Domestic alternatives to IGBTs and technology trends

Article transferred from Yushi Capital and Semiconductor Watch, “Crown Pearl: IGBT is a typical application for next-generation power semiconductors”

The overall growth of the power semiconductor industry is steady, and the periodicity is relatively small

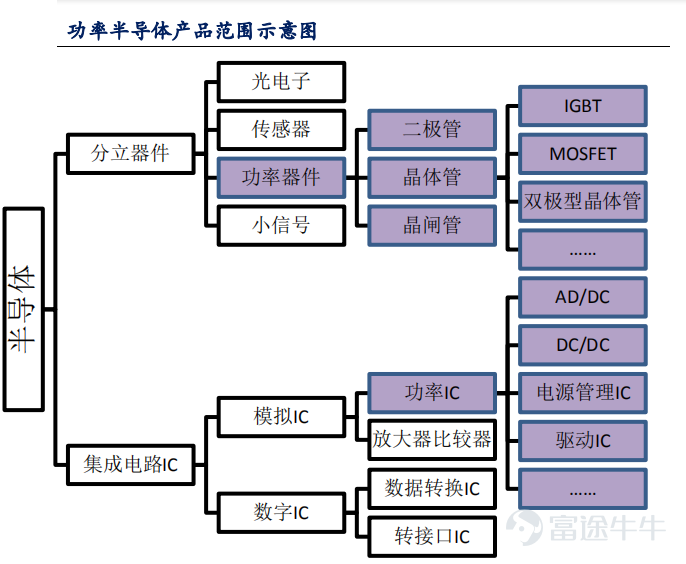

Power semiconductors are the core of electric energy conversion and circuit control in electronic devices. They are mainly used to change the voltage and frequency, DC to AC conversion, etc. in electronic devices. Power semiconductors are subdivided into power devices (a discrete device) and power ICs (an integrated circuit). Ideally, a perfect converter has no voltage loss when turned on, and no power loss when switching on and off. Therefore, the goal of product and technological innovation in the field of power semiconductors is to improve energy conversion efficiency.

The shaded parts in the image below are all power semiconductors:

According to IHS statistics, the global power semiconductor market was about 40 billion US dollars in 2019, and the global power semiconductor CAGR is expected to be 4.5% in 2019-2025. According to China Resources Micro's prospectus, China is the world's largest consumer of power semiconductors. In 2018, the market demand reached 13.8 billion US dollars, a growth rate of 9.5%, accounting for 35.3% of global demand.

There are many levels of power semiconductor products, and IGBTs are typical products in the new generation

The evolution path of power discrete devices is basically diodes → thyristors → MOSFETs → IGBTs. Among them, IGBTs are typical products in the new generation of power semiconductors. IGBT (Insulated Gate Bipolar Transistor), an insulated gate bipolar transistor, is a fully control-voltage-driven power semiconductor composed of BJT (bipolar triode) and MOSFET (insulated gate field effect transistor). IGBT not only has the advantages of fast MOSFET switching speed, high input impedance, low control power, simple driving circuit, and low switching loss, but also has the advantages of low BJT conduction voltage, high on-state current, and low loss. Comparatively, it is an ideal switching device in the field of power electronics, and is also known as the “CPU in power electronics devices.”

According to statistics related to Yole and others, currently about 50% of the world's power semiconductors are power ICs, and the remaining half are power discrete devices; MOSFETs accounted for the highest share of power discrete device sales in 2017, followed by diodes/rectifier bridges accounting for about 29%, thyristors and BJTs accounting for about 21% of discrete devices, and IGBTs accounting for 19%, but the compound growth rate is the fastest among all products.

