The US-Iran peace talks present conflicting narratives! What’s next for oil prices?

Gaozhan Weekly Rate Analysis | Iran Claims Permanent Control of the Strait! Is the Ghost of Rate Hikes Returning?

Issue No. 202611

In our previous column, we analyzed the heightened rate hike expectations and flattening yield curve dynamics following Waller’s appointment.Interest rate hikeBuilding on that foundation, this issue will further analyzeOil price shockImpact on global inflation and policy paths.

Last week, in the U.S.April PCEprice index reached athree-year high, primarily driven by the U.S.-Iran conflict pushing up energy prices. $Brent Last Day Financial Futures (AUG6) (BZmain.US)$ Weekly losses were sharp,11.78%, $Gold Futures (AUG6) (GCmain.US)$ while others rose against the trend,1.32% as markets showed a classicHedgingModel.

This article will systematically analyze the core market contradictions from three dimensions: inflation dynamics, divergence in global central bank policies, and asset pricing logic.

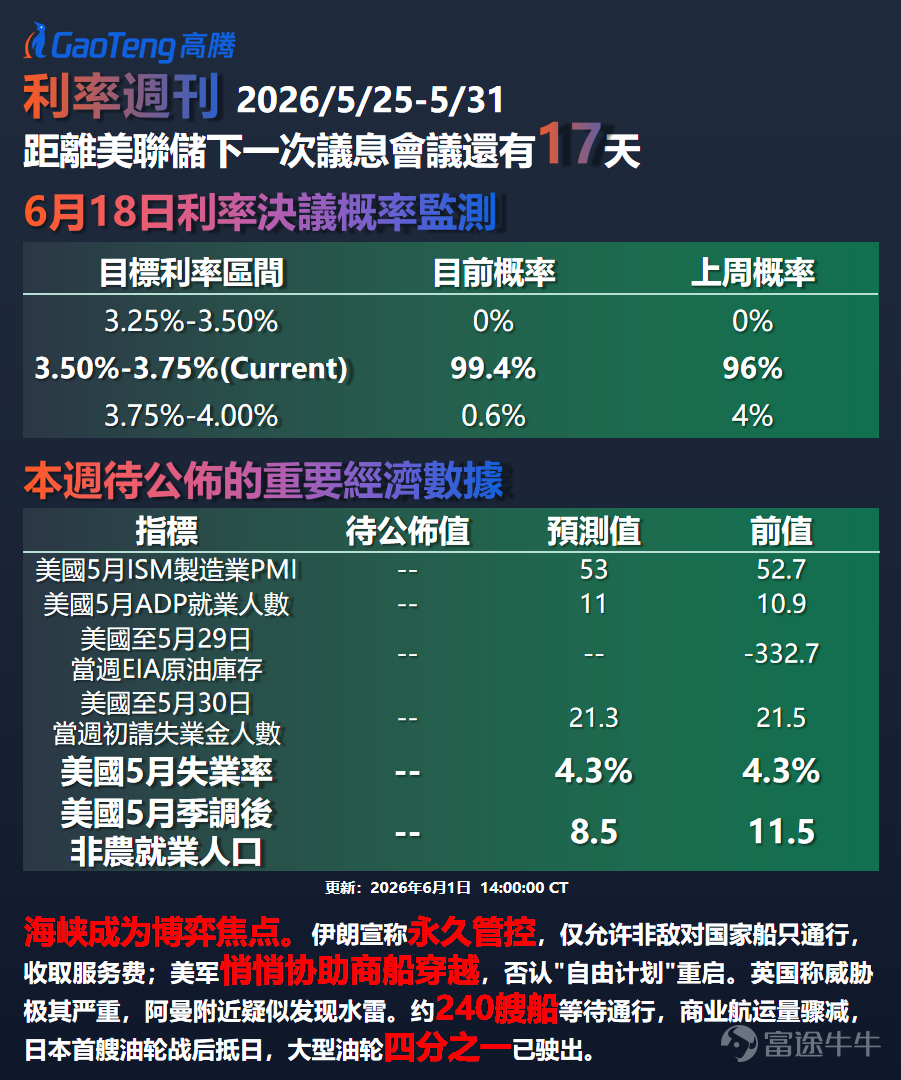

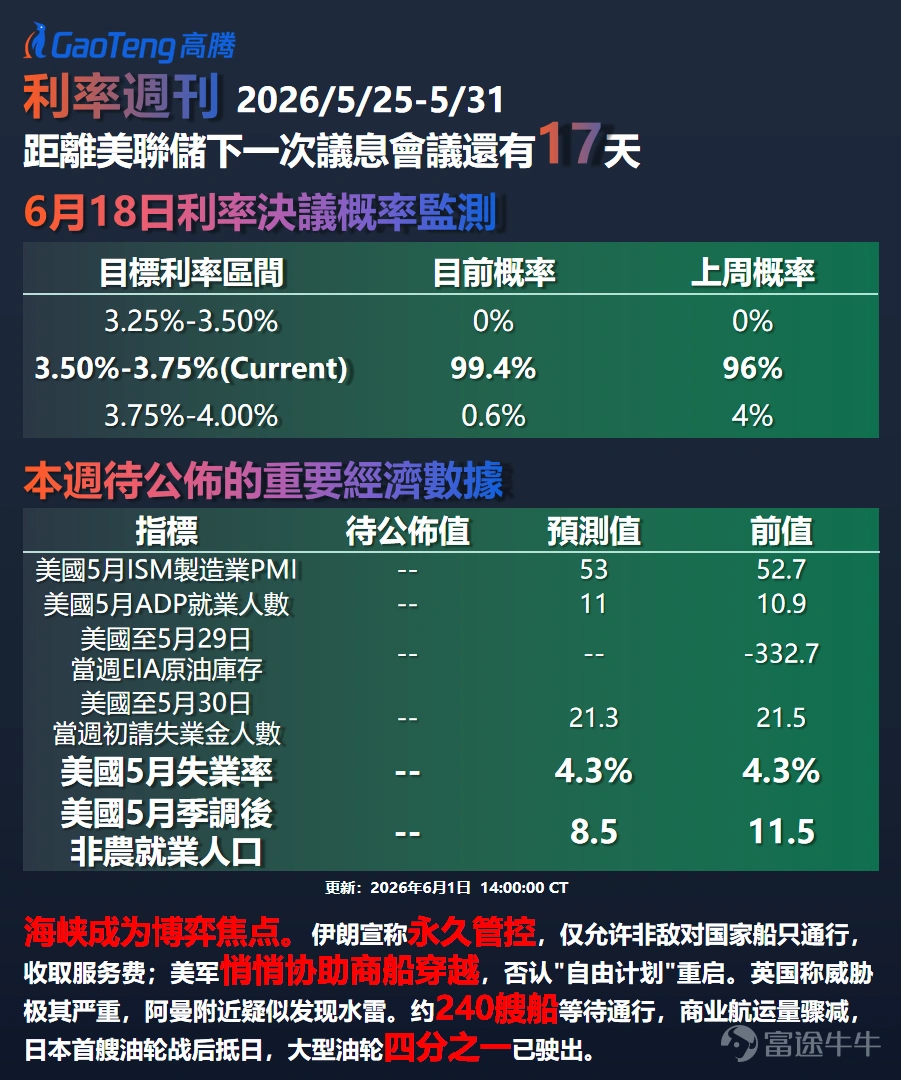

▌FedWatch Data Quick View

According toCME FedWatchData, days until next decision:FOMCMeeting17 days remaining, markets expect rates to remain unchanged3.50%-3.75%unchanged in the Fed’s next rate decision is99.4%,Interest rate hiketo3.75%-4.00%with only a probability of0.6%. Compared to a month ago, when there was still6.7%ofinterest rate cutexpectation, the market has now fully shifted to a wait-and-see stance.

The key drivers arePCEhigher-than-expected readings and escalating geopolitical risks. Demand at short-end Treasury auctions corroborates this outlook—the 4-week Treasury billwas awarded at a rate of 3.630%、with a bid-to-cover ratio of 2.76, capital is still seeking refuge in the short end.

▌ Oil Price Shock: The Specter of a Fifth Oil Crisis

Bank of Japan Governor Kazuo Uedastated bluntly that the world is facing a 'fifth oil price shock'. The U.S.-Iran conflict has driven up energy prices, and the U.S.April PCEhas consequently hit athree-year high.。

HoweverFederal Reserve Governor Bowmannoted that inflation, excluding one-off factors, is only slightly above 2%, and core inflationary pressures have not broadly disseminated.

