ARPU in these two markets.

According to the latest data from Overseas, the actual sales revenue for games developed independently by China was US$1,446 billion, down 5.80% from the previous month. The main reason for the decline was the decline in sales of some leading products.

This situation was actually partially reflected in the first quarter, mainly in the Tencent family. Mainly because the same period last year was when the overseas epidemic was the worst, the home led to a high base of game revenue. The game “PUBGM”, which has a relatively high market share, was greatly affected in the first quarter of this year. The year-on-year decline in turnover reduced Tencent's overall overseas sales growth rate in the first quarter.

As overseas social conditions return to normal and the dividends of going overseas disappear, in the short term, from the 2nd quarter to the 3rd quarter, the sailing circuit will be somewhat affected by this factor, offsetting some of the growth rate brought about by the increase in penetration rate.

We looked at the revenue of each company in the first quarter:

▷ Tencent's domestic game revenue fell 1% year over year to RMB 33 billion due to the impact of child protection measures on DAU and DAPU. Overseas revenue of 10.6 billion, up 4% year over year, mainly due to increased revenue from “Valorant” and “Clash of Clans”

▷ NetEase game revenue was 17.273 billion yuan, up 15.29% year on year. Old games performed steadily, and new products such as “Eternity” and “Harry Potter” brought in new volume

▷ Perfect World's game revenue for the first quarter was 1,973 billion yuan, up 23.01% year over year. Mainly, Tower of Magic was newly launched, with a turnover of 500 million yuan in the first month

▷gigabit$G-bits Network Technology (603444.SH)$Revenue increased 9.98% year over year, with little increase. The main increase was due to the fact that some new products were not launched in the same period last year, such as “Happy Thinking” and “Moore's Manor”. At the same time, the revenue of “Onitani Hachijiao” declined markedly year over year

In a situation where the share of overseas revenue is low, it is still quite obvious that companies are affected by domestic policies. The overall domestic market space is growing at a limited rate, which has led to a marked decline in the revenue growth rate of various companies. In a situation where there are fewer and fewer versions, the speed at which new products appear will inevitably be very slow, because every version is a very precious opportunity, and the company has no cheap trial and error opportunities, so they cut the product line drastically, or only take successful products from overseas to launch domestically. As a result, the possibility of innovation will be lower, there will be more products with industrialized assembly lines, and more products with a successful model of micro-innovation and iteration.

However, games belong to the content industry, and demand is being discovered rather than satisfied. Innovation can only create new demand. Until the original was unsuccessful, no one knew that open world mobile games could still have such great demand. Under the limited edition, bold innovation has become very extravagant. Only games that have gone through market verification and a mature commercialization system dare to go online and carefully iterate over the long term. Naturally, the result is that the ceiling of the entire industry can expand, but to a limited extent.

Well, going out to sea. Currently, going out to sea has rolled up, and this sea isn't that blue anymore; you can't just change the language of a game and go online directly. Going overseas to start deepening localization, and targeted promotion and operation and maintenance require a lot of time and money to gain experience. For game operations, it is more similar to factory management, and requires accumulation, so it's not a very easy task.

Therefore, in the sea circuit, I prefer manufacturers with successful experiences to eat most of the cakes that have been added to the 100 billion space, such as Tencent$TENCENT (00700.HK)$, NetEase$NetEase (NTES.US)$and 37$37 Interactive Entertainment Network Technology Group (002555.SZ)$。

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (11)

to post a comment

71

129