「AI瓶頸交易」引爆上游,誰在瘋狂吸金?

拆解英偉達Vera Rubin機櫃:910萬美元成本背後,誰是AI算力的隱形贏家?

AI基礎設施的軍備競賽,正在進入一個更「燒錢」的階段。

過去市場討論AI數據中心,往往聚焦在兩個問題:一是英偉達GPU夠不夠;二是電力夠不夠。

但Bernstein最新研報給出了一個更直觀的答案: $英偉達 (NVDA.US)$ 下一代Vera Rubin NVL72單個AI機櫃成本約909萬美元,明顯高於此前市場流傳的約800萬美元。而如果要建設1GW級別的Vera Rubin AI數據中心,總資本開支可能高達約473億美元。

這意味著,AI數據中心已經不只是「買顯卡」,而是一整套圍繞GPU、HBM、DRAM、NAND、網絡、電力、液冷和土建的超級資本開支工程。

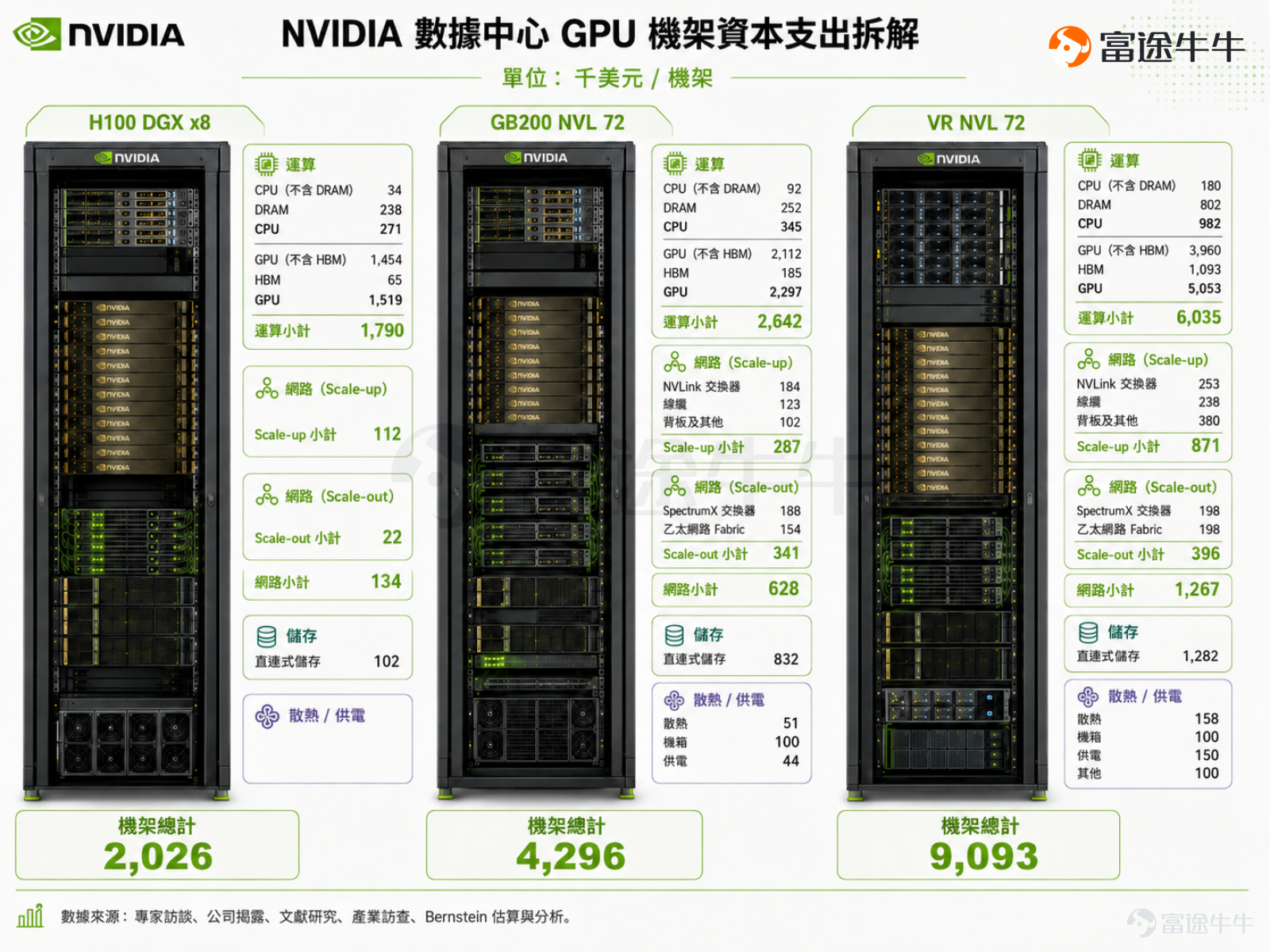

機櫃成本大解密:為什麼高達910萬美元?

