科技巨頭業績大考!Meta績後飆升

Futu Research | Google's 23Q4 financial report review: Limited upside potential

Alphabet, Google's parent company, announced its fourth-quarter financial report after the U.S. stock market on Tuesday. The fourth quarter achieved revenue of $86.31 billion, a 13% year-on-year increase, higher than Bloomberg's consensus expectation of $85.36 billion, with adjusted earnings per share of $1.64, surpassing the expected $1.59. Despite beating expectations in revenue and profit, the stock price performed poorly after the earnings release.

1. Advertising is Google's business pillar, and cloud computing is a key growth driver

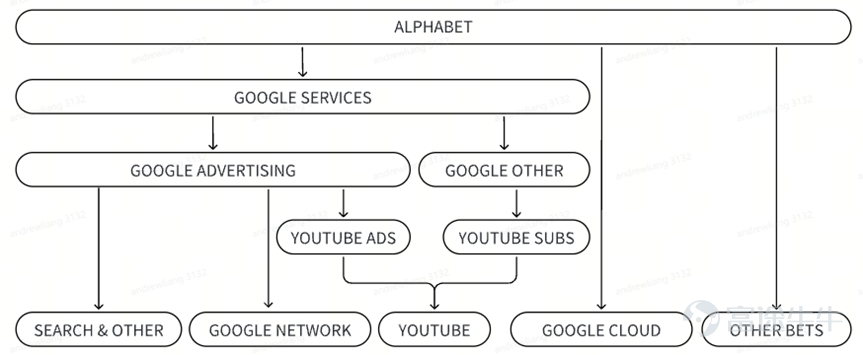

Alphabet is the parent company of Google, with business sectors including Google and Other Bets (innovative businesses). Google's business categories are diverse, primarily including Google services and Google Cloud from a revenue perspective.

(1) Google's services include advertising revenue and other revenue, with advertising revenue accounting for over 80% of Google's total revenue, contributing to the core income source. It can be divided into search ads, Network ads, and YouTube ad businesses, with revenue ratios of around 60%, 10%, and 10% respectively. Google's other businesses mainly include non-advertising businesses of YouTube (mainly user subscriptions) and hardware products Pixel, Fitbit, Google Nest home devices, and Google Play.

(2) Google Cloud can be divided into Google Cloud Platform and Google Work Space, providing cloud services and office assistance.

The advertising business is Google's foundation, with high dependency, determining the overall performance; while Google Cloud is a key growth driver, reflecting the cloud business demand under AI-driven, relating to Google's position in the new round of AI competition, both are indispensable for post-earnings stock performance.

Chart: Google Business Architecture

Source of Information: Company Announcement, Compilation of Futu Securities

2. The performance of the advertising business is not bad, but market expectations are higher

Google achieved a total advertising revenue of $65.51 billion in the fourth quarter, a year-on-year increase of 10.97%, slightly lower than the market's expected $65.77 billion (+11.4%).

In fact, we believe that the performance of the advertising business this quarter is not badThe month-on-month growth rate continues to increase, and the lower-than-expected performance is more due to Google's advertising revenue exceeding expectations significantly for two consecutive quarters, coupled with the ongoing improvement in consumer environment in the fourth quarter, leading to constant adjustments in the market's outlook for the advertising business and raising expectations for Google's ad revenue.

Graph: Google's quarterly advertising revenue (in million USD)

Source of information: Bloomberg, organized by Futu Securities

Looking at the detailed segments of the advertising business, YouTube advertising continues to shine and surpass expectations. YouTube's ad revenue is 9.2 billion USD, with a 16% month-on-month increase, driven by revenue growth in the connected TV segment.

YouTube's content remains highly attractive to users, with continuous growth in quarterly viewing time. In terms of major streaming market shares, the fourth quarter saw an increase in the overall share of cable TV programs due to a large number of sports broadcasts, squeezing the market share of streaming media. However, compared to its peers, YouTube's market share in streaming media remains relatively stable.

The ongoing improvement in YouTube's monetization rate has also driven revenue growth, with monetization efforts including subscription fees and advertising. In July, Google raised the subscription prices for YouTube Music and Premium, and in 2023 introduced features like unskippable 30-second ads and ad breaks. It also heavily promoted ad blockers in the fourth quarter, requiring users to disable ad blockers, otherwise videos will not play, leading users to switch to ad-free premium memberships.

Graph: Major streaming media market shares

Source: Nielsen, Futu Securities compiled

Stable growth in search advertising business, with search advertising revenue of $48 billion, a 9% increase month-on-month. In the medium to short term, Google Chrome browser continues to maintain a stable market share, with Bing not posing a significant threat to Google search. According to Statcounter data, as of the fourth quarter, Google's search engine market share slightly increased to 91.62% (from 91.58% at the end of the third quarter), while Microsoft's Bing market share increased from 3.01% to 3.37%.

Network advertising revenue decreased by 2% year-on-year, which typically refers to advertising content placed on third-party websites through products like Google AdSense and Google Ad Manager, but increased by 8.2% month-on-month, which is not a significant issue.

Chart: Market Share of Major Search Engines

Source: Statcounter, compiled by Futu Securities

II. The increase in AI costs has limited cost reduction effects

In the fourth quarter, the gross margin decreased slightly to 56.5%, and the operating margin decreased to 27.4% month-on-month.

Google's cost reduction measures in 2023 mainly involve layoffs, reduction in office expenses, and expenditure optimization resulting from extending the server depreciation period (from 4 years to 6 years). The latter is primarily a cost reduction achieved on paper through financial means rather than true cost reduction.

