【聚焦】政治局會議召開,釋放了哪些重磅信號?

The long-lasting pain inflicted by Ning has finally come to an end, with a major counterattack from the likes of Moutai.

The weather in summer is unpredictable and erratic—sometimes thunder roars and torrential rain pours down, while at other times the sun shines brightly in a clear blue sky.

The same was true for the A-share market, which saw extreme pessimism and heavy selling in the morning session, only to shift to extreme optimism half an hour later like Sun Wukong’s ever-changing face. This encapsulated last week's market movements in a single day.

Kweichow Maotai once plummeted by 3.4%, with its share price nearing 1,600 yuan, but eventually surged 4.5%, breaking through the 1,750-yuan mark, resulting in a staggering market cap fluctuation of 170 billion yuan. Looking at Tongce Medical, it almost hit the lower limit during trading, yet closed with a rise of over 3%, marking a 13% fluctuation. Other big names like舍得 (Shede), Jiugui Liquor, and Huaxi Biotech also staged significant rebounds. However, CATL surged 4% in the morning session but plunged to -3% in the afternoon, eventually closing with a modest gain of 0.29%. Of course, there were many smaller stocks that followed the downturn.

One retail investor raised a soul-searching question:Why does the A-share market experience such wild surges and plunges?

1

Why the sharp ups and downs?

China's institutional investors dominate market discourse, but their investment mechanisms and philosophies have notable issues (for example, focusing solely on short-term rankings), chasing short-term price differences rather than long-term stable returns.

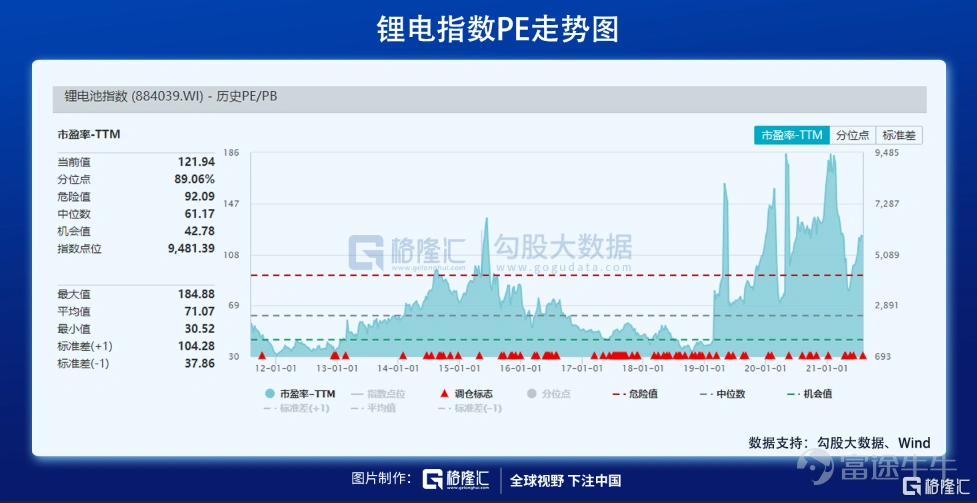

Currently, institutions have evolved into trend-following herds, such as the pre-Chinese New Year craze for baijiu and leading companies in various sectors, rapidly pushing stock prices sky-high within a very short period of time, only to result in a disastrous aftermath post-festival. This year, institutions aggressively targeted electric vehicles, photovoltaics, and semiconductors, creating a strong money-making effect and forming a positive feedback loop, with stock prices doubling or even increasing tenfold within just a few months.

In the past, institutions looked at P/E ratios and fundamentals; later, they focused on PEG ratios and valuation adjustments. But now, they only look at trends, while the concept of value investing has long been cast aside, becoming a slogan used to justify rampant speculation.Under this atmosphere, institutions trample real value investing underfoot, concentrating firepower on making quick profits. How about jumping into lithium batteries or photovoltaics? In just over a year, isn't a fivefold or tenfold return enticing enough?

Last year, baijiu was extremely popular, whether it was Moutai, Wuliangye Yibin, Luzhou Laojiao, or smaller distilleries, all seeing their stocks double or even triple, with the slogan 'YYDS' (forever a god) still ringing in our ears. At the peak of this frenzy—on December 23 last year—a widely spread article titled 'A Letter of Persuasion to Those Shorting Baijiu' took the internet by storm.The most tear-jerking statement: The trend of the baijiu industry is unstoppable, those who go with it will prosper, and those who go against it will fail!

