Energy transition accelerates! Which electric vehicle stocks stand to benefit the most amid high oil

[Opportunity Express] Battle at the 30-level! Can Xiaomi hold on?

In 2025, driven by explosive growth in the automotive business and strong performance catalysts, $XIAOMI-W (01810.HK)$ the stock price surged past 60 Hong Kong dollars, with market capitalization nearing 1.6 trillion Hong Kong dollars. However, after the summer peak, the stock entered a prolonged adjustment period. By early April, the stock price had dropped by half from its peak,approaching the psychologically significant level of 30 Hong Kong dollars, returning to the high point set during the previous surge in early 2021.

Today (April 8), tensions between the US and Iran eased, boosting global risk appetite, with Xiaomi surging over 6%. At this juncture, how should we view Xiaomi? What were the reasons for the recent pullback, and what future highlights can be monitored? Let’s dive into this week's Opportunity Express.

Earnings growth shifts gears amid cost pressure headwinds

The continued pullback in stock price is the result of both deteriorating external conditions and internal growth concerns. Although the full-year 2025 performance remains strong, looking at Q4 reveals some underlying concerns.

Q4 revenue reached 116.9 billion yuan, up just 7.3% year-over-year; adjusted net profit was 6.349 billion yuan, down 23.7% year-over-year. This marks a rare quarterly profit decline since the automotive business took off. It clearly indicates that the 'high growth' engine driving the stock price is shifting gears.

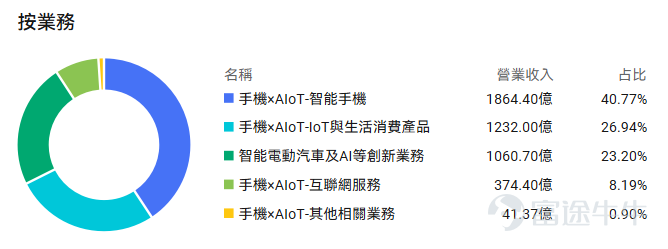

Xiaomi Business Breakdown in 2025

Data source: Futubull

The mobile phone business, as the core foundation, is facing a double whammy of 'weak demand' and 'soaring costs.' On one hand, global smartphone market growth has been sluggish, posing challenges for Xiaomi.The high base effect caused by consumption subsidies over the past 25 years has also started to fade this year.On the other hand,Memory chip prices saw an unprecedented surge starting from the third quarter of 2025, significantly eroding smartphone gross margins, particularly impacting Xiaomi, which is positioned in the non-premium segment.

Data source: Bernstein

On April 3, Xiaomi officially announced a price increase for some models effective April 11, successfully passing on cost pressures to consumers. It remains to be seen whether this will dampen consumer demand.

The automotive business was the star performer over the past year, delivering over 410,000 units in 2025 with a gross margin of 24.3%. However, the market is concerned about its sustainability as upstream lithium carbonate prices rebounded strongly from their lows in mid-2025, driving up power battery costs and pressuring Xiaomi's future automotive gross margins.The high growth base in 2025 makes it more challenging to maintain growth momentum in 2026. The company’s delivery target of 550,000 units set for 2026 implies a significant slowdown in growth. Intense industry competition and public opinion challenges have also added uncertainty to future sales.

Xiaomi Auto Deliveries (Monthly)

Amid expectations of slowing earnings growth, coupled with the recent weak overall market environment in Hong Kong stocks,Xiaomi's trailing twelve-month price-to-earnings ratio has retreated to around 18x, which is now significantly below the five-year average PE ratio. The forward PE ratio for 2026 stands at 19x.The market is repricing, shifting from assigning a high growth premium to scrutinizing its profitability quality and risk resistance capabilities.

Data source: Futubull

Potential future catalysts

Despite short-term pressures, Xiaomi's core business and strategic layout still hold catalysts that could reverse the situation. Xiaomi is making a significant bet on AI, with management guiding total AI investment to reach 60 billion yuan between 2026 and 2028.Its self-developed foundational model MiMo has demonstrated impressive technical capabilities, performing on par with mainstream models like Gemini and Claude across various metrics.

