美債收益率持續攀升,美股將如何演繹?

Bosch Investment Class|Read an article about US bond yields that “shocked” the market

Recently, one of the words investors have heard the most is “US bond yield.” The 10-year US Treasury yield continuously exceeded 2.5% and 2.8%. The global stock market was affected by this, and all showed significant fluctuations. The rise in US bond yields appears to be the “main culprit” of the market decline. What exactly is the US Treasury yield? What impact does its rise and fall have on the financial market? Today we're going to have a chat with all of you.

What is the US Treasury yield?

US bonds, or US Treasury bonds, are national bonds issued by the US Treasury on behalf of the government. Generally speaking, America's IOUs to borrow money from around the world are treasury bonds. Dollar endorsements are the greatest credit protection for US bonds, so US Treasury bonds are regarded by the market as risk-free bonds.

The US government borrows money through fixed term medium- and long-term bonds (such as 2-year, 5-year, 10-year, and 30-year terms) issued at a fixed interest rate determined by the current interest rate in the market at the time the bond was issued. Generally speaking, the longer the maturity period, the higher the coupon rate, because the longer the period, the greater the risk of uncertainty, the higher the risk premium as compensation.

The yield on US bonds refers to the return on earnings obtained from holding a bond until the agreed period. It depends on the face value of the bond, interest, and current bond market price. Generally, for bonds that have already been issued, the interest and face value are fixed, then the yield to maturity of the bond is negatively correlated with the bond price, that is, the bond yield rises and the bond price falls. 10-year US bonds are the most active bonds of all maturities, so the 10-year US bond yield is widely recognized as a “risk-free return”. This not only determines the lower limit of returns on various types of assets, but is also regarded as an “anchor” for global asset pricing.

US bonds are traded around the clock, so prices have always fluctuated. From a macroeconomic perspective, the steady rise in US bond yields represents an improvement in the economic situation. Selling off US bonds lowers prices and catalyzes higher US bond yields; lower US bond yields indicate that the economic situation is serious, and everyone is investing in risk-free treasury bonds.

What impact will rising US bond yields have?

Given the linkage of global financial markets, rising risk-free returns (using 10-year US Treasury yields as an observable indicator) will affect asset pricing in global financial markets through capital flow channels and market sentiment channelsThis includes bonds, stocks, futures, and real estate. Generally, 2% is seen as an important psychological threshold for the market. The accelerated rise in US bond yields may put pressure on risky assets and increase the volatility of global capital markets.

foreign exchange market: Higher US bond yields mean higher inflation expectations. When inflation rises too fast, the central bank's monetary policy will be tightened, thereby strengthening the US dollar. At the same time, rising US bond yields prompted capital flight from emerging markets, attracting capital flows from low interest rates and weak currencies to high-interest and strong currencies, which in turn led to an appreciation of the dollar. As far as the RMB exchange rate is concerned, China's treasury bond yield and US treasury bond yield remained large in the early period. After the US bond yield increases, the interest spread will decrease or even be inverted. This may reduce the amount of capital flowing into China's capital market, thus putting some pressure on the exchange rate.

