Hong Kong issues its first batch of stablecoin licenses! HSBC and Standard Chartered receive approva

Geopolitical tensions ease, macro headwinds persist as BTC rebounds | Bitcoin | Research Report | Cryptocurrency Market Analysis

This week $Bitcoin (BTC.CC)$ The price rose from 67,291.72 to 73,086.00, with a weekly increase of 8.61% and volatility of 10.85%. Meanwhile, Coinbase's 7-day average trading volume increased by 6.04% compared to the previous week, indicating that the price rise was not due to passive lifting caused by liquidity shortages but rather an expansionary trend accompanied by an increase in spot market activity. In other words, this is a repricing driven by buying pressure.

Meanwhile, global financial markets are caught in a tug-of-war between macro tightening and sentiment rebound. On one hand, U.S. employment and inflation data still indicate tightening; on the other hand, the U.S. and Iran have begun formal negotiations to end the U.S.-Israel-Iran war and reopen the Strait of Hormuz, leading to a strong and sustained market rebound amid suppressed declines.

The crypto market remains in a state of stark contrast—while DAT companies and U.S. equity funds are showing strong inflows, those deep in a bear market continue to sell off their losing positions.

Geopolitics

The U.S.-Israel-Iran conflict remains the most critical factor affecting global financial markets at present.

Earlier this week, Iran accepted a two-week ceasefire arrangement and agreed to negotiate with the U.S. in Islamabad, but the Iranian side clearly stated that this does not signify the end of the war, as the ceasefire is extremely fragile. Subsequently, over the weekend, the U.S. and Iran held approximately 21 hours of talks in Islamabad but ultimately failed to reach an agreement.

At the same time, the U.S. military dispatched a destroyer through the strait and initiated mine-clearing operations, transitioning the shipping route from 'closed' to 'partially restored,' though commercial shipping remains significantly below normal levels and passage continues to be heavily constrained by political and security conditions. Saudi Arabia simultaneously restored its east-west pipeline capacity to 7 million barrels per day, reflecting regional efforts to strengthen alternative export routes bypassing the Strait of Hormuz. Overall, the Strait of Hormuz is not 'back to normal' but has entered a 'fragile high-risk balance under military escort and ongoing unresolved negotiations.'This means that while the oil transport risk premium has declined from the peak period of total blockade, it remains insufficient to fully eliminate geopolitical uncertainty for global energy and risk assets.

However, both sides agreeing to mediate and hold their first round of talks in Islamabad is being viewed by the market as a 'turning point' in the month-long U.S.-Israel-Iran war. The long-suppressed Nasdaq rose for five consecutive days, surging 4.68% for the week, while WTI crude plummeted 14.66% to $95.63 per barrel.

Against this backdrop, BTC ETF inflows totaled $979 million for the week, driving a simultaneous issuance of $1.178 billion in stablecoins. $Bitcoin (BTC.CC)$ This week’s rally can be seen as part of a broader upward repricing of global financial markets following the emergence of a 'turning point' in the U.S.-Israel-Iran conflict.

Macro Finance

Global stock markets surged, pricing in the emergence of a 'turning point' in the U.S.-Israel-Iran war. However, global financial expectations did not improve, instead showing signs of worsening.

This week’s US inflation data for March showed that the CPI increased by 0.9% month-on-month and rose to 3.3% year-on-year, significantly higher than February's 0.3% and 2.4%; core CPI increased by 0.2% month-on-month and 2.6% year-on-year, up from the previous value of 2.5%, with an increase of 0.2% month-on-month and 2.6% year-on-year, up from the previous value of 2.5%. Labor Department data also confirmed this: energy prices in March increased by 12.5% year-on-year, while food prices increased by 2.7% year-on-year.

At the same time, the employment side has not provided a sufficiently clear recession signal. The non-farm payroll employment increased by 178,000, and the unemployment rate remained at 4.3%, still reflecting a state of ‘marginal slowdown but not yet out of control’. Initial jobless claims for the week ended April 4 rose to 219,000, slower than the previous week but still not out of control; the four-week average rose to 209,500, showing that the labor market is cooling down.However, the number of people continuing to claim unemployment benefits is still only 1.794 million, which does not indicate widespread unemployment or systemic deterioration.