IGBT industry chain and three business models

IGBT's industrial chain includes upstream IC design, midstream manufacturing and packaging, and downstream includes fields such as industrial control, new energy, home appliances, and electric high-speed rail;

IGBT companies have three business models:

IDM:The IDM model is a vertically integrated manufacturer. It refers to an enterprise model that includes all aspects of circuit design, wafer manufacturing, package testing, and investment in the consumer market. IGBT chips and fast recovery diode chip design are only one of these divisions, and the company has its own fab, packaging plant, and test plant. This model is extremely demanding on corporate technology, capital and market share. Currently, only a few international giants such as Infineon and Mitsubishi have adopted this model;

Mods:Such as Danfoss, SEMIKRON, etc.;

Fabless mode:Fabless is a combination of Fabrication (manufacturing) and less (nothing). The Fabless model is a business model in the integrated circuit industry. That is, the company itself focuses on chip design and outsources chip manufacturing to the founders, and the chip founders are responsible for purchasing silicon wafers and processing and production. Fabless companies do not need to invest in establishing wafer manufacturing production lines, reducing investment risks, and being able to quickly develop the chips needed for terminals.

Most foreign giants use the IDM model, and the Fabless+ module model used by typical domestic companies such as Star Semiconductor: The main reason why the Fabless model is popular in China is that power semiconductors do not require particularly sophisticated foundry foundry, and the capital recovery period for separate production lines is very long. In addition, there are many mature process foundries in mainland China that have sufficient control over production capacity, so for most domestic manufacturers, Fabless is a good model during the rapid catch-up period.

IGBT product updates are slow and prices are stable

Since the 1980s, IGBT chips have gone through 6 generations of upgrades. From planar penetration type (PT) to groove type electric field-cutoff type (FS-trench), various indicators such as chip area, process line width, on-state saturation voltage drop, shutdown time, and power loss have been continuously optimized, and the off-state voltage has also increased from 600V to over 6,500V.

Base station RF PA faces new challenges in 5G

IGBT product updates are slow: Currently, the IGBT4 generation defined by Infineon is the mainstream of the market and has been used for more than ten years. Infineon launched IGBT7 at the end of '18, reducing the area by 25% compared to the 4th generation, reducing costs and reducing power consumption. It is expected that large-scale promotion will still take 2-3 years. IGBT updates are relatively slow. The chip plays a decisive role in product performance, and the module can only guarantee the performance of the chip. The new generation of IGBT chips and the old generation each have advantages. The older generation's indicators such as loss and area are not necessarily good, but stability has been verified over a long period of time, and quite a few customers still choose to use the old generation chips when the new generation comes out. Other domestic and international companies have deployed IGBT7 generation technology, but the product verification cycle is long. Generally, customers need 5 to 10 years to verify reliability and application-side issues, so the iteration speed is slow. Currently, the latest generation IGBT Star is being jointly developed with Huahong, and trial production is expected by the end of the year.

The price of IGBT is relatively stable: even when the industry declined in 2019, the factory prices of major manufacturers did not drop, showing a very healthy price fluctuation. In summary, the IGBT chip update is relatively slow, and it is a gradual innovation, and continuous optimization and upgrading. Specifically, certain IGBT products can be used for 10 years; at the same time, the IGBT industry giants are mainly German and Japanese manufacturers. The style is relatively conservative, and they will not aggressively expand production capacity or fight price wars. Demand is stable and prices fluctuate relatively little, even when overall demand for semiconductors was poor in 2019.

The core of circuit design is logic design, which can be used through software such as EDA, and power semiconductors are similar to analog ICs, and require continuous adjustment and compromise according to actual product parameters. Therefore, the experience requirements for engineers are also higher, and excellent designers need 10 years or more of experience. Some textbooks on power semiconductors and analog ICs in universities are also basically equivalent to “experience notes” from practitioners over the past few decades. There is no relatively “standard paradigm” like digital integrated circuits, and R&D is also a process of continuously modifying parameters to balance performance and cost through a team of R&D engineers.

