May 2022 “Howard Marx's Memorandum — The Same Rhyme of a Bull Market”

2022 Oaktree Capital Management, LP All rights reserved

Memorandum: To Oaktree Capital (Oaktree Capital) Customers

From: Howard Marks (Howard Marks)

[Theme: The Same Sound of a Bull Market]

While I love to cite lots of sayings and epigrams in my articles, there aren't many of them on my main list. One of my favorite quotes is generally considered to be from Mark Twain:”History doesn't repeat itself, but it's always strikingly similar. ” There is ample documentation showing that Mark Twain said the first half of the sentence in 1874, but there is no clear evidence that the latter half also came from him. Many others have expressed similar views over the years, including the 1965 psychoanalyst Theodor Reik (Theodor Reik), who said roughly the same meaning in an article entitled “The Unreachables” (The Unreachables). His sentences are richer in terms, but I think his expression is most appropriate:The cycle repeats, ups and downs, but the process of how things unfold is basically the same, with slight differences in the middle. Some people have said that history will repeat itself. This might not be entirely true; it's just strikingly similar. Events in investment history won't repeat themselves, but similar themes will recur, especially behavioral themes. This is exactly my field of research.

Over the past two years, we've seen dramatic examples of the “ups and downs” Reich wrote. What surprised me was that some of the classic themes of investor behavior played out over and over again. And they will also be the subject of this issue of the memorandum.

First of all, I would like to emphasize that this memorandum is not intended to assess the current possible direction of the market.After the outbreak of the epidemic in March 2020, the market bottomed out, and since then, the market's bullish behavior began; since then, both internal factors (inflation) and external factors (Ukraine) of the economy have experienced major problems; and the market has undergone a major adjustment.No one, including me, knows how these events will affect the future in general.

I'm writing this memo only to put recent events in a historical context and suggest some hidden historical lessons. This is very important becauseWe need to go back 22 years ago — before the TechNet bubble burst in 2000 to see how I think the real bull market and the resulting bear market ended.I think many readers probably haven't experienced this incident due to their late entry into the investment field. You might be asking, “Why did the market rise before the 2008-09 global financial crisis and the collapse caused by the 2020 pandemic?” In my opinion, the market movement before the two crises was gradual rather than a parabolic rise; it was not driven by excessive mental state of mind, and it did not push stock prices to crazy levels. Meanwhile, high stock prices were not the root cause of any of these crises. The former is due to the excessive development of the real estate market and subprime mortgage securities, while the latter is due to the COVID-19 outbreak and the economic lockdown policies adopted by the government to control the spread of the virus.

When I mentioned a “real bull market” above, I'm not referring to its standard definition, such as the definition in the investment encyclopedia:

• A period of continuous increase in the price of an asset or security in a financial market

• A situation where the stock price rose 20% after falling 20%

The first definition is too straightforward and doesn't reflect the emotional nature of a bull market, while the second one tries to use pseudo-accuracy. A bull market should not be defined as a percentage of price change. I think it's best described in terms of feelings, the state of mind behind them, and the behavior triggered by that state of mind.

(I started my investment career before the digital standards for bull and bear markets were formed, and I don't think this scale makes much sense. Take two recent news stories, for example. On May 20, the S&P 500 index fell more than 20% from its highest point; as a result, the Financial Times wrote on May 21, “The Wall Street stock market plummeted into a bear market yesterday...” but due to the subsequent rebound, the final total decline was just under 20%. The “New York Times” headline on the same day wrote, “The S&P 500 index fell... but did not enter a bear market.” Does it really matter if the S&P 500 fell 19.9% or 20.1%? (I prefer the old school definition of a bear market: mental torture.)

Excesses and corrections

Excesses and correctionsMy second book is Cycles. As you all know, I study cycles and believe in cycles. Over my years as an investor, I've gone through several important cycles (and learned from them). I believe that understanding where we are in the market cycle can shed light on future developments. However, as I reached about two-thirds of the writing of this book, I suddenly thought of a question I hadn't considered before:Why do we have cycles?