Source: Goldman Sachs.

The integration of AI with Xiaomi's ecosystem is key to building long-term competitive advantages and shedding the label of being merely a 'hardware assembler.' If AI capabilities can be successfully implemented in smartphones, automobiles, and IoT devices, offering differentiated experiences, it will reshape the valuation logic for Xiaomi as a technology company.

This year marks a major product cycle for Xiaomi's automotive business. Currently, Xiaomi only has two models, the SU7 and YU7, but plans call for launching six new or upgraded models this year, covering everything from pure electric to range-extended vehicles and sedans to SUVs. The new generation SU7, unveiled in March, received positive market feedback, and if the new lineup continues to gain market approval, it will strongly support revenue growth and stabilize valuations.

After price increases take effect on mobile devices, although sales may see short-term impacts, gross margins are expected to bottom out and rebound starting from Q2. If memory chip prices stabilize in the second half of the year, margin recovery will become a key driver of profit growth.

Additionally, while growth in consumer lifestyle products (home appliances) has slowed, shipments of large home appliances such as air conditioners, refrigerators, and washing machines reached record highs in 2025, officially entering markets like France and Germany, which could become new growth engines. Meanwhile, amid the trend of explosive growth in AI hardware (such as glasses, earphones, and rings), Xiaomi, which operates one of the world’s largest consumer IoT platforms, may see its ecosystem advantages re-evaluated.

Technical Analysis & Options Strategies

From a technical perspective, the daily chart remains below key moving averages, indicating weak momentum and suggesting an early stage of oversold bounce-back.On the weekly chart, the price broke below the MA 120 line in mid-March. Going forward, attention should be paid to whether the recent rebound can stabilize above this level.

The current area forms a key support zone, which is not only a round-number level but also close to the high point region of 2021, making it technically significant as a strong support.

In the short term, cost pressures on mobile phones and slowing growth in the auto sector are like the Sword of Damocles hanging overhead; stock prices need to find a bottom through earnings validation. However, from a medium- to long-term perspective, the strategic vision of its 'people-car-family full ecosystem' is becoming increasingly clear, with ongoing positioning across AI, autos, premiumization, and overseas expansion. For investors, the current valuation has entered a historically low range, but confirmation of an 'inflection point' still requires patience for fundamental data to stabilize and break out.

From the options market perspective, the IV rank is 19, while the percentile is relatively high at 71%, indicating volatility overall remains in a neutral state.It should be noted that liquidity in the Hong Kong stock options market is relatively insufficient compared to the US market; investors are advised to select contracts with relatively active trading for positioning.

Here are a few strategy references:

(1) Moderately bullish: Bull Call Spread

Buy a call option with a strike price slightly below the current stock price, while selling a call option with a higher strike price. This creates a position with relatively low cost, limited but clearly defined profit and loss. The purchased call option captures potential upside gains, while selling the higher strike price call option effectively reduces the premium costs.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

(2) Existing positions: Covered Call

If you already hold Xiaomi shares and believe there will be short-term fluctuations or mild rebounds, but it is unlikely to quickly break above strong resistance levels, you can sell corresponding amounts of call options to generate additional income, enhance portfolio returns, or lower holding costs.

If the stock price is below the strike price at expiration, the option will expire worthless, allowing the investor to retain the full premium while continuing to hold the stock; if the stock price is above the strike price at expiration, the stock will be assigned at the strike price, enabling the investor to sell at their target price but forfeiting any subsequent upside.

Risk Disclosure: This content does not constitute a research report and is for reference only. It should not be used as the basis for any investment decision. The information involved in this article is not a comprehensive description of the mentioned securities, markets, or developments. Although the source of the information is considered reliable, no guarantee is provided regarding its accuracy or completeness. Additionally, no assurance is given regarding the accuracy of any statements, opinions, or forecasts provided herein.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

28

35