Specifically, IGBT technology and barriers are extremely high, mainly reflected in the following aspects:

1) IGBT chip design

The IGBT chip is the core of the IGBT module: its design process is extremely complex. It is necessary not only to keep the module working stably in a high current, high voltage, and high frequency environment, but also to maintain a balance between opening, closing and loss, short circuit resistance, and conduction voltage drop. Fast recovery diode chips are used in conjunction with IGBT chips in IGBT modules. While they need to withstand high voltage and high current, they also require extremely short reverse recovery time and reverse recovery loss. An enterprise can only gain a foothold in the industry if it has a deep technical heritage and strong innovation ability, and has accumulated rich experience and knowledge reserves. Therefore, latecomers in the industry often need to go through a long period of technical exploration and accumulation to compete with companies that already have a technological advantage in the industry.

2). Module design and manufacturing process

IGBT modules require high product reliability and quality stability, and the production process is complicated. A seemingly simple process in production often requires a long time of exploration to master, such as aluminum wire bonding. On the surface, the circuit only needs to be connected with aluminum wire, but the selection of bonding points, the strength, time, parameter settings of the bonding machine, fixture design applied during the bonding process, and employee operation methods will all affect the quality and yield of the product. As the core component of industrial products, IGBT modules need to adapt to various harsh working environments in different application fields, so the requirements for product quality are high. For example, in the electric welding machine industry, consider inverter electric welders.

The working environment is harsh and the usage load is heavy. When purchasing IGBT modules, priority is given to the durability of the module. Therefore, the reliability of chip parameters and module manufacturing process is the core of producing IGBT modules. Furthermore, IGBT is closely integrated with downstream applications, and often requires R&D personnel to have a good understanding of the downstream application industry to produce products that meet customer requirements. Currently, there is still a shortage of R&D technical personnel with relevant practices and experience in China. If newly entered enterprises want to master the design and manufacturing process of IGBT chips or modules and achieve large-scale production, it will take a long time to train talents, learn, explore, and accumulate technology.

IGBT manufacturers' product stability needs to be verified over a long period of time, and the construction of brand effects and reputation needs to be accumulated:

IGBT modules are key components in downstream products. Their performance, stability and reliability are critical to downstream customers, so the certification cycle is long and replacement costs are high. When it comes to new IGBT suppliers, customers often maintain a cautious attitude. Not only do they comprehensively evaluate the strength of suppliers, but they also usually have to go through multiple steps such as individual product testing, machine testing, and multiple small-batch trials before making large-scale procurement decisions, and the procurement decision cycle is long. Therefore, even if new entrants to the industry develop and produce IGBT products, it will take a long time to win customer recognition.

The driving factors of the IGBT industry are clear, and the driving force of moving the ceiling upward is strong

IGBT is widely used in many fields such as industrial control and automation, new energy vehicles, motor energy saving, solar power generation, wind power generation, etc.; it is used to improve the efficiency of power conversion, transmission and control in various circuits. Among them, drive systems in new energy vehicles are the most typical application.

In terms of global IGBT applications, industrial control accounts for 37%, the largest application area, electric vehicles: 28%, new energy power generation 9%, and consumer sector 8%; domestically, due to the development of high-speed rail in China, industrial control in downstream applications is 29%, rail transit is 28%, new energy vehicles 12%, and new energy generation 8%. However, with the continuous development of China's new energy sector, the share of demand for new energy vehicles, photovoltaics, and wind power will continue to rise in the future.

In 2017, the global IGBT market was US$5.255 billion, up 16.5% from 2016. In 2018, the global IGBT market was around US$5.836 billion, up 11% year on year, making it the most prosperous among all segments of power semiconductors.

Since the development of China's IGBT industry, great progress has been made. Although large imports are still needed, some enterprises already have large-scale production capacity. China's IGBT power module production was 1.9 million in 2010, and increased to 11.15 million in 2018.

Domestic IGBT demand growth far exceeds global growth: According to data from Intelligent Research Consulting, China's IGBT market size in 2018 was 16.19 billion yuan, up 22.19% year on year, and the growth rate is significantly higher than the global average; benefiting from the continuous development of China's strong fields such as new energy vehicles, wind power, and photovoltaics, it is expected that the compound growth rate of domestic IGBT will continue to be above 20% in the future.