For example, if the S&P 500 index has been running in its current form since 1957, and for the past 65 years, its average annual return was slightly above 10%, why not get a 10% return every year? Updating the question I asked in my memorandum “Good Balance” (July 2004), why was its annual return between 8% and 12% only 6 times during this period? Why is it far from the average 90% of the time?

After thinking about this for a while, I found what I thought was the explanation: excessive and corrective.If the stock market is a machine, then it may be reasonable to expect it to perform steadily over the long term. On the contrary,I think the state of mind has a significant impact on investors' decisions and explains market fluctuations to a large extent.

When investors become very optimistic about the market, they usually think that (i) all investments will keep rising, and (ii) no matter how much they spend on an asset, someone else will buy it from them at a higher price (“stupid theory”).

Due to the high level of optimism:

• The stock price is rising faster than the company's profit, and the surge far exceeds fair value (Excessive rise)。

• Eventually, the investment environment became disappointing, and/or the unjustifiability of high prices became apparent, and stock prices fell back to fair value (amends), then fell below that value.

• The decline in prices intensified pessimism, a process that ultimately led to prices far below the value of stocks (excessive decline)。

• The buyers' buying operations on dips caused the sluggish price to rise back to fair value (amends)。

Excessive increases make returns above average for a period of time, while excessive declines make returns below average for a period of time. Of course, there may be many other factors at play, but in my opinion, “excesses and corrections” explain most of the reasons. In 2020-21, we saw some excessive upside, and now we see a correction taking place.

Bull market psychologyIn a bull market, favorable developments can lead to higher prices and boost investor sentiment. An optimistic mentality can induce aggressive behavior. Aggressive actions will cause prices to rise further. Higher prices encourage people to be more optimistic and take risks further. This spiral upward trend is the essence of a bull market. When this is going on, it feels unstoppable.

Asset prices experienced a typical collapse in the early days of the pandemic: for example, the S&P 500 index reached an all-time high of 3,386 points on February 19, 2020, then fell by one-third in just 34 days, and reached a low of 2,237 points on March 23. After that, due to the combined effects of several forces, the price rose sharply:

• The Federal Reserve cut the federal funds rate to near zero and announced large-scale stimulus measures with the Treasury Department.

• These actions have convinced investors that these institutions will do whatever it takes to stabilize the economy.

• Interest rate cuts have greatly reduced return expectations that make investments relatively attractive.

• Due to the combined effects of these factors, investors are forced to take risks that they had not been able to avoid until recently.

• Asset prices rose: By the end of August, the S&P 500 had recovered its losses and surpassed the February high.

• FAAMG (Facebook, Amazon, Apple, Microsoft, and Google), software stocks, and other tech stocks rallied sharply, driving the market higher.

• Ultimately, investors think — as they often do when everything is going well, they can expect the market to continue to rise.

The most important point about the mentality of a bull market (as quoted in the last point above) is that most people see rising stock prices as a positive sign of future development.Many turned optimistic. Relatively speaking, few people doubt that the increase so far may have been excessive, overdraining future returns, and heralding a reversal rather than a continuation of the trend.

It reminds me of another of my favorite sayings — one of the earliest I learned about 50 years ago — “The Three Stages of a Bull Market”:

• In the first stage, a few forward-looking people began to believe that the market would be better;

• In the second phase, most investors are aware that the actual situation is improving; and

• In the third stage, everyone thinks things will always get better.

What's interesting is that although the market changed from a depression in March 2020 to a boom in May — mostly thanks to the Federal Reserve, the attitude I most often saw during this period was one of doubt. And the question I get asked the most is: “If the environment is so bad — the pandemic is raging and the economy is stagnating — isn't it wrong for the market to rise?” It seems hard to find optimists. Many of the buyers were what my late father-in-law called “handcuff volunteers”: they didn't want to buy, but because they had to because the return on their cash was too low. And once the market starts to rise, people are afraid of missing out on opportunities, so they chase higher prices. Thus, the rise in the market appears to be the result of the Federal Reserve's manipulation of the capital market, rather than positive corporate development or the psychological stimulus of optimism. It wasn't until around the end of 2020 — when the S&P 500 rose 16.3% for the whole year and 67.9% from the bottom in March — that investors' mentality kept up with rapidly rising stock prices.

