新一輪制裁來襲,俄烏局勢如何演變?

Bain: What kind of crisis will the conflict between Russia and Ukraine bring to the energy and commodity sectors after the outbreak.

Summary: If the conflict continues, the world trade map will be completely reshaped.

For most companies, when dealing with the crisis caused by the Russia-Ukraine conflict, a crucial part is making their business, operating models, and supply chains more resilient.

Executives' management styles have become increasingly cautious, shifting their focus from traditional indicators like reducing costs and increasing efficiency to enhancing resilience. The company's governance motto is gradually shifting from 'seize the opportunity' to 'better safe than sorry.'

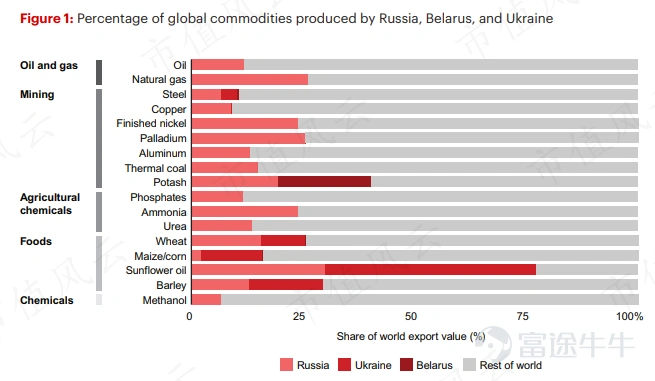

But for many companies, the first step in response is to understand the specific impacts on the supply side, including what goods Russia, Belarus, and Ukraine primarily supply to the world.

From the chart, it can be seen that the commodities supplied by the three regions mainly focus on crude oil, natural gas, ores, pesticides, and grains.The top three items with the highest proportion of exports are sunflower seed oil, potash, and natural gas.

The shortage of commodities has led to soaring prices, causing downstream customers, especially in industries heavily reliant on the import of these commodities such as manufacturing, energy, and textiles, to suffer greatly.

The broad coverage of industries involving commodities such as oil, natural gas, and food has led to a synchronous increase in prices affecting the entire society's consumer goods, ultimately causing all consumers to bear the cost.

The sharp rise in everyday consumer goods has significantly increased household expenses for the public, prompting the government to introduce a series of economic stimulus plans, tax reductions, and other measures to alleviate the pressure on people's lives. The rapid changes in regulatory policies also force companies of all sizes to constantly adjust their crisis response strategies.

Bain & Company has analyzed the specific impact points from several perspectives.

1. Soaring prices of commodities

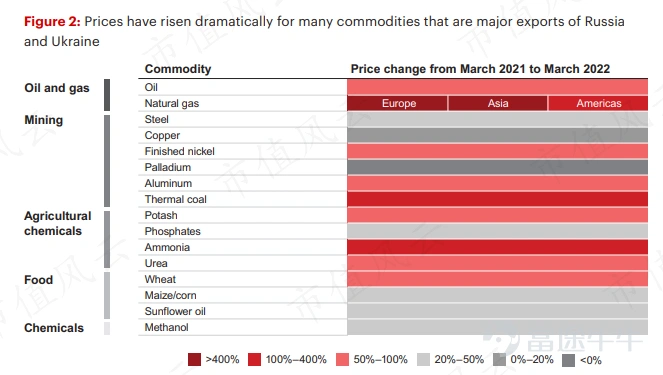

From March 2021 to March 2022, prices of major commodities exported from Ukraine and Russia have sharply increased. Among them, the most dramatic price increases were in oil and natural gas, with price rises to Europe and Asia exceeding 400%, and price increases to the United States ranging from 100% to 400%. Other commodities with price increases between 100-400% include thermal coal and ammonia, while wheat, aluminum, potash, among others, have also seen significant increases.

Other commodities with price increases between 100-400% include thermal coal and ammonia. In addition, wheat, aluminum, potash, and other commodities have also seen notable increases.

In fact, every commodity faces different levels of risk under the Russian-Ukrainian conflict, but at the same time, the new environment has also created new opportunities for the company. Based on the degree of economic impact, we will focus on analyzing three commodities: natural gas, oil, and wheat.

1. Natural Gas

Europe imports 60% of its natural gas from Russia, and for Russia, exports of natural gas to Europe account for 75% of its total natural gas exports.

In response, the European Union immediately proposed to reduce its dependence on Russian natural gas by more than half to quickly respond to sanctions. This proposal not only reflects Europe's concerns about energy sanctions but also significantly increases Europe's dependence on liquefied natural gas in the spot market, further pushing up the price of liquefied natural gas.

This also affects Europe's power generation model, with more countries possibly deciding to slow down the pace of closing nuclear power plants while trying to accelerate the construction process of renewable energy generation, although wind power, solar power, and other new energy generation methods cannot perfectly replace gas power without supporting scale energy storage.

Furthermore, replacing natural gas with coal or oil to reduce dependence on Russian natural gas may increase greenhouse gas emissions, leading to a setback in Europe's environmental protection progress.

High natural gas prices will also lead to a decrease in demand, especially for European industries with high natural gas consumption. However, it also provides more opportunities for lower-cost manufacturing industries in developing countries, especially those regions that can export to Europe.

Nevertheless, even so, it is difficult for Europe to reduce the proportion of its dependence on Russian natural gas to below 50%, meaning the demand for Russian natural gas will still be maintained at 50 billion to 70 billion cubic meters per year.

However, at the same time, the Russian government will also lose funding from natural gas and oil trading, although this income only accounts for about 7% of Russia's total GDP, it has a high impact of up to 40% on the overall Russian government budget.

