"Cash is king" narrative continues? Cloud giants snap up long-term contracted capacity

Memory sector hit by pullback! Jensen Huang urgently 'recharges' investor confidence—what’s next?

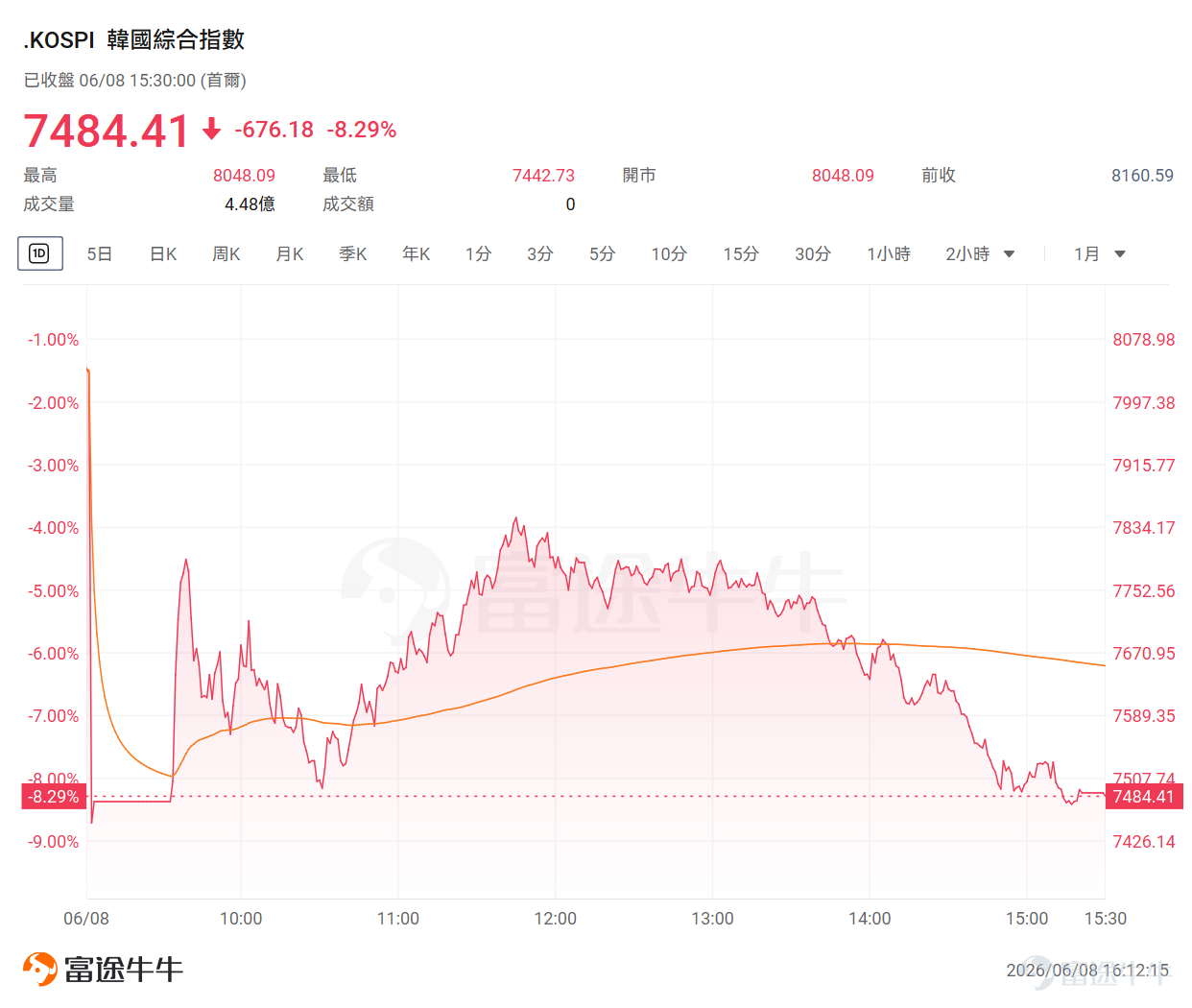

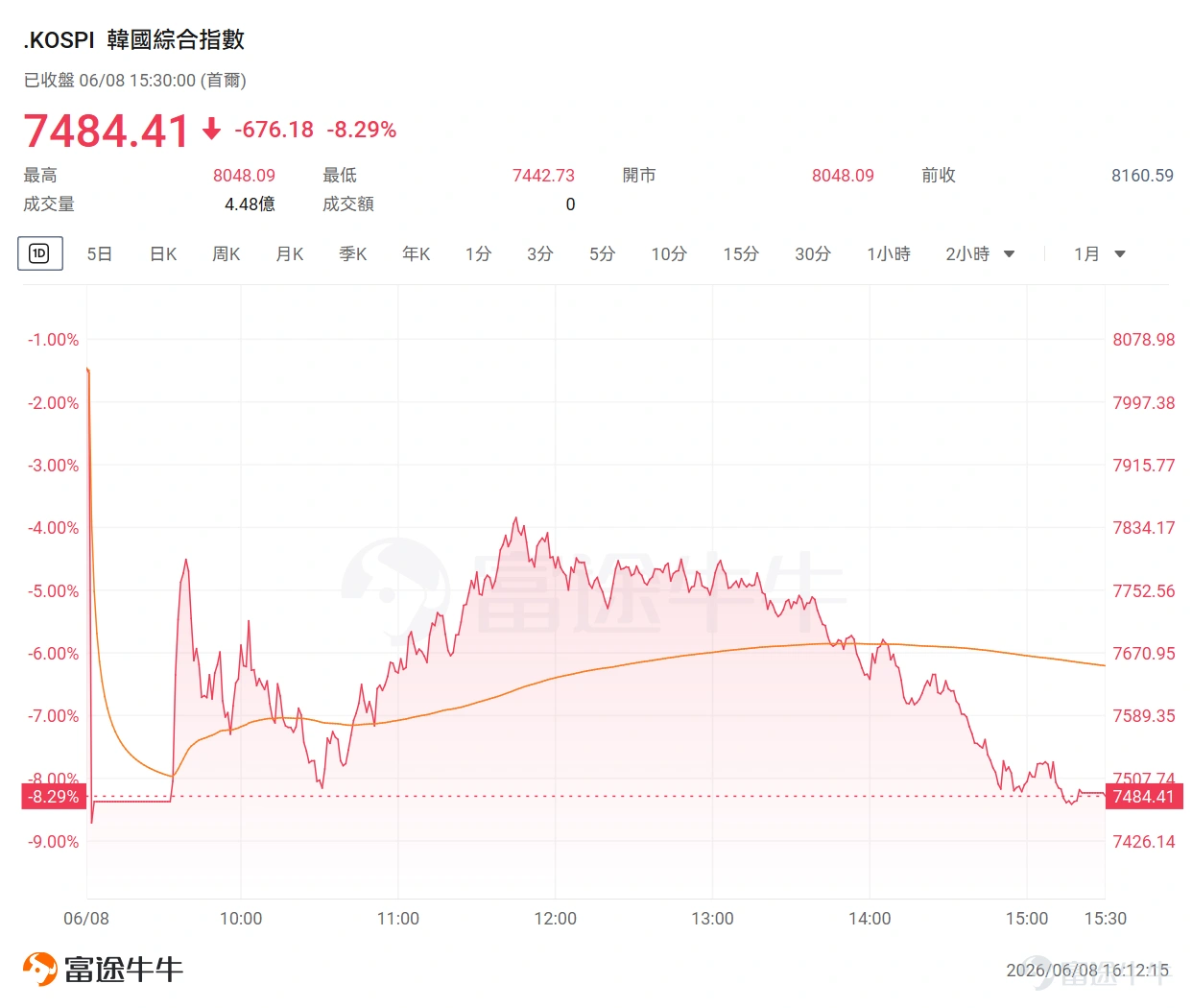

After a globally unrivaled rally, South Korea’s stock market—valued at a staggering $4.9 trillion—has begun showing signs of strain.

Today, $Korea Composite Index (.KOSPI.KR)$ plunged 8.29%, $Samsung Electronics (005930.KR)$ and $SK Hynix (000660.KR)$ share prices dropped more than 10% and 7%, respectively—such unusually sharp swings highlight the current volatility of the index.