In my experience, the 2020 bull market was unprecedented because there was almost no first phase, and the second phase was very short. Many investors were still very hopeless at the end of March, but by late that year, they suddenly became highly optimistic.This reminds us that while some topics do recur, it is a huge mistake to expect history to completely repeat itself.

Reasons for optimism, superstocks, and new noveltiesThe crazy bull market reflects popular fanaticism about the stock market. In extreme cases, thoughts and actions are detached from reality. However, there must be factors that stimulate investors' imagination and cause them to abandon prudence, which will lead to this situation. Therefore, special attention should be paid to the factors that almost always drive a bull market: a new development, some kind of invention, or some reason for stock prices to rise.

By definition, a bull market is characterized by prosperity, confidence, trust, and a willingness to pay high prices for assets — all of which proved excessive in hindsight. History has generally shown that keeping these things in moderation is critical. Therefore, the rational or emotional basis for driving a bull market is often based on new things that cannot be measured by history.

That last sentence is very important. History has shown amply that when (i) the market shows bullish behavior, (ii) overvalued, and (3) unhesitatingly accepts the latest developments, the consequences are usually very serious. Everyone knows — or should know — that a parabolic stock market generally falls 20-50% after rising. However, these rising scenes occurred over and over again, reminding me of the so-called “self-anesthesia” theory I learned in high school English classes. Here's another quote I really like:

Contributing to... market frenzy are two other factors that few people have noticed in this day or in the past.The first is that the memory of financial markets is extremely short.As a result, the financial disaster was soon forgotten. Moreover, when the same or very similar situations happen again, sometimes after only a few years, they are hailed by a new, often young, and extremely confident generation as important innovations in financial markets and the larger economic world. In the field of human activity, there are few other fields where the significance of historical events is so unremarkable as in the financial world.Past experiences — if anyone else remembers them, are devalued as an instinct to escape reality because they can't understand and appreciate the beautiful things of the present.(John Kenneth Galbraith, A Brief History of Financial Fever, 1990 — highlighted)

I've shared this passage with my readers many times over the past 30 years — because I think it's a good summary of some important points, but I haven't read the behavior it describes before.I don't think investors are actually forgetful. They simply chose between knowing history and being careful, and a Libra who dreams of becoming rich. And the latter always wins. Memory, prudence, realism, and risk aversion only hinder this dream. For this reason, legitimate concerns are often overlooked when a bull market begins.

Instead, they usually seek theoretical grounds for valuations that exceed historical normal levels. On October 11, 1987, Anise Wallace (Anise Wallace) described this phenomenon in the New York Times in an article entitled “Why this market cycle is no different.” At this point, people are happy to accept optimism and find justification for abnormally high stock prices, but Wallace said this is unsustainable:

John Templeton (John Templeton), a 74-year-old mutual fund manager, believes the four most dangerous words in investing are “different this time.” In times of ups and downs in the stock market, investors always use this reason as a basis for their emotion-driven decisions.

In the coming year, many investors will probably use these four words again to defend the rise in stock prices. They should treat the rise in stock prices by referring to empty rhetoric such as “the check is on its way” (a kind of procrastination by the debtor). No matter what the broker or financial manager says, the bull market won't last forever.

It hasn't even been a year. Just eight days later, the world experienced “Black Monday,” and the Dow Jones Industrial Average fell by 22.6% in a single day.

Another explanation for a bull market is often the belief that certain businesses can guarantee a great future. This applies to the “Pretty 50” growth companies in the late 1960s; disk drive manufacturers in the 80s; and telecommunications, internet, and e-commerce companies in the late 90s.The development of these industries is thought to change the entire world every time, so the previous commercial reality did not limit investors' imagination and desire to chase high prices.And they really changed the world. However, their overvaluation, which was once considered reasonable, failed to be maintained.