IGBT competition pattern: Europe, America, and Japan basically have a monopoly, and the share of domestic production is extremely low

The IGBT market competition pattern is concentrated. The main competitors include Infineon, Mitsubishi, Fuji Electric, Ansemi, Swiss ABB, etc. In 2017, the share of the top five global IGBT manufacturers exceeded 70%, and the current market share of domestic companies is generally small.

IGBTs mostly appear in the form of IGBT modules. Domestic IGBT leader Star Semiconductor had a market share of 2.2% in the module field in 2018. According to Star Semiconductor's 2018 revenue of 675 million yuan, the market space for IGBT modules launched in 2018 was close to 30 billion yuan (of which the overall IGBT market space in 2018 was 5.836 billion US dollars)

There is plenty of room for domestic alternatives. Currently, only Star Semiconductor has entered the top 10 domestic IGBT modules in the world, but it only accounts for 2.2% of the global IGBT module market share. Since the downstream application of IGBT in new fields such as new energy vehicles, photovoltaics, wind power, etc., China's voice in the world is higher than in the traditional fuel vehicle field and industrial control field in the past, so more than half of the demand in the IGBT incremental space is in China. In the next few years, China's IGBT market demand share will increase from no 35% in 2019 to 50% or more in 2025, increasing the share of IGBT manufacturers in China and Competitiveness has created favorable conditions, and domestic IGBT manufacturers have great potential to increase their market share and business volume.

Determining High Growth: Drivers of IGBT's High Prosperity Over the Next Five Years

IGBTs account for nearly 8% of NEV costs and are pure incremental products

The main applications of IGBT in the field of electric vehicles are divided into three categories:

1) Electronic control system: The IGBT module drives the automobile motor (electronic control module) after converting DC to AC;

2) Vehicle air conditioning control system: low power DC/AC inverter. The working voltage of this module is not high, and the unit price is relatively low;

3) The IGBT module in the charging pile is used as a switch: the IGBT module in the charging pile accounts for nearly 20% of the cost;

According to Digitimes Research data, in the current cost structure of new energy vehicles:

1) Batteries account for the largest share of costs. Generally speaking, they can account for more than 40% of the total cost of electric vehicles;

2) Motor drive systems account for the second largest cost, which can reach 15% to 20% of the total cost of electric vehicles, while IGBT accounts for 40%-50% of the total cost of electric vehicles. In other words, IGBT accounts for nearly 8% of the total cost of new energy vehicles.

Also, for IGBTs, the demand for IGBTs for new energy vehicles is a pure incremental increase, because traditional fuel vehicle power semiconductor devices require only Si-based MOSFETs, and MOSFETs for NEVs above 600V cannot meet the requirements and must be replaced with IGBTs; therefore, IGBTs are the second most beneficial component after batteries.

Each NEV is expected to cost an IGBT of 450 US dollars: According to Yole Development's estimates, the average IGBT consumption per vehicle in 2016 is about 450 US dollars. Of these, ordinary hybrid and plug-in hybrid vehicles require about 300 US dollars of IGBT per vehicle, and pure electric vehicles use an average of 540 US dollars of IGBT per vehicle.

According to the average IGBT usage of bicycles in 2019, which is 460 US dollars, benefiting from the continued increase in the share of BEVs, the average bicycle usage is expected to increase year by year to 490 US dollars/car in 2022. Starting in 2023, after the maturity of SIC-MOS, the average IGBT usage of bicycles will gradually decline to 430 US dollars/vehicle in 2025, and the estimated sales volume of new energy vehicles will be 5.04 million units in 2025 (estimated according to the national NEV industry development plan - the penetration rate of electric passenger vehicles in 2025 is about 25%).