This extreme turbulence has inevitably left the market gasping. Many fellow investors likely have one pressing question: Is the recent rally in the memory sector coming to an end? Today, we’ll break down the core logic behind the memory cycle and uncover investment truths amid this market turmoil!

What has recently happened in the memory industry?

The immediate trigger for this downturn in the memory sector was a report released by SemiAnalysis stating that $NVIDIA (NVDA.US)$NVIDIA has drastically cut the modular memory capacity of its next-generation Vera Rubin server rack from 55TB to 28TB, which the market interpreted as a signal of cooling AI memory demand.Following the news, Micron Technology's stock price plunged that day, dragging down the entire semiconductor sector.

Dylan Patel, founder of SemiAnalysis, later clarified thathis analysis "contained no bearish sentiment whatsoever."

According to Barron's, NVIDIA’s reduction in module memory capacity may actually reflect an ongoing HBM crowding-out effect. HBM production is extremely wafer-intensive, requiring approximately three times the wafer capacity per unit compared to standard memory. As HBM supply expands, capacity for other memory types gets squeezed, potentially driving up prices across the entire memory industry.

TrendForce analysts also noted that as HBM technology continues to evolve through 2027, larger die sizes and rising demand will further intensify the crowding-out effect on conventional DRAM capacity. This will give suppliers grounds to raise HBM prices and strengthen their pricing power in next year’s HBM negotiations.

In other words,The SOCAMM capacity adjustment may not signal weakening AI memory demand; it could instead result from the increased production priority given to high-value HBM.

However, just as the market panicked,NVIDIA CEO Jensen Huang issued an optimistic message, stating plainly that he still sees no end in sight for the current memory shortage cycle, with the entire supply chain remaining supply-constrained and strong demand likely to persist for several years.

On Monday, NVIDIA and SK Hynix officially announced a multi-year technology partnership, under which they will jointly develop next-generation AI memory chips and secure long-term supply commitments. This collaboration directly addresses persistent market concerns about memory supply bottlenecks amid the expansion of AI infrastructure.

Even more notably, Huang explicitly stated that he still sees no end to the memory shortage cycle: “From wafers and packaging to silicon photonics, the entire supply chain is supply-constrained.” With AI demand continuing to surge, this tight supply-demand balance could last for several years.

Reframing the investment thesis for memory stocks: Are they traditional cyclical plays or AI-driven growth stocks?

Since the beginning of this year, global memory stocks have continued to rise. At present, the market shows clear divergence in how it prices the memory sector: Is this merely a cyclical rebound, or long-term growth driven by infrastructure restructuring in the AI era?

To understand today’s memory industry, we must analyze it through two distinct frameworks: 'cyclical' and 'growth.'

1. Viewing it as a 'growth stock': The strategic core of AI infrastructure

If the market is willing to assign memory companies growth-stock valuations, the key prerequisite is:High-end memory (e.g., HBM) is no longer a short-term supply-constrained commodity but a structurally scarce resource underpinning AI architecture upgrades.

Pricing logic is shifting: Morgan Stanley points out that memory has become the absolute bottleneck in AI computing infrastructure. As GPU and ASIC clusters evolve toward higher performance, demand for HBM and enterprise-grade SSDs is exploding exponentially.

Business models are being reshaped: Memory used to be at the mercy of market cycles, but Long-Term Agreements (LTAs) are now changing the game. LTAs are converting what was once a highly cyclical business into one with guaranteed revenue streams and high-margin, long-duration cash flows—delivering exceptional earnings visibility for the industry.

The 'Davis Double Play' of valuation and scale:

◦ Explosive growth in Total Addressable Market (TAM): JPMorgan forecasts that the global memory market size will be significantly revised upward between 2026 and 2028, potentially reaching $1.7 trillion by 2028 ($1.237 trillion for DRAM and $454.5 billion for NAND).

◦ Upward shift in valuation anchor: Morgan Stanley estimates that under high LTA (Long-Term Agreement) coverage, pricing memory stocks as ordinary cyclical commodities would lead to severe mispricing. If LTA coverage rises to 80%, the implied blended P/E ratios for Samsung and SK Hynix should exceed 10.5x, marking a valuation leap from cyclical to growth stocks.