Overall, the US is currently closer to a combination of 'marginal growth slowdown + inflation picking up again'.This means that the Federal Reserve will find it difficult to smoothly pivot towards easing due to economic slowdown in the short term, and it may not immediately return to a hawkish stance due to a single month's energy fluctuations; for the market, the real important implication is not 'an immediate resumption of rate hikes', but rather 'short-term valuation enhancement'. The US stock market will continue to face discount rate constraints; as for Bitcoin (BTC) and the crypto market, this means that macro liquidity is temporarily unlikely to provide sustained tailwinds. If there is no stronger capital inflow or structural buying support going forward, the market will more easily maintain high volatility and could even reprice downward.

The current macro environment shows a clear 'triple tightening': the 10-year real interest rate rose from 1.90% to 2.15%, and the nominal interest rate rose to 4.42%; the US Dollar Index climbed from 103.8 to 105.2. On the policy front, interest rates remain in the 3.50%-3.75% range, and the market's expectation of one rate cut by 2026 is only slightly above 20%, forming a significant hawkish repricing.

From the perspective of macro transmission paths, this environment should theoretically manifest as follows: decreased liquidity → reduced market depth → risk assets being more sensitive to sell-offs. However, Bitcoin (BTC) did not fall but instead rose by 8.61%, indicating that the transmission of macro tightening did not fully materialize this week under the context of war-related pricing turning points.

Market Structure

The internal dynamics of the cryptocurrency market show continued weak selling pressure and two-way resonance of capital inflows, providing momentum for a substantial rebound.

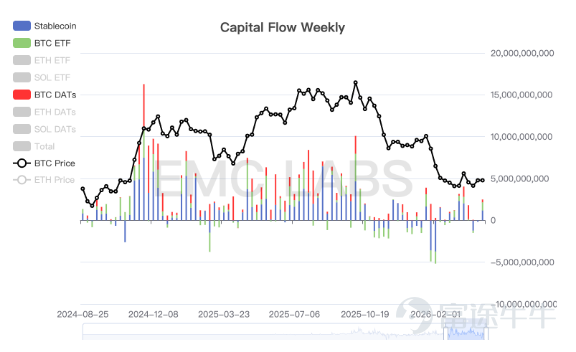

In terms of capital flow, ETFs saw a weekly net inflow of approximately $979 million, with a single-day peak inflow reaching $680 million, constituting a clear source of off-exchange allocation funds. Meanwhile, the total supply of stablecoins increased by $11.78 billion on a weekly basis, and daily fund flows were predominantly net inflows, showing that dollar liquidity on-chain is also expanding simultaneously.

Daily statistics of fund inflows into the cryptocurrency market

This means that this week’s rally is not driven by a single source of funds but rather by simultaneous improvements in both ETFs (the traditional financial entry point) and stablecoins (on-chain liquidity), forming a dual expansion of 'external capital + internal liquidity.' This structure,enables the market to maintain the ability to absorb buy orders even amid a tightening macroeconomic environment.

In terms of market structure, the supply held by long-term holders increased by 33,823.63 units, while the supply held by short-term holders decreased by 30,303.28 units, indicating that holdings are transitioning to a more stable structure. Centralized exchanges sold off 98,050 units, with inventory decreasing by 1,105 units; buying power has declined but continues nonetheless.

This implies that selling pressure is contracting while demand continues.

In the futures market, open interest (OI) increased weekly by 11.17%, significantly higher than the 6.04% increase in spot trading volume; derivatives trading volume also rose by 9.93%. A peak short squeeze of $89,641,255 occurred mid-week, while the funding rate fell from slightly positive to near zero or slightly negative.

This indicates that price increases in the futures market were not driven by crowded long positions but rather by passive short liquidations combined with new position establishment, avoiding one-sided crowding.