In many bull markets, one or more groups are selected as what I call “superstocks.”Their rapid rise has made investors more and more optimistic. This rising optimism, in turn, pushes stock prices to rise continuously, and is usually a feature of the market cycle. Moreover, some of this positive sentiment and appreciation of securities will be further reflected in the prices of other securities (or all securities) in the relative value comparison and/or general improvement in investors' sentiment.

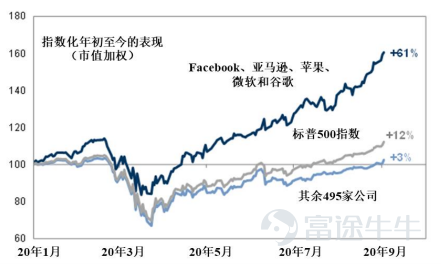

At the top of the list of companies that excited investors in 2020-21 was FAAMG (Facebook, Apple, Amazon, Microsoft, and Google), which had unprecedented market dominance and ability to scale. FAAMG's impressive performance in 2020 attracted investors' attention and supported the market's move towards a bull market. By September 2020 (that is, within six months), these stocks had nearly doubled from their March lows, and increased 61% compared to the price at the beginning of the year. In particular, these five stocks have significant weight in the S&P 500 index, so their performance made the overall rise of the index good, but this distracted attention from 495 other stocks that were clearly underperforming. The performance of superstocks made investors enthusiastic and turned a blind eye to the ongoing pandemic or other risks.

FAAMG's huge success has had a positive effect on tech stocks as a whole. Demand for technology stocks has soared, and as is often the case in the investment sector, strong demand encouraged and created supply. One of the most notable barometers is the attitude towards unprofitable companies' initial public offerings (IPOs). Prior to the TechNet bubble in the 1990s, it was relatively rare for unprofitable companies to do IPOs. This situation became the norm during the bubble, but then the numbers plummeted again. During the 2020-21 bull market, there was a sharp rebound in the number of unprofitable IPOs, as investors were very willing to fund technology companies' desire to scale up and biotech companies' drug testing expenses.

If companies with bright prospects can fuel a bull market, then emerging market developments are fueling the situation and driving these markets to rise excessively. A special purpose acquisition company (SPAC) is a typical recent example. Investors issue blank checks for these newly formed entities to carry out acquisition activities, and after meeting the attached conditions, they can recover the invested capital with profit: (1) if no acquisitions have been completed within 2 years, or (2) if the investors do not like the proposed acquisition. This looks like a “steady profit trade” (the most dangerous words in the world), and the number of SPACs has soared from just 10 in 2013 to 59 in 2019, 248 in 2020, and 613 in 2021. Some of these investments have been very profitable, while in other cases investors have also recovered their funds with profit. But there is no scepticism about this relatively untested innovation — driven by a bull market mentality, so many SPACs have been created, and regardless of whether their sponsors have the corresponding abilities, they will be richly rewarded by completing the acquisition... any acquisition.

SPACs that have completed acquisitions and exited since 2020 (all approved by their investors) now sell for an average price of $5.25, compared to an issue price of $10.00. This is a prime example, which ultimately proves that new things aren't as reliable as investors think — they've once again fallen into the trap of an “impossible to fail” killer. SPAC supporters believe that these entities are just an alternative way to bring a company to the public market, and I don't care if they are useful. My focus is on the extent to which investors can accept some kind of untested innovation during hot times.

Another development involving innovative elements is worth mentioning, as it shows how “new things” can contribute to a bull market.

• Robinhood Markets began offering commission-free trading of stocks, ETFs, and cryptocurrencies a few years before the outbreak of the pandemic. After the outbreak of COVID-19, it encouraged people to “trade stocks” as casinos and sporting events all stopped betting businesses.

• Millions of people have not lost their jobs, but have also received generous fiscal stimulus benefits, meaning that many people's disposable income has increased during the pandemic.

• Social news sites like Reddit are turning investments into a form of social activity when quarantined at home.

• As a result, the website attracted a large number of novice retail investors, many of whom lacked basic experience in investment analysis.

• Newbies are thrilled to worship a public figure who claims “the stock market will only rise.”