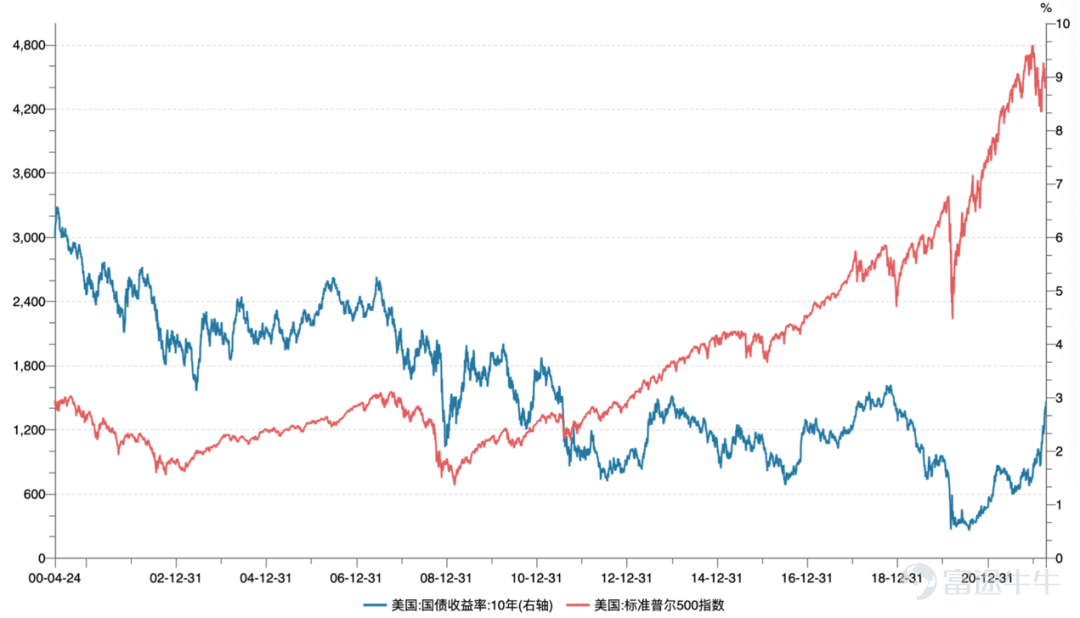

stock market: On the one hand, the trend rise in US bond yields is affected by higher inflation expectations. Higher inflation expectations also mean that monetary policy may be tightened, leading to market turbulence after revaluation; on the other hand, rising US bond yields mean an increase in the attractiveness of US bonds, which will also attract capital from the stock market to the bond market, leading to a decline in the stock market.Of course, the relationship between US debt and the stock market has historically been unstable (as shown below). It is driven by various factors, while the relationship between US debt and A-shares is more delicate and more affected by emotional panic.

Relationship chart between US Treasury yields and S&P 500 in the past 20 years

Asset pricing:Rising US bond yields are spreading in the economic market in the form of higher borrowing costs, such as increases in mortgages and car loans. At the same time, in the traditional sense, rising US bond yields will have a suppressing effect on the rise in gold prices, which under normal circumstances shows a negative correlation.

Some emerging market economies:The economic and financial situation in some emerging market economies is not optimistic in the first place. In particular, in low-income economies where the economy is sluggish, the debt is heavy, and the epidemic is difficult to control, the rapid rise in US bond yields has led to capital outflows, forcing emerging markets to suppress inflation and increase the attractiveness of capital through interest rate hikes, even though interest rate hikes at this time are inappropriate for the economy.

The impact on RMB assets is relatively manageable

Historically, the narrowing of the gap between China and the US has often been accompanied by the depreciation of the RMB, but it is not a key factor that dominates the RMB exchange rate. The renminbi has gradually shown the nature of a safe-haven currency in recent years, in stark contrast to other major emerging market currencies. The low volatility of the RMB itself, its low correlation with other assets, and its high yield make RMB assets the target of capital inflows under risk aversion. From a balance of payments perspective, at this point, current account and direct investment project surpluses are still large, domestic dollar liquidity is sufficient, and the scale of capital outflows is still manageable. As a result, the narrowing of the gap between China and the US may have limited impact on the RMB.

On the 21st, the President of the country delivered a keynote speech at the opening ceremony of the 2022 Annual Meeting of the Boao Forum for Asia, stating that “the fundamentals of China's strong economic resilience, sufficient potential, wide room for maneuver, and long-term improvement will not change, which will provide strong impetus for the steady recovery of the world economy and provide countries with broader market opportunities.”

Therefore, although the misalignment of monetary policies between China and the US will cause the gap between China and the US to gradually narrow, the dynamic outlook for China's economic growth is still very attractive to overseas capital.

【Risk Reminder]

The information in this material comes from public materials, and our company does not guarantee the accuracy and completeness of such information. Under no circumstances does the information or opinions expressed in this material constitute the actual investment results of our company, nor does it constitute any solicitation, invitation or any investment advice to investors. People reading this material should read the relevant sales documents in detail before making any investment decisions, fully understand the risks and relevant legal characteristics and consequences, and determine whether the investment fits their personal financial situation and investment goals based on personal circumstances, and whether they can withstand related risks, and seek appropriate professional opinions when necessary.

The copyright of this material belongs to Bosch Fund (International) Management Co., Ltd. No part of this material may be copied, copied or reproduced in any way, or distributed to any other person without written authorization.

The fund manager undertakes to manage and manage fund assets based on the principles of honest credit, diligence and responsibility, but does not guarantee that the fund will be profitable or profitable.The performance of other funds managed by the fund manager does not guarantee the performance expression of a certain fund. The fund's past performance and net value do not indicate future performance, and there is a risk of fluctuation in fund income.The fund manager reminds investors of the “buyer's own responsibility” principle of fund investment. After making an investment decision, the investor is responsible for investment risks caused by changes in the fund's operating conditions and net fund value.

Investors should purchase and redeem funds through the fund manager or other organization with fund sales qualifications. Fund documents and related announcements can be viewed on the fund manager's official website.

This material was issued by Bosch Fund (International) Limited and has not been reviewed by the Hong Kong Securities Regulatory Commission.

Investments are riskful, so please choose carefully.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

20

65