Therefore, it can be said that both sides actually hope to see the natural gas trade continue to be maintained, at least to fulfill the existing contracts, which means that there is at least 5 years before the overall situation is completely disrupted.

As a result, the expectations for the winter of 2022-23 will become particularly severe, the potential threats make the crucial energy of natural gas even more fragile in the already tight market, with increased volatility and a substantial rise in premiums.

2. Crude Oil

Russia supplies 7.8 million barrels of crude oil and corresponding refined oil products daily, two-thirds of which flow to countries that already support sanctions against Russia.

In fact, even before the Russia-Ukraine war began, the price of oil had already increased during the post-pandemic economic recovery period, with the price per barrel rising from $54 in January 2021 to $74 in December 2021. After the conflict erupted, the price per barrel soared to over $110.

If Russia, as a major oil producer, continues to stay out of the market indefinitely, oil prices could be even higher. However, it is unlikely that Russia will completely withdraw from this opportunity-filled global market.Oil trade can be easily sanctioned, but the sanctioned oil will find new ways to re-enter the market.

Based on this, one possibility is that Russia's oil exports could decrease by 1 million barrels per day - a quantity that would be more easily accepted by the global market. In reality, the US and the EU have many ways to bypass sanctions, which could result in low- and middle-income countries purchasing Russian oil at a discounted price.

However, in a more extreme scenario, up to 4 million barrels of oil could be sanctioned daily.

Simultaneously, due to the potential withdrawal of Western capital and major energy companies from Russia, new foreign patents and hardware devices may no longer be imported into Russia. As a result, with the wear and tear of existing equipment and depreciation, even without direct sanctions, the supply of the entire oil industry will diminish over time.

Chicago SRW wheat

Russia and Ukraine play crucial roles in the global food supply chain. In addition to exporting essential fertilizer ingredients such as ammonia, phosphates, and potash globally, the combined wheat production of these two countries accounts for about 14% of the world's total, with their wheat trade representing approximately 1/4 of the global total.

The main importers of corn in North Africa and the Middle East, such as Egypt, where 60% of the national wheat consumption is imported, and 80% of these imports are from Ukraine or Russia.

Hence, Egypt's wheat prices have already risen by 40%-60% this year. After the sanctions begin, countries like Egypt will be forced to buy wheat from the international market at higher prices, further driving up the price of wheat.

Shifting demand from wheat to soybeans, barley, corn, and other crops will lead to a surge in prices for other commodities. If the conflict continues, it will affect global farmers' planting decisions in the next sowing season, thereby continuing to have a chain effect on the prices of these crops.

And the price fluctuations of commodities such as chicago srw wheat can actually impact a wider range of unpredictable industries. When a company is stuck in long-term supply chain shortages and has to invest far beyond planned costs to solve these issues, the impact may become increasingly significant.

For example, a palladium shortage can affect the cost and output of converters, thereby impacting the entire autos industry. Therefore, not only the energy and natural resources industry, but actually all industries in society, including manufacturing, technology, retail, and consumer sectors, need to actively prepare for the uncertainty brought about by this conflict.

Passive impacts at the macro level.

The drastic fluctuations in commodity prices and continuous supply chain shortages will accelerate the already high level of inflation before the conflict erupts. In this case, consumers will also reduce non-essential spending, and central banks around the world will begin to raise interest rates under immense pressure.

As investors worry about conflict escalation and economic downturn, financial market volatility will intensify, and capital inflows to Eastern Europe will decrease. More pessimistically, the issue of liquidity tightening may also escalate.

Under the dual pressures of deteriorating financial conditions and reduced consumption, governments around the world may be forced to take more economic stimulus measures, similar to those taken during the outbreak of the Covid-19 pandemic. However, unlike before, the persistently high commodity prices may dampen the recovery brought about by these economic stimulus measures.

Impact on policy and technology levels.

Sanctions and trade interruptions will also reshape geopolitical landscapes. To boost crude oil inventories, Europe and the USA have re-established cooperation with countries previously excluded from the trading map (such as Venezuela, Iran, etc.). Therefore, if the conflict continues, the international trade landscape will be completely reshaped, but premiums will also continue to exist.

The government will also take more intervention measures to reduce the negative impact from conflict regions, especially for countries heavily dependent on energy imports from conflict areas. The EU's REPowerEU initiative (as shown in the figure below) is an example, aiming to accelerate the construction speed of new energy infrastructure.

For private companies, investors, and consumers, there is a greater inclination to further strengthen scrutiny of energy and supply chain issues. At the same time, there will be a significant increase in focus on cybersecurity. After all, in a fragmented world, increasing investment in protective measures is necessary.

As an aside, last year, Cloudflare (NET.O), a network security giant that Wind Cloud has covered, along with the entire network security sector seem to have unfavorable stock price trends this year. However, based on Bain's analysis of cybersecurity issues mentioned earlier, perhaps under the outbreak of the Russia-Ukraine conflict, this sector may see new opportunities?

Author: Baby

Disclaimer:

This report (article) is an independent third-party research based on the public nature of listed companies and the information disclosed by listed companies according to their legal obligations (including but not limited to interim announcements, periodic reports, and official interactive platforms). The information and opinions contained in the report (article) aim to be objective and impartial, but the accuracy, completeness, and timeliness cannot be guaranteed. The information or opinions expressed in this report (article) do not constitute any investment advice, and Market Dynamics does not assume any responsibility for any actions taken based on the use of this report.

How to choose a company?

How to detect financial fraud?

What indicators should be considered when analyzing a company?

Value investing, most people have heard of it, only a few people master it.

Fengyun has compiled the most detailed and comprehensive "Value Investing System Panorama", guiding you through the professional investment analysis mindset, avoiding stock market pitfalls, and discovering good companies.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

7

6