Holding conditions have improved somewhat but remain in a 'deep bear market' state.Overall MVRV rose from 1.27 to 1.35, with long-term holder MVRV reaching 1.61, reflecting increased unrealized profits; however, short-term holder MVRV remains at 0.90–0.95, still near break-even. The SOPR indicator similarly shows that most trading occurs around the cost basis rather than through large-scale profit-taking. Long-term holder SOPR briefly rose at the start of the week but remained below 1 for most of the time, implying continued distribution from long-term holders despite price increases, as the group still engages in significant 'stop-loss' selling.

Market Outlook

This week’s rise in BTC was driven by the market pricing in a 'turning point' in the US-Israel-Iran conflict, transmitted via dual inflows into BTC ETFs and stablecoins.

However, the first phase of US-Iran talks ended in failure on Sunday, and whether subsequent renegotiations will resume or tensions reignite remains highly uncertain. If the situation continues to deteriorate, global stock markets will inevitably experience further downward pricing. $Bitcoin (BTC.CC)$ will also follow the downturn.

In addition, the tightening of macro liquidity remains unchanged, and is even intensifying. As 'the leading indicator of global macro liquidity,' $Bitcoin (BTC.CC)$ the future market trend still depends on inflation, employment data, and the Fed's statements.

If the 10-year real interest rate remains above 2.15%, or if the US Dollar Index breaks through 106, macro pressures will continue to strengthen. If ETFs cannot maintain weekly inflows close to $1 billion, or if stablecoin expansion slows, the current capital support will weaken.

We believe that the current rally is more a result of following the broader stock market rather than internal dynamics or cyclical movements. Therefore, it relies heavily on the outcome of the US-Iran negotiations and guidance from macroeconomic and employment data. The height and sustainability of this rebound should not be overestimated.

The above analysis is provided by EMC Labs.

———————————————————————

About EMC Labs

EMC Labs is a partner of Victory Securities, and together they launched the only virtual asset fund approved by the SEC that accepts stablecoin subscriptions — the Victory EMC BTC Cycle Fund. EMC Labs was co-founded by experienced virtual asset investors and data scientists, with a core team from JD.com Finance, Bell Labs, Marsbit, and other companies. EMC Labs has invested substantial resources into building professional engines to analyze BTC on-chain data and technical indicators.

Disclaimer

Investing involves risks, and investors should be aware. The value of securities and investments can rise or fall, and there is no guarantee. Investors may not recover their initial investment amount; past performance does not necessarily predict future results. The securities trading services of Victory Securities are provided by Victory Securities Limited (hereinafter referred to as 'Victory Securities'). This document was prepared and authorized for release on this platform by Victory Securities Limited. The information contained herein is for reference purposes only, and Victory Securities reserves the right to change or terminate without prior notice. All information provided on this platform cannot be reproduced, linked, reposted, or otherwise used by any media, website, or individual without prior written authorization from Victory Securities. Authorized users must attribute the source of this document to Victory Securities and commit to complying with relevant laws and internet usage practices worldwide, refraining from illegal purposes or methods. Violators will bear all related legal and financial responsibilities. Data cited in this document may be sourced from third parties; Victory Securities does not guarantee the accuracy, fairness, timeliness, completeness, or correctness of any data, forecasts, and/or opinions contained herein, nor does it assume legal responsibility for any benchmarks upon which such forecasts and/or opinions are based. Any forward-looking statements in this document should not be considered guarantees of future performance, and actual developments may differ significantly. This document is neither an offer nor a solicitation for the purchase or sale of any securities or investment decision-making basis, nor should it be interpreted as professional advice. Readers or those making investment decisions should fully understand the risks and the associated legal, tax, and accounting implications, and decide whether investing aligns with their personal objectives and risk tolerance, seeking appropriate professional advice if necessary. In certain countries, dissemination and distribution of this document may be restricted by law, and recipients are responsible for compliance with such restrictions.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment