美聯儲鷹聲嘹亮,存在哪些風險和機會?

FOMC meeting minutes unexpectedly discussed balance sheet reduction, when will the turmoil in technology stocks end?

On January 5, 2022, the Federal Reserve released the supplementary minutes of the December FOMC meeting. Different from the statements in December, these meeting minutes caused a stir upon release, leading to a sharp decline in technology stocks. Even the stock prices of usually stable technology giants could not withstand the impact.$Microsoft (MSFT.US)$Google,$Tesla (TSLA.US)$、$NVIDIA (NVDA.US)$、$Amazon (AMZN.US)$As stock prices collectively weaken,$Alphabet-C (GOOG.US)$Stock prices have fallen below the 120-day moving average for the first time in over a year, causing a sense of anxiety in the entire market. Just what is happening? Following the December meeting, the Nasdaq surged directly, but yesterday's meeting minutes brought a chilling downward trend. After three weeks, what change has the Fed's attitude undergone? The analysis is as follows:

1. The meeting minutes extensively discussed the normalization of monetary policy. In addition to tapering and rate hikes, it is highly likely that balance sheet reduction may also accelerate, which exceeded the market's expectations.

Of particular note, participants expressed that the current economic outlook is much stronger compared to the last monetary normalization event (the balance sheet reduction that began in 2017), with higher inflation rates and a tighter labor market.

Currently, the Federal Reserve's balance sheet, whether in U.S. dollars or relative to nominal GDP, is much larger than at the end of 2014 when the third large-scale asset purchase plan concluded. Participants pointed out that the current weighted average maturity date of the Fed's holdings of Treasury securities is shorter than when the last normalization event began. Some delegations noted that, therefore, if the Committee follows its previous practices of gradually halting reinvestment of maturing Treasuries and principal payments on agency MBS, the pace of balance sheet reduction may be faster than the last time. However, some participants expressed concern about the vulnerability of the U.S. Treasury market and how this vulnerability could affect the appropriate pace of balance sheet normalization. Several attendees highlighted the potential benefits of a strategy framework for addressing this concern. Participants also believed that the Fed is better suited for normalization than in the past due to the ample reserve balance framework and the current interest rate control tools at the Fed's disposal, including interest on excess reserves and the overnight reverse repurchase agreement (ON RRP) mechanism, which are in place and functioning well. Some participants felt that significant balance sheet reduction during the normalization process may be appropriate, especially considering the abundant liquidity in the monetary markets and the higher usage rate of the ON RRP tool.

Participants discussed the appropriate conditions and timing for starting the balance sheet reduction relative to raising the federal funds rate from the ELB.In previous experiences, the balance sheet reduction began nearly two years after the policy rate (federal funds rate) started to rise, at which point the normalization of the federal funds rate was considered to be underway.。Almost all participants believed that it might be appropriate to begin deliberating on the balance sheet choice sometime after the first increase in the federal funds rate target range. However, participants determined that the appropriate timing for balance sheet deliberation might be closer to the rise in policy rates than the Committee's previous experience.They pointed out that the current situation includes a stronger economic outlook, higher inflation, and a larger balance sheet, which may require a faster pace for normalizing policy rates. They emphasized that the decision to start tapering would depend on the data.

Some participants commented that reducing policy accommodation by relying more on balance sheet reduction than raising policy rates could help limit any flattening of the yield curve during the policy normalization period. Some participants expressed concerns that a relatively flat yield curve could adversely affect the net interest margins of some financial intermediaries, which could increase financial stability risks. However, several other participants referenced staff analysis and past experiences, pointing out that many factors would influence long-term yields, making it difficult to determine how different policy combinations would affect the shape of the yield curve.

Many participants judged that the appropriate pace for balance sheet deliberation might be faster than in the previous normalization period. Many participants also believed that monthly caps on securities choices could help ensure that the pace of choices is measurable and predictable, especially given the relatively short weighted average maturity of the Fed's Treasury holdings.

Participants discussed factors to consider regarding the long-term scale of the balance sheet, consistent with effectively implementing monetary policy under an ample reserves regime. They noted that the current size of the balance sheet has expanded, and this size might be maintained for a period of time after the normalization of the balance sheet begins. Some participants highlighted that the level of reserves needed for effective monetary policy implementation is still uncertain, as banks' potential demand for reserves evolves over time. Given this uncertainty and the Committee's past experience, several participants expressed a preference for allowing a sizable buffer of reserves to support rate control. Participants indicated the need to carefully monitor developments in the money markets as reserve levels decline to provide information for the Committee's ultimate assessment of the appropriate long-term balance sheet level. Some participants believed that as the balance sheet approaches its long-term level, a strategic outcomes framework could help ensure rate control; some participants noted that the strategic outcomes framework could promote balance sheet choices rather than other scenarios. Some participants suggested that in the long run, establishing a strategic outcomes framework could reduce the demand for reserves, indicating that the long-term balance sheet could be smaller than in other scenarios.

Participants also discussed the composition of the Federal Reserve's asset holdings. Consistent with previous normalization principles, some participants indicated that in the long term, the Fed's asset holdings would mainly consist of U.S. Treasury bonds. In order to achieve this composition, some participants are inclined to reinvest the principal of MBS institutions relatively quickly into Treasury bonds, or to allow MBS institutions to run off their balance sheets faster than Treasury bonds.

2. The outlook for the economic situation is more optimistic. Controlling inflation is the Fed's current top priority, with a more resolute attitude than in December.