• As a result, the prices of many tech stocks and “meme stocks (meme stocks)” soared.

One last factor worth discussing is cryptocurrencies. Bitcoin supporters, for example, claim that it is versatile and that its supply is limited relative to potential demand. On the other hand, skeptics point out that Bitcoin lacks cash flow and intrinsic value, making it impossible to determine a fair price. Whichever party is proven right in the end, Bitcoin satisfies some of the characteristics of those who have benefited from the bull market.

• It's relatively new (although it's been around for about 14 years, most people have only learned about it in the last 5 years).

• Its price has soared significantly, from $5,000 in 2020 to a high of $68,000 in 2021.

• And, according to Galbraith (Galbraith), it is certainly something that previous generations “couldn't understand and agree with.”

• In all of these aspects, it fully satisfies Galbraith's description of something “enthusiastically embraced by a new, often young, and super-confident generation, as a great innovation discovery in the field of finance...”

Bitcoin is down slightly more than half from its 2021 peak, but the thousands of other cryptocurrencies that already exist have dropped much higher.

The spectacular performance of FAAMG, tech stocks, SPACs, memes, and cryptocurrencies in 2020 made this fascination even more fanatical and increased general optimism among investors.It's hard to imagine a full-blown bull market in the absence of anything unheard or unseen.“Something new and new” and the belief that “this time is different” are clear examples of the recurrence of the bull market theme.

Compete to the bottomAnother recurring bull market theme in different cycles is that bull market trends have a harmful impact on the quality of investors' decisions.Simply put, when a calm mind is replaced by hot optimism:

• Asset prices are rising;

• Greed triumphs over worry;

• Stop worrying about losing money and worrying about going short; and

• Risk aversion and caution disappear.

It is important to keep in mind that risk aversion and loss fears can keep the market safe and calm.However, these situations often collectively raise the market, causing careful investigation and thinking to disappear from the market, making it a dangerous place.

I explained in the 2007 memorandum back-to-bottom competition that when investors and capital suppliers have too much capital, they are in a hurry to put the capital into operation, so they bid too aggressively on securities and loan opportunities. Their aggressive bids weigh down potential returns, increase risk, weaken security structures, and reduce fault tolerance.

• Prudent investors who adhere to principles say, “I insist on 8% interest and strong contracts.”

• The competitor answered, “I can accept 7% interest and ask for fewer contracts”

• The most unruly investors who don't want to miss out on opportunities say, “I can accept 6% interest and no contract required.”

This is “bottom to bottom competition.” That's why it's often said, “The worst loans are made at the best of times.” When people are saddened by recent losses and are worried about losing money again, this is something that is unlikely to happen.It is no coincidence that the Federal Reserve's massive response to the global financial crisis ushered in a record 10-year economic recovery and stock market rally, and the following phenomena that followed:

• Loss-making companies ushered in a wave of listing;

• Record issuance of sub-investment grade securities (including high-risk CCC grade bonds);

• Large amounts of debt issued by companies in highly volatile industries (such as technology and software) that lenders may be unable to avoid during prudent periods;

• The valuation multiples of mergers and acquisitions continue to rise; and

• Risk premiums continue to fall.

The favorable developments also encouraged the use of leverage. Leverage can amplify gains and losses, but in a bull market, investors think gains are inevitable and ignore the possibility of losses. Under these circumstances, few see a reason not to borrow — through extremely low interest costs — to increase the rewards of success. However, investing in increased debt at high prices during an upward cycle is not a recipe for success. When things get bad, leverage becomes a negative factor. Moreover, when investment banks issue debt at the end of the cycle, they are unable to distribute it to buyers, and the debt issuance process comes to a standstill. The debt “hanging” on a bank's balance sheet is usually a “canary in a coal mine,” a sign of what is about to happen.