According to the above hypothesis, it is simply estimated that China's automotive IGBT market will reach 2.2 billion US dollars in 2025. At that time, the number of new energy vehicles in the world is expected to be 3 times that of the domestic market (that is, overseas sales are 2 times that of domestic), and the global automotive IGBT market will reach 6.6 billion US dollars, which is equivalent to reinventing the IGBT market (the total global IGBT in 2019 was in the 6 billion US dollar range).

IGBT continues to benefit from the increase in the share of photovoltaics and wind power in the energy mix

Rectifiers and inverters in wind power and photovoltaics require IGBT modules. According to Energy Administration data, in 2019, domestic PV installations were 30.11GW, and global PV installations were 115GW.

Domestic photovoltaic power generation accounted for 3% of the total power generation in 2019, and there is great potential for continued growth in the future. According to the “China Photovoltaic Development Outlook 2050” of the United Nations Climate Change Conference in Madrid, China's photovoltaics will begin accelerated deployment from 2020 to 2025; from 2025 to 2035, China's photovoltaics will enter a period of accelerated large-scale deployment. By 2050, photovoltaics will become the largest power source in China, accounting for about 40% of the country's electricity consumption in that year, and there is still plenty of room and potential for future photovoltaic development.

The global demand level for IGBTs corresponding to wind power and photovoltaics in 2025 is 1.5 billion US dollars: the total IGBT space and share of new energy power generation estimated by the aforementioned intelligent research consulting and Infineon can be estimated (IGBT's 2018 global market space was 5.8 billion US dollars, of which IGBT applications such as photovoltaics and wind power accounted for 9%). In 2018, the PV wind power IGBT market space was about 522 million US dollars. In the current energy structure, solar and wind energy together account for less than 10%. In the context of global energy saving and emission reduction, it has become the consensus of countries around the world to reduce dependence on fossil energy and increase the use of solar and wind energy. According to BloombergNEF's forecast, it is estimated that the world will add close to 300 GW of new PV installations in 2025, and wind power will also grow about 2.5 times compared to PV in 5 years, so it is estimated that the global demand for IGBT corresponding to wind power and photovoltaics in 2025 will be 1.2 to 1.5 billion US dollars.

Variable frequency driving IGBTs for white goods continue to grow

IGBT is one of the core components of “inverters”, and the promotion of inverter white goods can bring a stable market to IGBT's IPM. Currently, there is room for improvement in the frequency conversion penetration rate of white goods appliances: according to the industry online network, the domestic white power inverter penetration rate has continued to increase in recent years: 1) Air conditioners: from 2012 to 2018, domestic inverter air conditioner sales increased from 30.16 million units to 64.34 million units, and the penetration rate increased from 28.94% to 42.70%; 2) Refrigerators: From 2012 to 2018, domestic inverter refrigerator sales increased from 3.63 million units to 16.65 million units; 3): From 2012 to 2018, domestic inverter washing machines increased Washing machine sales increased from 5.77 million units to 21.63 million units, and the penetration rate increased from 10.36% to 32.97%. Yole expects the market size of variable frequency drive IGBT for white goods to reach 990 million US dollars in 2022, an increase of 22% over 2017.

The localization of IGBTs with variable frequency white electricity is low: only Silanwei and HuaWei Electronics are shipping some white power IPM modules in China. Although the unit price of IPM modules for home appliances is low, the power to replace suppliers is not strong, and downstream is concentrated. Currently, the leading suppliers are all Japanese and American companies, such as the US, mainly Sanyo and Fairchild; Glee/Haier is mainly Mitsubishi, and some IR and LS are being supplied. When supply chain security is threatened by the external environment, domestic IGBT manufacturers will still have a niche market in the future Relatively large replacement potential.

The field of industrial control is the basic platform for IGBT applications

IGBT modules are core components in traditional industrial control and power supply industries such as inverters and inverter welders, and have been widely used in this field.

1) Inverter industry

The overall market size of China's inverter industry is on the rise. The IGBT module not only plays the role of a traditional transistor in a frequency converter, but also includes the role of a rectifier. According to the Forward-looking Industry Research Institute, the market size of China's inverter industry in 2016 was 41,677 billion yuan, with an average 4-year compound growth rate of 8.74%. In 2017, China's inverter market size was about 45.32 billion yuan. In the next few years, the high-voltage inverter market with high-efficiency and energy-saving functions will continue to grow, driven by policies. By 2023, the high-voltage inverter market will reach about 17.5 billion yuan.

2) Inverter welding machine industry

An inverter arc welding power supply, also known as an arc welding inverter, is a new type of welding power supply. This type of power supply generally converts a three-phase power frequency (50 Hz) AC network voltage first rectified and filtered by an input rectifier, then converted to DC through the alternating switching effects of high-power switching electronic components (IGBTs), and inversely converted into medium frequency AC voltages of several thousand Hz to tens of thousands of hertz. According to data from the National Bureau of Statistics, in 2018, China's electric welding machine output was 8.533 million units, an increase of 584,600 units over 2017. Continued heating of the electric welding machine market will also ensure a gradual increase in demand for IGBTs.

The global industrial control IGBT downstream market is scattered: According to Jibang Consulting data, the IGBT market size of the global industrial control market in 2019 was about 14 billion yuan, and the IGBT market size of the Chinese industrial control market was about 3 billion yuan. Due to the fragmentation of downstream demand in the industrial control market, the increase in downstream demand alone is difficult to drive up overall industry demand. Therefore, demand in the industrial control IGBT market is relatively stable. Assuming a 3% annual growth rate in the future, the global industrial control IGBT market is expected to reach 17 billion yuan by 2025. This is the basic market for the IGBT industry. Demand is stable and fluctuations are relatively small.

High market attention: how to view the challenges of third-generation semiconductor materials to IGBT

leniencyIntroduction to semiconductors

Many of the world's power semiconductor giants are laying out the next generation of power semiconductors based on gallium nitride (GaN) and silicon carbide (SiC), laying the foundation for competing with traditional silicon-based power semiconductors in the market.

SiC and GaN are third-generation semiconductor materials. Compared with first-generation second-generation semiconductor materials, third-generation semiconductor materials have a wider bandgap width, higher breakdown electric field, higher thermal conductivity, higher electron saturation rate, and higher radiation resistance. They are more suitable for making high-temperature, high-frequency, radiation-resistant and high-power devices, and are also commonly known as wide bandgap semiconductor materials.

Si-IGBT for high frequency and low voltage, SiC MOS for high frequency and high voltage, and GaN is used for low voltage power but high frequency. When using Si at low frequency and high pressure

Compared with Si, the on-resistance of SiC can be made lower, which is reflected in the product, that is, the size is reduced, thereby reducing the volume. In the NEV industry, since batteries are also quite heavy, a drastic reduction in other devices will help make NEVs lighter; for example, DC/DC of about 5 kW is about 85% lighter than Si's IGBTs.

Due to cost issues, IGBT will remain the most important application for the next 3-5 years

The reason that currently limits the use of SIC is that the cost is too high and the product parameters are not stable. Currently, the cost of SIC chips is 4-5 times that of IGBT, but the industry expects SiC costs to drop to about 2 times within 3 years. Currently, the model that uses SiC MOS is Tesla's Model 3.

Currently, the main reason hindering the reduction in SiC costs is substrate defects. The strategic marketing director of Applied Materials commented: “This wider bandgap makes the material have excellent characteristics, such as faster switching speed and higher power density, but the main challenge is substrate defects, and misplaced screws can cause “fatal defects”. SiC devices must reduce these defects in order to obtain the high yield required for commercial success.”