Reviewing the information obtained during the December 14-15 meeting indicates that after the slowdown in real GDP growth in the third quarter, there was a slight rebound in the fourth quarter. In October and November, the labor market conditions continued to improve, with significant increases in wage indicators so far this year. The consumer price inflation rate as of October (measured by the 12-month percentage change in the Personal Consumption Expenditures Price Index (PCE)) remains high. Nonfarm payroll employment steadily increased on average in October and November, but the average growth rate was lower than in recent quarters. The unemployment rate decreased from 4.8% in September to 4.2% in November; during this period, the unemployment rates for African Americans and Hispanic Americans also decreased significantly, but both rates are still well above the national average. Labor force participation rates and employment-population ratios increased in November. Based on measures of job openings and labor turnover, private sector job openings remain well above pre-pandemic levels. The four-week moving average of initial claims for regular state unemployment benefits decreased in early December, similar to pre-pandemic levels. Recently, estimates of weekly single-count payroll numbers for the private sector, using data provided by payroll processor ADP, indicate that private sector employment will further increase by early December. Over the 12 months ending in November, average hourly earnings increased by 4.8%, with wage increases in most industries being quite substantial.

In October and November, total nonfarm payroll employment steadily increased on average, but the average growth rate was lower than in recent quarters. The unemployment rate decreased from 4.8% in September to 4.2% in November; during this period, the unemployment rates for African Americans and Hispanic Americans also decreased significantly, but both rates are still well above the national average. Labor force participation rates and employment-population ratios increased in November. Based on measures of job openings and labor turnover, private sector job openings remain well above pre-pandemic levels. The four-week moving average of initial claims for regular state unemployment benefits decreased in early December, similar to pre-pandemic levels. Recently, estimates of weekly single-count payroll numbers for the private sector, using data provided by payroll processor ADP, indicate that private sector employment will further increase by early December. Over the 12 months ending in November, average hourly earnings increased by 4.8%, with wage increases in most industries being quite substantial.

Inflation data remains high, with various indicators suggesting increased inflationary pressures in recent months. As of October, the 12-month total inflation rate for PCE prices was 5.0%, while the core PCE price inflation rate (excluding changes in consumer energy prices and many food prices) was 4.1% during the same period.。The 12-month average reduction in PCE inflation rate constructed by the Federal Reserve Bank of Dallas was 2.6% in October, an increase of 0.6 percentage points from two months ago. In November, the 12-month change in the Consumer Price Index (CPI) was 6.8%, while the core CPI inflation rate for the same period was 4.9%. Based on survey-based medium- to long-term inflation expectations indicators — including the University of Michigan Consumer Survey, the New York Federal Reserve Bank Consumer Expectations Survey, and the Professional Forecasters Survey — have stabilized after rising over the past year.

Despite improvements in COVID-19 cases, the effects of previous fiscal stimulus measures have weakened, persistent supply bottlenecks, and recent consumer price increases, real PCE growth appears to have rebounded in the fourth quarter. Specifically, actual spending on retail goods steadily increased in October, while service spending strengthened. However, in November, the components of nominal retail sales data used to estimate PCE declined, possibly reflecting some holiday sales being brought forward to October.Auto sales volumes for October and November were below the average level of the third quarter, as extremely low dealer inventories continued to limit sales.。Housing demand remains strong, but there was relatively little overall change in housing sector activity indicators in October, including housing starts and sales.Shortages of building materials seem to be impeding the completion of construction, with limited land available for construction.

The upcoming data is consistent with the rebound in foreign economic growth this quarter, mainly due to the reopening of Asian economies after earlier lockdowns to curb the resurgence of COVID-19 cases. Strong growth in intra-Asia trade and solid readings from purchasing managers' indices also provide some early signs that production bottlenecks in the region are easing. In contrast, new public health restrictions introduced in Europe to address a new wave of COVID-19 infections seem to have dampened economic activity in some European economies. The recent discovery and rapid spread of the Omicron variant have prompted many foreign economies to impose new international travel restrictions. Foreign inflation continues to rise, primarily due to further increases in retail energy and food prices. Additionally, cost pressures from ongoing supply and transportation bottlenecks are reflected in the record high input and output price components of the purchasing managers' indices.

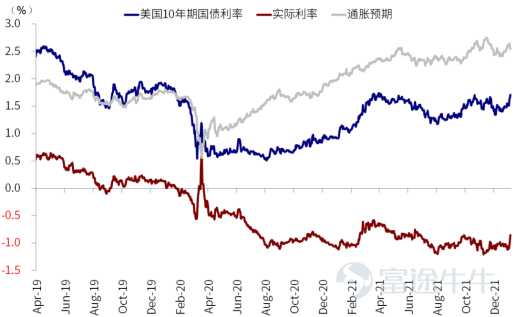

3. More hawkish remarks pushing real interest rates higher, growth stocks under collective pressure once again.

The Fed's hawkish stance led to a sharp rise in the yield of the U.S. ten-year Treasury bond to above 1.7%, as rising real interest rates put collective pressure on growth stocks, including Google last night.$Microsoft (MSFT.US)$、$NVIDIA (NVDA.US)$Even these YYDS are not immune. In the short term, rate hikes and balance sheet reductions are not the core of reversing the trend of technology giants, but the likely sharp valuation kill brought by short-term low sentiment. The market is very likely to fluctuate significantly in the near future, and after the rate hike is implemented, the core technology leader with stable and growing performance remains the best investment direction in the market.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (19)

to post a comment

40

104