Zhang Kun was also deified due to the extreme surge in baijiu stocks, but what about now? Has the fundamental situation changed for Moutai, which went from 2,600 to 1,700 in just half a year? No, the only thing that has changed is the thrill of making quick money, and wealth has undergone a massive shift. Last year’s investors cashed in on Moutai's potential gains of 2-3 years within just a few months, while those who entered this year are facing significant losses—not just their principal.

Last weekend, 'A Letter of Advice to Consumption and Healthcare Fund Managers' went viral across the web—let’s pivot to lithium! The trend of lithium batteries is overwhelming, those who follow it will thrive, and those who oppose it will perish! What a familiar tune!But I know that trees don’t grow to the sky, and you have to eat your meals one bite at a time.

Those who bought into premium baijiu names like Moutai, Wuliangye, and Luzhou Laojiao earlier this year probably thought that even if the broader baijiu sector collapsed, the strongest blue-chip leaders wouldn't falter because their solid performance would eventually justify their valuations. But things didn’t go as planned, as the three were slashed by 32%, 31%, and 42% respectively over six months. Now, those trading lithium, chips, and EVs likely share similar thoughts. In my view, speculation is fine, but don’t mistake it for value investing—don’t get too carried away and remember to exit in time.

Trend speculation, focusing firepower to make quick profits, has become one of the biggest sources of market instability among institutional players.That wave around Chinese New Year was the same, and so was last week’s doomsday-like plunge over the first three days.

2

How to view 730

After discussing the market trends, let’s move on to last Friday’s Politburo meeting—it was quite important.

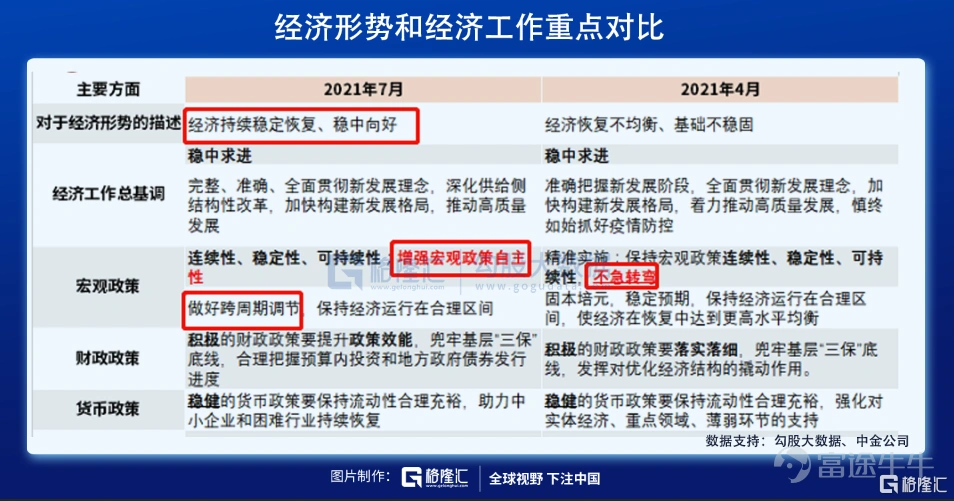

The description for July differs from April in three key aspects, which need to be interpreted carefully.

First,The description of the economic situation has changed from 'uneven economic recovery and an unstable foundation' in April to 'continued stable recovery with a steady upward trend'.This indicates that the authorities believe the economic situation has improved compared to April.

However, in reality, the economy has shown a noticeable downward trend in recent months, with an even more 'unstable foundation.' When the reserve requirement ratio (RRR) cut was announced in July, both mainstream expectations and expert interpretations generally believed that the future economic outlook was not optimistic and that stimulus measures would be needed to counteract the downturn.

On July 31, the National Bureau of Statistics disclosed that the manufacturing Purchasing Managers' Index (PMI) was 50.4%, a significant drop of 0.5 percentage points from the previous month. Among this, the PMI for small enterprises was only 47.8%, declining by 1.3 percentage points from the previous month. This demonstrates the current state of the economy, especially the difficulties faced by small enterprises. The primary logic behind the previous targeted RRR cut was also to provide 'lifeline funds' to small and medium-sized enterprises.

The official assessment of the economic situation has greatly exceeded mainstream expectations—why is this the case?

It's important to recognize that this stance will determine the direction and intensity of upcoming monetary policies, fiscal measures, and economic adjustments. Let’s set that aside for now and continue examining further details.

