百度Q2智能雲收入亮眼,你看好財報後走勢嗎?

Financial Report Review|Baidu's Q2 advertising business continues to pick up, AI cloud+intelligent driving continues to advance

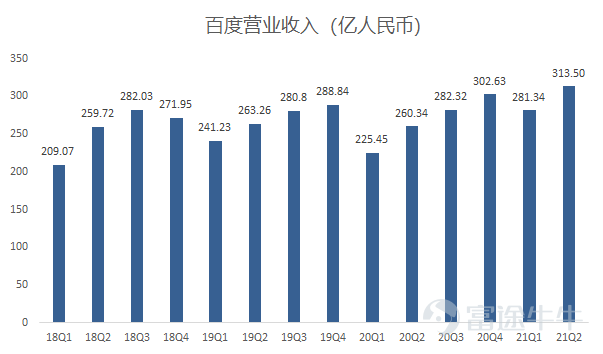

I. Financial performance:

1. Operating income:Baidu's core revenue (excluding iQiyi portion) was 31.35 billion yuan in Q2 2020, an increase of 27% over the previous year. iQiyi's partial revenue was 7.6 billion yuan, an increase of 3% over the previous year. The revenue growth of Baidu's core business this quarter was mainly driven by Baidu's smart cloud business development. This quarter's smart revenue reached 3.3 billion yuan, an increase of 71% over the previous year.

2、Ren Li:Baidu's net profit loss for Q2 2021 was 583 million yuan, compared to net profit of 3,579 billion yuan for the same period last year. The reason the net profit turned into a loss was that its long-term investment “Kuaishou Technology” stock price was drastically adjusted, causing long-term investments to lose 3.1 billion yuan at fair value.

3. Operating profit:Baidu's core operating profit was 4.6 billion yuan, and the core operating profit margin reached 19%.The adjusted EBITDA was $7.3 billion. Baidu Core's adjusted EBITDA is $8 billion, and Baidu Core's adjusted EBITDA margin is 33%.

4. Financial Guidelines:suppositionBaidu's core revenue increased 9% year over year~20%. Baidu's revenue is expected to be between RMB 30.6 billion (US$4.7 billion) and RMB 33.5 billion (US$5.2 billion), an increase of 8% to 19% over the previous year.

II. Online marketing business: Q2 marketing business recovered, Q3 uncertain

1. Operating data:Baidu's MAU reached 580 million people in June, of which the proportion of daily logged-in users reached 77%.Considering that currently search content in closed-loop ecosystems such as WeChat, ByteDance, and Weibo has not been fully opened, Baidu still has certain limitations in terms of search resources.

In addition, Baidu's previously active content platforms such as live streaming, short videos, and Q&A are also facing fierce competition, so the Baidu app and overall user base are growing slowly. No detailed data was disclosed in this financial report on live broadcasts, short videos, etc. that previously established a content ecosystem.

2. Performance and outlook:Baidu's core online marketing revenue in Q2 was 19 billion yuan, an increase of 18% over the previous year. Mainly in Q2, China's epidemic was controlled and online advertising gradually recovered.However, in Q3, Baidu's online marketing business may face a lot of pressure. First, the epidemic was repeated in some regions, and industries such as offline consumption, transportation and travel were clearly impacted, which is likely to affect Q3 related industries; secondly, stricter regulations in the Q3 online education sector directly led to a decrease in online advertising related to online education. The various problems experienced by the online marketing business in Q3 are also reflected in the expected growth rate of Q3's core revenue (9% to 20%)

3. AI Cloud and Autonomous Driving: Intelligent Cloud Continues to Maintain High Growth Rate, and Intelligent Driving Continues to Promote Commercialization

The AI cloud is Baidu's new growth engine at present, and it is also the most mature business of Baidu's AI strategy.Baidu has been investing in AI technology on a large scale for many years. Currently, the most mature commercial promotion is the AI cloud, which provides AI capabilities to customer services through cloud computing capabilities.

1. Operation and performance:The revenue of the smart cloud business this quarter was 3.3 billion yuan, up 71% year on year, and maintained a high year-on-year growth rate for many consecutive quarters. According to the Q2 conference call, Baidu's new customer retention rate has performed well. New customers and new projects account for a relatively high proportion, and it will further expand into different industries in the future. However, objectively speaking, the domestic giant Alibaba Cloud is also currently in the stage of rapidly expanding new industries, and whether it can maintain a growth rate of 70% or more in the future may face a lot of uncertainty.

In terms of AI technology:Looking at the product structure, the difference between Baidu Smart Cloud and other cloud computing service providers is that Baidu's positioning focuses more on AI capabilities. In other words, the cloud computing business is not only a separate part of Baidu's business, but also a channel for selling Baidu's AI capabilities to customers.

According to the IDC report of June 2021, Baidu's deep learning platform became the most widely used platform in China. The cumulative number of developers of its open AI platform PaddlePaddle increased to 3.6 million, an increase of 62% over the previous year, serving 130,000 enterprises. Simply put, Baidu not only wants to be an AI developer's own ecosystem, but also wants to be an AI developer ecosystem. Currently, more and more players and customers are joining the ecosystem. This is probably one of the highlights of Baidu Cloud's differentiated competition in the future.

2. Intelligent driving:Baidu's intelligent driving is divided into: ① Apollo autonomous driving, where the main customer is to provide autonomous driving solutions to automakers; ② Baidu ended up building a car: Baidu and Geely set up a joint warehouse to build their own cars; ③ Apollo Robotaxi: also an autonomous public transportation business. The Apollo L4 test run reached 7.5 million miles this quarter, and in June, Great Wall Motor announced that its flagship model would be equipped with Apollo automatic parking in the new 2021 version. In the long run, Baidu has invested heavily in intelligent driving, and it is also a point where the capital market focuses on Baidu's potential, but judging from the latest financial information, the intelligent driving business has not yet entered the point of large-scale monetization

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

10

22