Since I believe in the enduring investment motto, it is very appropriate to cite what I think is most relevant to the different cycles of investor behavior: “Wise people start; fools end. ” In the first phase of a bull market, when prices were low due to widespread pessimism (such as during the 2008-09 global financial crisis and early COVID-19 in 2020), those who bought were likely to reap substantial potential returns with minimal risk: the prerequisite was to have the capital and courage to invest.But when the bull market heats up and impressive returns fuel investors' optimism, the characteristics of reaping returns are urgency, recklessness, and risk taking. In the third phase of the bull market, aggressive buying by new entrants allowed the bull market to continue for a period of time. Prudence, selectivity, and discipline didn't exist when they were needed most.

Notably, investors who are in a good mood and are rewarded for taking risks generally don't discern investment opportunities. Investors not only see some cases of “new things” as inevitable that they will succeed, but in the end they think everything in this field will perform well, so there is no need to make a distinction.

For these reasons, “bull market mentality” is not a compliment. It means unsuspecting behavior and high risk tolerance, and investors should be worried rather than encouraged.As Warren Buffett said, “When other investors are less careful, it's also when we should be more careful.” Investors must know when a bull market mentality dominates and take the necessary cautious stance.

The pendulum swingsA bull market is not born out of thin air. The reason why winners in every bull market can be winners stems from a simple truth: their earnings are supported by some truth. However, the bull market I described above is very vulnerable because it often exaggerates advantages and pushes securities prices to excessive levels. Keep in mind that the pendulum won't go up forever.

In a memo to “On the Couch” (January 2016), I wrote, “In the real world, things generally fluctuate between 'pretty good' and 'not that good'. But in the investment world, people's perceptions often fluctuate between 'flawless' and 'hopeless'.” Serious excesses are one of the key characteristics of investor behavior. During a bull market, investors believe that something difficult, unlikely, and unprecedented will definitely happen. However, in a less optimistic period, favorable economic news and “profits exceeding expectations” will not encourage asset purchases, and short breaks will no longer make investors anxious. As a result, we see no will to stop skepticism, and our state of mind quickly shifts to negativism.

The key is that investors can interpret almost any piece of news as positive or negative news based on the way the news is reported and their emotions.(Here's one of my favorite comics of all time; although it was published many years ago — think about the meaning behind the various media reports — it's clear that this text is relevant at the moment.)

![2022 Oaktree Capital Management, LP All rights reserved Memorandum: To Oaktree Capital (Oaktree Capital) Customers From: Howard Marks (Howard Marks) [Theme: The Same Sound of a Bull Market] While I love to cite lots of sayings and epigrams in my articles, there aren't many of them on my main list. One of my favorite quotes is generally considered to be from Mark Twain:”History doesn't repeat itself, but it's always strikingly similar. ” There is ample documentation showing that Mark Twain said the first half of the sentence in 1874, but there is no clear evidence that the latter half also came from him. Many others have expressed similar views over the years, including the 1965 psychoanalyst Theodor Reik (Theodor Reik), who said roughly the same meaning in an article entitled “The Unreachables” (The Unreachables). His sentences are richer in terms, but I think his expression is most appropriate:The cycle repeats, ups and downs, but the process of how things unfold is basically the same, with slight differences in the middle. Some people have said that history will repeat itself. This might not be entirely true; it's just strikingly similar. Events in investment history won't repeat themselves, but similar themes will recur, especially behavioral themes. This is exactly my field of research....](https://nnqimage.futunn.com/4be3b204-c776-46fd-86a5-acae8a8daf1a.png/big?imageMogr2/ignore-error/1/format/webp)

“Today on Wall Street, news of interest rate cuts will push the stock market up, but then the market will fall because investors expect a low interest rate environment to lead to inflation; later, as investors realise that low interest rates may stimulate the sluggish economy, the market will rise again; eventually, the market will fall again as investors worry that the overheating economy will cause interest rates to rise again.

” As I mentioned before, the “from flawlessness to despair” process, the hustle and bustle of speech is always reversed. While the arguments supporting a bull market aren't so absolute, investors will see it as unbreakable when everything is going well. And once some shortcomings in the argument begin to appear, it will be completely rejected.

• In the optimistic period (a year ago), people who are optimistic about technology stocks said, “You must buy growth stocks because they have decades of potential for profitable growth.” But now, after the market plummeted, what we're hearing is, “Investing based on future growth potential is too risky. You should stick to investing in value stocks because they have a definite present value and are reasonably priced.”

• Similarly, during frenzied times, investors involved in initial public offerings of loss-making companies say, “There's nothing wrong with companies reporting losses. They have a valid reason to invest money to scale up.” However, in the current period of adjustment, many people are discouraged, “Who would invest in unprofitable companies? They are simply money shredders.”

People who rarely follow the market might think that asset prices are determined solely by fundamentals, but this is certainly not the case. The price of an asset depends on fundamentalsAnd people's perceptions of these fundamentals.Therefore, changes in asset prices depend on fundamentals and/or changes in people's views on fundamentals. Company fundamentals are theoretically affected by so-called “analysis,” and possibly even predictions. On the other hand,Attitudes towards fundamentals are psychological/emotional, are not determined by analysis or prediction, and can change more rapidly and drastically.There are also some sayings reflecting this phenomenon:

• A balloon can be deflated much faster than it is blown.

• Things will take longer than you think to happen, and once they begin, they will develop faster than you think.

As for the second adage, in my experience, we often see positive or negative fundamental developments that continue for quite some time, but stock prices don't respond. But then a tipping point was reached — probably for fundamental or psychological reasons, and the entire cumulative effect was suddenly reflected in the price, and sometimes overreacted.

What will happen then?Bull markets don't treat all industries equally. In a bull market, as I mentioned earlier, optimism is heavily concentrated in specific sectors, such as “emerging industries” or “leading stocks.” These stocks rose the most, became a symbol of the bullish market during the period, and attracted more buying. The media paid the greatest attention to these industries, thus extending the course of the bull market. FAAMG and other tech stocks are the best examples of this phenomenon in 2020-21.

It goes without saying, but I still want to explain that investors who hold large numbers of leading securities have performed very well in every bull market. Fund managers who are smart enough or lucky enough to invest in these securities get the highest returns when optimism dominates, and get on the front pages of newspapers and TV shows.In the past, there was no shortage of people in the investment community who became famous because of a chance to make a correct prediction. For fund managers who are smart or lucky enough to hold heavy positions to lead the bull market, this effect is doubled.

However, stocks that rise the most during a bull market usually experience the biggest decline during a bear market. The adage applied here comes from the real world, but it doesn't affect its relevance: “Success or failure always happens;” “there must be a rise and fall;” and “the higher you climb, the heavier you fall”:

• A technology equity fund rose as much as 157% in 2020, from silent to prominent. However, the fund lost 23% in 2021 and fell 57% again so far in 2022. If you invest $100 at the end of 2019, it would be worth $257 a year later, but now it's down to $85.

• Another technology stock fund with less volatility, rising 48% in 2020 but falling 48% thereafter. Unfortunately, a 48% increase and then a 48% decline ultimately resulted in no change, but a net loss of $22 for every $100 invested.

• The third technology stock fund rose by an impressive 291% in the first year, but fell 21%, 60%, and 61%, respectively, in the following three years. If you invest $100 at the beginning, the final value is $43, and the next three years are down 89% from the impressive performance of the first year. But be careful: the current bull/bear market process is less than four years old. Note that the results I'm quoting occurred in 1999-2002, during the last time the tech bubble expanded and burst.

I'm telling these stories only as a reminder that history follows the same path. Earlier, I mentioned Robinhood, the pioneer of commission-free trading. It epitomizes the 2020-21 bull market. Robinhood went public in July 2021 at an issue price of $38, and its share price soared to $85 in the following week. Now its stock price is only $10, down 88% from its highest point in less than a year.