伯恩斯坦分析師指出,此前媒體廣泛流傳的「約800萬美元每機架」報價,系基于過時的內存價格,嚴重低估了實際成本。核心分歧在于高帶寬內存(HBM):當前HBM 4價格約為每GB 16.6美元,但預計到2027年Vera Rubin大規模出貨時,價格將升至每GB約53美元,且英偉達很可能通過動態定價機制將成本轉嫁給終端客戶。

伯恩斯坦采用自下而上的方法,對Vera Rubin NVL72機架進行逐項拆解,最終得出約910萬美元的成本估算。

GPU仍是最大單項成本。報告顯示,Rubin GPU售價約為每顆5.5萬美元,每個機架配備72顆GPU,僅GPU本身成本即達396萬美元,占機架總成本近半。此外,每機架36顆Vera CPU合計貢獻約18萬美元。

內存與存儲成本大幅抬升,是本次估算與市場預期產生分歧的主要來源。伯恩斯坦預計該項成本約為320萬美元,遠高于按歷史價格測算的約200萬美元。其中,HBM 4貢獻約109萬美元,CPU DRAM(LPDDR5X)約80萬美元,直連存儲約128萬美元。報告特別提示,內存與存儲價格波動劇烈——NAND價格自2023年4月低點至2026年5月已累計上漲11.3倍,年化漲幅達115%,投資者需持續跟蹤價格變化以維持預測準確性。

網絡、冷卻與供電合計貢獻約200萬美元。其中,網絡成本約127萬美元,包括NVLink交換機約25萬美元、線纜約24萬美元、背板及其他規模擴展組件約38萬美元,以及SpectrumX交換機約20萬美元;冷卻約16萬美元,供電約15萬美元。

打造1GW AI數據中心需要多少錢?

接下來是最震撼的數字。

Vera Rubin NVL72單機柜功耗約220kW。Bernstein假設機柜功耗約占數據中心總功耗的78%,因此折算下來,一個1GW數據中心大約可容納3557個Vera Rubin機柜。

按單機柜約909萬美元計算,僅機柜成本就達到:3557個機柜 × 909萬美元 ≈ 323億美元

如果再加上數據中心的機械電氣、土地、建筑等基礎設施成本,Bernstein估算總成本約為:473億美元/GW,這比Blackwell周期的約405億美元/GW繼續上升,說明AI數據中心的資本密度還在提高。

可以簡單理解為:未來誰想擁有1GW級別的頂級AI算力,賬面上要準備接近500億美元的資本開支。

不過,表面上看,Vera Rubin成本更高。但從算力性價比來看,結論并不悲觀。Bernstein指出,Vera Rubin NVL72單機柜FP8算力約2520 PFLOPS,明顯高于Blackwell NVL72的720 PFLOPS。也就是說,雖然單機柜價格從約430萬美元上升到約910萬美元,但算力提升幅度更大。

這意味著,AI數據中心雖然越來越貴,但每一美元買到的算力仍在提升。這也是為什么雲廠商和AI實驗室仍然愿意繼續投入:在算力緊缺的環境下,新一代GPU的單位算力回報更高,只要下游AI需求繼續增長,資本開支就有繼續擴張的邏輯。

真正的投資主線:AI Capex從「GPU故事」變成「全產業鏈故事」

如果說 AI 發展的第一階段是「得 GPU 者得天下」,那麼進入 Vera Rubin 週期後,高達 473 億美元 / GW 的驚人資本開支,正在宣告一個全新時代的到來:AI 基礎設施的投資邏輯,已經從單一的晶片擴張為涵蓋整個硬體供應鏈的「系統級超級工程」。

當單一 Vera Rubin 機櫃成本飆升至約 910 萬美元,而 GPU 本身「僅」佔近半時,剩下的數百萬美元究竟流向了哪裡?攤開 AI 伺服器供應鏈的全景圖,我們可以清晰看到這場軍備競賽的資金,正全面灌溉至以下五大核心生態系:

1. 核心算力大腦與底層IP:不再只是英偉達的獨角戲

雖然 $英偉達 (NVDA.US)$ 依然是這場盛宴的絕對主角,但整體算力需求的擴張也為其他巨頭留下了空間。美國超微公司與 英特爾正加速追趕,試圖在推理端或特定應用場景分一杯羹。同時,底層架構與客製化晶片需求爆發,帶動了 ASIC 設計服務與IP板塊的繁榮, $博通 (AVGO.US)$ 、 $邁威爾科技 (MRVL.US)$ 以及 $Arm Holdings (ARM.US)$ 成為支撐多元化 AI 算力不可或缺的基石。

2. 記憶體與數據傳輸的「高速公路」:打破頻寬瓶頸的重頭戲

Bernstein報告中最令人意外的成本暴增來自於記憶體與網路。龐大的數據吞吐量讓「算力」與「傳輸」必須齊頭並進。

記憶體: HBM4價格的預期飆升與LPDDR5X的大量導入,讓掌握定價權的 $SK海力士 (000660.KR)$ 、加速推進的 $三星電子 (005930.KR)$ ,以及 $美光科技 (MU.US)$ 迎來量價齊升的黃金窗口。

光通訊:單機櫃網路成本高達 127 萬美元,光通訊產業鏈迎來史無前例的爆發,細分賽道更是百花齊放:

光學IC與DSP:由 $邁威爾科技 (MRVL.US)$ 、 $博通 (AVGO.US)$ 領銜, $MaxLinear (MXL.US)$ 、 $Credo Technology (CRDO.US)$ 與 $MACOM Technology Solutions (MTSI.US)$ 緊隨其後。

3. 算力背後的「軍火製造商」:晶圓代工、封測與半導體設備

再昂貴的設計,都需要極致的製造工藝來實現。

晶圓代工與封測: 絕對龍頭 $台積電 (TSM.US)$ 掌握了先進製程與 CoWoS 封裝的命脈,先進封裝協力廠 $艾馬克技術 (AMKR.US)$ 與 $日月光半導體 (ASX.US)$ 同樣吃下外溢的龐大產能需求。

半導體設備供應商:支撐這些產能擴充的,是上游的設備巨頭們——光刻機霸主 $阿斯麥 (ASML.US)$ 、 $應用材料 (AMAT.US)$ 、 $泛林集團 (LRCX.US)$ 、檢測設備廠 $科磊 (KLAC.US)$ ,以及在特定製程(如晶圓減薄與切割)中扮演關鍵角色的日本廠商 $芝浦機電 (6590.JP)$ 與 $Disco (6146.JP)$ 。

4. 挑戰物理極限的底座:電源管理與系統整合

Vera Rubin 單機櫃功耗高達 220kW,對電力供應與整機組裝提出了極限挑戰。

電源供應與管理: 龐大的電流需要極高效率的轉換與分配, $意法半導體 (STM.US)$ 、 $英飛凌科技(ADR) (IFNNY.US)$ 以及 $Monolithic Power Systems (MPWR.US)$ 提供了關鍵的電源管理晶片(PMIC)與功率元件。

伺服器硬體與系統整合: 最終,將數百萬美元的零組件組裝成 220kW 且能穩定運作的「液冷巨獸」,高度考驗硬體廠商的系統整合能力。 $超微電腦 (SMCI.US)$ 、 $戴爾科技 (DELL.US)$ 與 $慧與科技 (HPE.US)$ 成為這波基礎設施狂潮中最直接的賣鏟人。

總結:一場史詩級的全產業鏈基建紅利

綜合來看,Vera Rubin週期所呈現的高達473億美元/GW估算成本,反映出AI數據中心的建置門檻正在顯著提高。這也標誌著相關基礎設施的投資邏輯發生了轉變:從早期的單一GPU採購,擴展為涵蓋晶圓製造、高階記憶體、光通訊傳輸以及電力與系統整合的整體供應鏈協同佈局。

在「單位算力性價比提升」的邏輯支撐下,雲端服務商對AI基礎設施的資本開支預期仍將維持一定的延續性。未來市場的關注焦點將不再僅侷限於單一核心晶片供應商,而是會沿著整個硬體生態系向下延伸。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論(9)

發表評論

167

524