2. If viewed as 'cyclical stocks': Beware of speculative dynamics in the latter half of the main uptrend

Despite strong AI-driven demand, the foundational segments of memory (commodity DRAM and NAND) remain deeply tied to traditional consumer electronics such as smartphones and PCs. If the market ultimately continues to trade these as traditional cyclical stocks, we need to monitor the following key variables:

Pricing logic remains unchanged: It still follows the traditional path: 'supply and demand determine prices → prices determine profitability → profitability influences capital expenditure.' The current investment focus is: How much longer can prices rise? Are manufacturers accelerating capacity expansion?

Current cycle status: According to Bernstein, driven by AI and cloud computing, DRAM and NAND contract prices are expected to rise by approximately 60% quarter-over-quarter in Q2 2026, supporting current supernormal profitability for manufacturers.

Risk of cycle peaking: Under the traditional cyclical framework, the current phase appears more likethe latter half of the main upswing rather than the early stage of a bottom reversal.Demand from consumer segments such as smartphones and PCs has already started to weaken. Bernstein forecasts that price increases will significantly moderate in Q3 this year, and with new capacity gradually coming online, sector sentiment could peak in the second half of 2027 and return to normal.

3. Summary: How to navigate the current 'valuation divergence'?

The memory industry is currently in a unique dual-track phase:While fundamentals remain constrained by cyclical swings in consumer electronics, strong demand from AI and HBM is driving a repricing at the surface level.

Investors should adopt a flexible strategy:

1. Upside potential lies in AI: As long as AI capital expenditure continues to rise and HBM long-term contracts remain solid, the high-end memory sector can continue to enjoy the valuation premium typically accorded to 'growth stocks.'

2. Downside risks lie in supply: If HBM supply comes online faster than expected, AI demand slows down, or demand from traditional consumer electronics collapses entirely, the growth narrative for high-end memory will be invalidated, and the entire sector’s valuation will quickly revert to that of a typical 'cyclical stock.'

Which companies in the memory industry deserve attention?

Overall, from Jensen Huang’s strong endorsement to Wall Street giants’ enthusiasm, market sentiment remains highly optimistic about the long-term outlook for the memory industry. We’ve conducted in-depth research and compiled the followingmemory industry chainfor fellow investors’ reference:

I. Core Memory Manufacturers: The 'Absolute Bottleneck in Compute Power' in the AI Era

This segment is the undisputed star of the current super-cycle and the direct supplier of HBM (High Bandwidth Memory) for AI servers.

$SK Hynix (000660.KR)$: The undisputed leader in the HBM space. Currently NVIDIA's largest HBM supplier, thanks to its leading yield and packaging technology in HBM3 and HBM3E. If you're bullish on the continued explosive growth of AI computing power, SK hynix is the purest play.

$Samsung Electronics (005930.KR)$: Global memory giant. Although it initially lagged slightly behind SK hynix in the HBM race, its massive production capacity and resources cannot be ignored. Samsung’s strength lies in its full vertical integration (foundry + memory).

$Micron Technology (MU.US)$: North America's sole memory player and a strong HBM contender. Micron Technology is aggressively pushing into the HBM3E generation, skipping certain intermediate iterations to compete directly with industry giants, and holds significant pricing power in traditional DRAM and NAND markets.

II. The 'Water Sellers': The Underlying Drivers of the Super Cycle

Whether it’s the 3D stacking in HBM or higher-layer-count NAND, extremely complex manufacturing processes are required. Investing in these companies means betting on the certainty of industry capacity expansion and technological upgrades.

$Applied Materials (AMAT.US)$& $Lam Research (LRCX.US)$: The world's two semiconductor equipment titans. Lam Research dominates global etch equipment—each additional layer in 3D NAND requires its etchers—while Applied Materials is irreplaceable in thin-film deposition. The complex TSV (through-silicon via) packaging process used in HBM directly boosts demand for equipment from these two companies.

$Rambus (RMBS.US)$: Memory interface IP powerhouse. As data transfer speeds increase, signal integrity becomes ever more critical. Rambus provides foundational patents and controller IP for high-speed DDR5 and HBM.