Unlike in 2022,supply shocksthe current global economic growth is already weak, and rising oil prices are exacerbating the situation.Stagflationrisks.European Central BankThe meeting minutes also noted that upside inflation risks and downside economic risks are intensifying simultaneously.

▌ Fed Watch: Rate Hikes Are No Longer Off the Table

Last week, Fed officials spoke extensively, with an overall tone clearly leaning hawkish.Minneapolis Fed President KashkariThey reiterated that bringing down inflation remains the top priority and warned that the inflation shockwave could persist.Citadel Securitieseven more openly called for a prompt pivot towardInterest rate hike. HoweverCME FedWatchindicating the market still firmly believesJuneNoInterest rate hike—The divergence between expectations and stated positions itself is a key risk signal.

▌ Internal Divisions: Intense Hawk-Dove Tug-of-War

【Hawkish】Minneapolis Fed President KashkariWarned that inflationary ripple effects from Middle East conflicts could persist, emphasizing that disinflation remains the top priority.Chicago Fed President GoolsbeeNoted that expectations of rising productivity could drive increased investment, thereby fueling inflation and forcing the FedInterest rate hike。

【Dovish】Fed Vice Chair JeffersonBelieves current monetary policy is appropriate and expects inflation to ease later this year.New York Fed President WilliamsAlso stated that policy is in an ideal position.

【Centrists】Most officials stressed data dependency, advocating for observing more economic signals before making decisions.

▌ Historical Perspective: Policy Dilemmas Amid Supply Shocks

Soaring oil prices in 2022 once forced the Fed into aggressiveInterest rate hike. But the current environment is more complex—slowing growth coupled withsupply shocks, forcing monetary policy into a more difficult balancing act between fighting inflation and stabilizing growth.

▌ Scenario Analysis: Asset Implications of Two Paths

*Scenario 1 (Persistently High Oil Prices)

Inflation remains elevated, forcing the Fed to signalInterest rate hikehawkishness,US Treasury bondsyields rebound,Goldequities under pressure, and the dollar strengthens.

*Scenario 2 (Easing Geopolitical Tensions)

Falling oil prices have cooled inflation expectations, the Fed remains on hold, and risk assets are rebounding,GoldandUS Treasury bondsbenefiting in tandem.

Current market pricing leans toward Scenario Two, but a flurry of official statements suggests risks are building toward Scenario One.

▌ Other major central bank activities

European Central Bank: Several officials explicitly voiced support fora June rate hike. The ChairLagardeis expected to revise up the inflation forecast, and Chief EconomistLanehinted that there’s no need to correct market speculation regardingInterest rate hike.

Bank of Japan: GovernorKazuo UedaWarningOil price shockcould lead to persistent inflation, and the market expectsJunepossibly in JulyInterest rate hiketo combat inflation.

People's Bank of China: Last week's reverse repo operations gradually increased in volume toRMB 258 billion, with a cumulative net injection ofRMB 558.5 billion, and simultaneously issued in Hong KongRMB 30 billioncentral bank bills, reflecting a refined approach to liquidity management.

▌ Market Reaction: Risk-off Dominates

Last week, the market exhibited a typicalHedgingpattern. $Crude Oil Futures (AUG6) (CLmain.US)$ Down9.53%、Brent crude oilDrop11.78%;

Yields across all maturitiesUS Treasury bondsdeclined across the board, indicating market pricing in rate cuts, $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ Down3.06%to4.437%;

Goldrose against the trend1.32%to$4,569.9;

Hedgingfunds flowed from commodities into bonds andGold, the dollar did not benefit fromHedging, indirectly reflecting market concerns about the US economy.

▌ Closing Remarks

The core conflict this time lies inoil price shockswhich are driving up inflation while economic growth momentum is already weakening.

The Fed is caught in a policy dilemma under the shadow ofStagflation"stagflation"—maintaining a wait-and-see stance could allow inflation to run unchecked, while pivotingInterest rate hikewould weigh on growth.

Investors should closely monitor the upcoming non-farm payroll and unemployment rate data this week, as well asJune FOMCthe meetings andEuropean Central Bankinterest rate decisions; both meetings will set the tone forthe second half of the year andglobal policy direction.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

1