Second, there was an unusually explicit mention of 'cross-cycle adjustment.'What we usually hear and see is 'counter-cyclical adjustment,' which means stimulating the economy with measures like injecting liquidity when it is slowing down, and tightening liquidity or raising interest rates when the economy overheats.

The meeting's mention of 'cross-cycle' instead of 'counter-cyclical' suggests that the policy is more focused on changes occurring in the larger cycles and environment above the traditional economic cycle, as well as how the policy framework should address these medium- and long-term issues.

In simple terms, although the current economic slowdown is evident, there is no urgent need for counter-cyclical adjustments or injecting liquidity to boost economic growth.It's about reserving more ammunition for when it's more needed, such as next year when the economy may be even tougher.Because we are not only focused on the present or the second half of the year; our perspective has extended to a longer time frame. With this understanding, one should be able to grasp why the conference’s statement on the economic situation went far beyond both reality and expectations.

Third, the macro policy deleted 'not making a sharp turn' and added 'enhancing the autonomy of macro policy.'In the past, the interpretation of 'not making a sharp turn' usually meant not tightening the funding side significantly, i.e., no interest rate hikes. Removing it, does this imply that the possibility of an abrupt shift in monetary policy (raising interest rates) is being considered? In my view, deleting the commitment to 'no sharp turn' probably means that the current monetary policy, after a year of adjustment, has returned to its pre-pandemic normalization and there is no basis for a sharp turn.

Currently, US inflation continues to rise, and the probability of being forced into a sharp monetary turn is increasing day by day, with a high likelihood of interest rate hikes in 2022. Based on past behavior, once the US enters an interest rate hike cycle, major economies around the world tend to follow, including China which has done so for many years. However, the ebb and flow of US interest rate hikes and cuts largely represent the use of dollar hegemony to harvest global wealth.

This time, top leadership clearly proposed 'autonomy of macro policy,' meaning that China will not follow the US dollar. Autonomy implies roughly two scenarios: one is raising interest rates before the US does, and the other is that after the US raises interest rates, China instead lowers them. In the first scenario, given the current economic downturn and high debt levels, the probability of raising interest rates ahead of the US would be relatively low.

What about the second scenario? Historically, from 2003 to 2006, the US embarked on a three-year interest rate hike spree, but due to China’s significant economic growth potential, foreign capital did not flow back to the US as much as the Fed expected (the rebound of the US Dollar Index was very weak). After failing to 'harvest' China, this indirectly led to the outbreak of the subprime mortgage crisis. It should be noted that in previous interest rate hike cycles, the US successfully harvested wealth from Latin America, Japan, and the Asian Tigers.

Thus, after this upcoming (forced) US interest rate hike, there is a considerable probability that China might lower interest rates to stabilize the economy, which could instead make China a safe haven for foreign capital. This aligns with the second point discussed earlier, offering a clearer perspective on the situation.

Through the Politburo meeting, we can roughly judge that the pressure on economic growth in the coming period will be significant, and we shouldn’t expect excessive liquidity injections to offset this, because we need to save our resources for even tougher times.Therefore, this will suppress the overall capital market, and this macroeconomic backdrop remains quite clear.

3

Epilogue

This year, the stability of the A-share market has been very poor, with roller-coaster movements occurring multiple times already. It has become difficult to profit from the market. Healthcare stocks, led by Tongce Medical, have performed relatively well despite several ups and downs, with a small overall gain for the year.

However, blue-chip stocks that were aggressively pushed up last year haven’t been as lucky, such as Moutai, Wuliangye Yibin, Luzhou Laojiao, Vanke, Conch Cement, Sany Heavy Industry, Ping An, Yili, Midea, Gree, Shuanghui, Zhongju Hi-Tech, Muyuan Foods, New Hope, Yonghui Superstores, and Shanghai Machine Tool.A large number of investors are stuck holding these shares, and it may take a long time before they recover their losses; of course, some may never break even.

The old speculative strategies focused on small-cap stocks, and the current value investing approach, both face the risk of collapse, increasingly evolving into trend speculation. This makes it harder for more investors to navigate the market, and losing money becomes much easier.Currently, managing one’s position is extremely important, and keeping some cash reserves is also a prudent move.

Last year, liquor stocks were considered 'eternal gods' (YYDS), this year it's lithium battery stocks. So who will be the next big thing?

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1