$MONTAGE TECH (06809.HK)$: Leader in memory interface chips. With servers undergoing a full upgrade to DDR5, demand for Montage's memory interface chips (RCD/DB) has surged significantly, making them key components driving AI server computing efficiency.

III. Host Controllers and Memory Controllers: The 'Brain' of Memory

Memory dies themselves are merely storage units and must be paired with a controller to enable efficient read/write operations.

$Marvell Technology (MRVL.US)$: Leader in data center interconnects. In addition to its powerful networking chips, Marvell holds a dominant position in memory controllers—particularly enterprise SSD and HDD controllers—and stands as a core beneficiary of AI data center memory architecture upgrades.

$Silicon Motion Technology (SIMO.US)$: World’s largest supplier of NAND flash memory controller chips. Controller chips are essential for PCs, smartphones, and enterprise SSDs alike. Their growth is more closely tied to the recovery of traditional consumer electronics and the widespread adoption of solid-state drives.

IV. Systems and Mass Memory: The 'Foundational Granary' of the Data Explosion

AI model training requires ingesting and storing massive amounts of data, which ultimately must reside on physical flash memory and systems.

$SanDisk (SNDK.US)$: The 'dark horse' standout of this AI cycle and a pure-play NAND giant. Since its spin-off and independent listing from Western Digital in 2025, SanDisk has become a rare pure-play investment target focused solely on NAND Flash and enterprise SSDs. It has perfectly capitalized on the AI data center construction boom—delivering explosive revenue and profit turnaround, with its share price surging dozens of times within just over a year, making it one of the most responsive core assets in this memory super-cycle.

$Western Digital (WDC.US)$ & $Seagate Technology (STX.US)$: The HDD (hard disk drive) duopoly. Following SanDisk’s spin-off, Western Digital refocused on its core HDD business. Despite the rapid rise of SSDs, HDDs remain the most cost-effective solution for cloud providers and data centers to store 'cold' and 'warm' data, continuing to serve as an indispensable foundational component in the AI era.

$Kioxia Holdings (285A.JP)$: A global leader in NAND flash memory supply. Like SanDisk, it is deeply focused on NAND flash technology and is a major player among global memory manufacturers with significant market share.

$NetApp (NTAP.US)$ & $Everpure (P.US)$: Enterprise memory solutions provider. They do not manufacture memory chips themselves but instead integrate them into high-performance 'all-flash arrays' and data management software, serving as critical system optimization experts that enterprises heavily rely on when deploying AI computing clusters.

In addition, for investors bullish on the memory sector but wishing to avoid single-stock exposure, ETFs/funds are the most efficient tools:

$Roundhill Memory ETF (DRAM.US)$ :The world's first 'pure memory' ETF, which strictly screens companies whose core business revenue derives more than 50% from HBM, DRAM, or NAND. Its top three holdings are SK Hynix, Micron Technology, and Samsung Electronics, with a combined weight of nearly 60%.

$Tuttle Capital Concentrated Memory Stack ETF (HBMX.US)$ : An ETF focused on the 'broad memory ecosystem' that aims to overcome AI computing bottlenecks, actively and flexibly selecting companies deriving over 25% of their revenue from the memory supply chain—including HBM manufacturers, advanced packaging, and testing equipment providers. It employs a concentrated active management strategy holding 20 to 35 stocks, encompassing not only traditional memory giants but also advanced packaging firms, outsourced semiconductor assembly and test (OSAT) providers, substrate manufacturers, material suppliers, and semiconductor equipment companies involved in memory production.

A quick heads-up: Futu will soon launch Korean equity trading—fellow investors, stay tuned!

Summary

In short, the recent sharp volatility in South Korean equities and memory sector leaders reflects less an 'end' to the supercycle and more a stress test and valuation reset following a massive rally.

Cycles may rise and fall, but the wave of AI-driven computing transformation has only just begun. Maintaining clear-headed logic amid short-term price swings and long-term industrial upgrading is key to staying ahead in future markets. After a globally unprecedented rally, South Korea’s $4.9 trillion stock market is now showing signs of pressure.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (6)

to post a comment

43

100