But the average performance of the stock market isn't that bad, is it? Even the extremely tech-heavy Nasdaq Composite Index “only” fell 27.4% in 2022. One of the characteristics of this bull market is that stocks of large companies (that is, stocks with the highest weight) performed best, supporting the rise in the index. Just imagine what that means for the rest of the stocks; 22% of NASDAQ shares are down at least 50%. (Data as of May 20 here and below):

Here's how some well-known tech/digitalization/innovation stocks I randomly selected fell from their highest points. Perhaps there are some of these stocks, and when they were at their peak, you were once bothered by not buying them:

PayPal -57%

BeyondMeat -63

Coinbase -74

Salesforce -37

Carvana -86

DocuSign -50

Moderna -46

Netflix -69

Shopify -74

Spotify -54

Uber -44

Zoom -51

average -59%

Assuming you still believe that market prices are determined by wise investors' consensus on fundamentals, if that's true, then why are these stocks falling so much? Do you really think the value of these businesses has been reduced by more than half in the past few months? This series of questions made me think about other things all the time. During periods of maximum fluctuation in the stock market, Bitcoin usually showed a trend in the same direction. Are there any fundamental reasons for the correlation between the two? The same question applies to international market correlations: when Japanese stocks open sharply lower, European and US stock markets tend to follow the decline. Moreover, it sometimes seems that the US stock market will drive the Japanese stock market down. Are the fundamentals of these countries relevant enough to be a reason to follow this trend?

My answer to all of these questions is “no.” The common thread is not fundamentals: it is a state of mind, and when the latter undergoes significant changes, all are similarly affected.

lessons learnedWhat matters most when it comes to investing is not what events happened in a specific period, but what we can learn from these events. We can learn a lot from 2020-21 and the cycle that followed the same rhythm before 2020-21. In a bull market:

• Optimism is built around excellent performance.

• The impact of the rise is strongest when it starts when mentality and prices are in a particularly low position.

• A bull market mentality is accompanied by a lack of sense of worry and a high level of risk tolerance, leading to very aggressive behavior. Take risks and reap rewards, while ignoring the need for thorough due diligence.

• High returns reinforce confidence in new, unlikely, and optimistic things. When people are convinced of the merits of these things, they often come to the conclusion that “nothing is too expensive.”

• Once these effects (and prices) reach an unsustainable level, they will eventually cool down.

• Overhanging markets are vulnerable in the face of external events, such as the Russian-Ukrainian conflict.

• The assets that have risen the most, and the investors who have heavily invested in them, often suffer painful reversals.

Over the course of my career, these themes have come up countless times. Not once was it based solely on fundamentals. Instead, they are mostly due to psychological factors, and the way mental states operate is unlikely to change.This is why I am convinced that as long as humans participate in the investment process, these phenomena will happen over and over again.

Also, we need to note that since market ups and downs are mainly driven by mental states, it is clear that market trends can only be predicted when prices are at unbelievable peaks or troughs.

May 26, 2022

Important Legal Information and Disclosures

This material expresses the author's views as of the date indicated, and such views are subject to change at any time without notice. Oak has no responsibility or obligation to update the information contained in this material. Furthermore, Oak does not state that past investment performance is an indicator of future performance, and you must not make such assumptions. In fact, whenever there is an opportunity to profit, there is also a possibility of loss.

This material is for informational purposes only and must not be used for any other purpose. The information contained in this material does not constitute or be construed as an offer to provide consulting services or an offer to sell or solicit the purchase of any securities or related financial instruments in any jurisdiction. Some of the information contained in this material relating to economic trends and performance is based on or taken from information provided by independent third party sources. Oaktree Capital Management, LP (“Oak”) believes the source of the information obtained is reliable, but cannot guarantee the accuracy of the information, nor has it independently verified the accuracy or completeness of this information or the assumptions made based on it.

All or any part of this material (including the information contained in this material) may not be copied, reproduced, republished, or published in any way without Oak's prior written consent.

To the extent that this material or part of its content is in Chinese, such Chinese translations are for reference only, and if there is any difference between the Chinese translation and the English manuscript, the English manuscript shall prevail. Oaktree Capital (Hong Kong) Limited is available in English for this material. Oak, its affiliates, or any of their respective officers, partners, employees, affiliates, shareholders or agents are (i) not responsible for any inaccuracies, errors, or omissions in the translation of this material, and (ii) have no obligation to notify any recipient of any inaccuracies, errors, or omissions in the translation.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (5)

to post a comment

47

172