Cost reduction and product stability will take time to verify. The core contradiction among domestic manufacturers is domestic substitution. The stability of SiC MOSFET products needs further verification. According to experts disclosed at Infineon's 2020 Power Semiconductor Application Conference, currently SiC MOSFETs have only been implemented for a very short time. Some technical indicators such as short circuit tolerance time have not provided enough verification. A high-end power semiconductor will take a long time from customer certification to product trial application to product batch application. Therefore, in the next 3-5 years, IGBTs will still be mainstream high-end power semiconductor products. SiC will be new in the high-end part There is some gradual and slow penetration in the energy vehicle sector. However, for domestic manufacturers, the core contradiction in the next 5 years is domestic substitution (leading market share from 2% to 20%).

Long-term perspective: While replacing domestic IGBTs in China, there are also forward-looking layouts for SiC

Third-generation materials such as SiC are one of the directions in the evolution of power semiconductor technology. Domestic IGBTs also have some R&D reserves and samples. The following are examples of Star Semiconductor and CRRC Era Electric:

1. Star Semiconductor: The company's SiC-related product and technical reserves are being carried out intensively

1. The company has successfully developed technology related to silicon carbide modules

According to the disclosure in Star Semiconductor's prospectus, the company has developed technologies related to silicon carbide modules, mainly including:

a. Silver paste sintering technology: After sintering with silver paste, the melting point of the connecting layer can reach 900 degrees or more, which is 4 times the melting point of the connecting layer in the soldering process, suitable for applications where the working temperature is above 200 degrees; the electrical conductivity and thermal conductivity of the silver paste sintering layer are 5 times and 4 times that of the solder bonding layer, respectively;

b. Copper wire bonding technology: Compared with aluminum wire, the melting point of copper wire is increased from 660C to 1083C, which can greatly improve the overflow capacity of aluminum wire. At the same time, its thermal conductivity, resistivity, and Young's modulus are all significantly superior to aluminum wire, and its thermal expansion coefficient has been reduced from 23.6 to 16.5 of aluminum wire, which can greatly reduce the stress of the connecting layer during chip operation and improve the chip's ability to withstand power cycles.

2. Reserve progress for the company's key projects

The prospectus describes the progress of the company's reserves for key projects under development. Among them, the fourth reserve is:

1) Project name: Development of power modules for wide bandgap semiconductor devices;

2) Project progress: At present, SiC device modules for photovoltaics have been developed for customers to use in batches, and automotive SiC modules have completed sample certification.

3) The goal to be achieved by the project: further improving the product line, improving SiC devices for photovoltaic applications and SiC module products for new energy vehicles in 2019.

3. The company's future key research and development plans for technology research and development:

It mainly mentions the development of three important products: 1. Development of a full range of FS-trench IGBT chips; 2. Development of next-generation IGBT chips; 3. R&D, design and large-scale production of cutting-edge power semiconductor products such as SiC and GaN: The company will adhere to scientific and technological innovation and continuously improve the power semiconductor industry layout. While vigorously promoting conventional IGBT modules, it will rely on its own expertise to actively lay out wide bandgap semiconductor modules (SiC modules, GaN modules) to continuously enrich its product range, strengthen its competitiveness, and further consolidate its own industry status.

2. CRRC Era Electric: In addition to showing IGBT products, the official website also displays 5 SiC Schottky (SIC SBD products)

Therefore, at present, the SiC industry chain is highly monopolized by foreign countries. In the next 2-3 years, when the cost of SiC is reduced from 4-5 times to 2 times, and the domestic SIC upstream and downstream industry chains are more mature and break foreign monopolies, it is expected that SIC will only begin to increase its penetration rate domestically, and SiC is only a base material. In the future, as SiC technology gradually matures, there will also be SiC IGBT-related products.

In summary, Si IGBT will still be the mainstream of application in the next 3-5 years. The core logic of domestic manufacturers is to increase the share of domestic substrates in the new energy sector of industrial control appliances. Under the general trend of SiC substrates gradually encroaching on the share of Si substrates after 5 years, it is believed that leading domestic power semiconductors with leading technology and high quality can also actively reserve related technologies and products, and actively embrace innovation in this industry.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1