Starting from the first quarter, Google has been continuously implementing cost reduction measures such as layoffs, with limited impact on overall cost savings, as it is more of a structural adjustment of costs. This is because most of the eliminated positions are replaced by higher-cost artificial intelligence engineers. Compared to Meta, Google's reduction efforts are relatively moderate, with its total workforce decreasing by only 4% by the end of the third quarter compared to the end of 2022, while Meta Platforms saw a reduction of 23%. Stock-based incentive expenses also increased year-on-year, rising from $19.3 billion in 2022 to $22.4 billion.

Image: Google's cost-cutting plan

Source: Public information, Futu Securities compilation

Moreover, from the perspective of research and development expenses and capital expenditures, Google's investment in AI in the fourth quarter has significantly increased. Research and development expenses increased by 18% year-on-year, with a significantly higher growth rate. Looking at the total capital expenditures from 23Q1 to 23Q3, capital expenditures in the first three quarters decreased by 11.1% year-on-year, due to some projects being delayed. Q4 capital expenditures were 11 billion US dollars, a 45% year-on-year increase, mainly driven by investments in infrastructure, with overall capital expenditures higher than in 2022.

Image: Google's quarterly capital expenditures (million US dollars)

Source: Public information, Futu Securities compilation

Third, Google Cloud's performance slightly exceeded expectations, but still not good enough

The revenue growth rate of Google Cloud is crucial, as it mainly reflects the pull of AI demand on cloud computing. Google's cloud business revenue in the fourth quarter was 9.1 billion US dollars, a 25.6% year-on-year growth, better than the expected 22%, and stabilizing compared to the previous quarter.

Image: Google Cloud business revenue and growth rate (million US dollars)

Source of information: Bloomberg, organized by Futu Securities

However, this growth performance is still not good enough. One reason is that the market's expectations are not high to begin with. The 22% year-on-year growth rate is basically flat compared to the previous quarter. Following the lower-than-expected growth of Google Cloud in the previous quarter, the market intentionally lowered its growth expectations for Google Cloud. Secondly, compared to Microsoft's 30% growth reported on the same day, Google Cloud's performance is relatively weak. Google Cloud's scale is smaller than Amazon and Microsoft, and the market has traditionally had higher expectations for its growth rate.

Figure: Market Share of Major Cloud Computing Providers

Source: Synergy Research Group

However, looking at the performance of recent quarters, Microsoft Cloud, benefiting from the incremental demand brought by AI during the downturn in enterprise IT spending cycle, has seen a smoother growth trajectory. The last quarter even showed accelerated growth. As for Google, Gemini was launched later, and is still catching up with chatgpt. Google also lacks the TOC-end advantage of Microsoft in office software. The incremental demand brought by AI mainly targets TOB customers, making the benefits and the timing of the benefits of Google Cloud later than Microsoft Azure.

IV. How is Google's future viewed?

1. EPS Growth

We continue to look at the two business segments of advertising and Google Cloud for analysis.

(1) Advertising Business: In 2024, it is expected to continue to maintain good growth, with Youtube still being the most promising advertising business.

In terms of the macro environment, according to WARC's 2023/24 global advertising spending outlook, it is projected that by the end of 2023, global advertising spending will reach $963.5 billion, a 4.4% year-on-year increase. Advertising spending is expected to accelerate in 2024, with an estimated 8.2% year-on-year growth. The upcoming U.S. presidential election and the Olympics (scheduled for 2024) will help offset macroeconomic uncertainties for advertising.

The search business will focus on stable growth in 2024. In the medium to short term, Google's position in the search field is difficult to challenge, and the future evolution is more likely to see Microsoft and Google squeeze more market share from smaller search engines. Even if New Bing's user search volume increases, advertisers are not likely to shift budgets quickly until the number of new users reaches a certain scale, preferring to use Google's AI tools such as PMAX to influence ad placements.

(2) Google Cloud's growth rate is expected to stabilize and rebound.

Based on the growth rates of Amazon and Google in the past two quarters, there are signs of growth rate rebound. The trend of cutting enterprise IT spending is slowing down, and cloud computing is expected to stabilize and rebound in growth rate in 2024.

(3) Cost-wise, it is expected to remain significant.

According to the company's guidance, capital expenditures in 2024 will overall exceed those in 2023, meaning that the company will continue to increase capital expenditures and research and development investments. The marginal effect of cost reduction and efficiency improvement will decrease month-on-month, indicating that cost and expense spending in 2024 will not see significant improvements.

Based on the above assumptions, it is expected that in 2024, revenue will increase by 14% year-on-year to $350.7 billion. Due to increased costs, net income is expected to grow by 12% year-on-year to $82.6 billion.

2. Shareholder Returns

In April 2023, Google announced a $70 billion buyback plan (also $70 billion in 2022). As of Q4 2023, Google repurchased $61.5 billion for the full year. Estimated to repurchase $60 billion in 2024, the corresponding shareholder return rate based on the current market cap is 3.1%.

3. Valuation

Google's full-year 2023 free cash flow is $69 billion, with a net profit of $73.7 billion. The current market cap is 27 times the free cash flow and 26 times the net profit. If estimated based on the 2024 net profit, it's equivalent to 23 times the forecasted net profit in 2024. Looking at the valuation range over the past five years, the central tendency is around 26 times, indicating that Google's current valuation has limited upside potential (about 12%).

4. Risks

However, the current valuation is also related to several unresolved antitrust risks facing Google. Let's analyze the impacts in detail:

(1) Google Play Tax: Google lost to Epic and agreed to allow users to download software through third-party channels while providing third-party payment systems. Google's revenue does not separate this business. According to Sensor Tower's data, the App revenue on Google Play in 2023 was about $38.5 billion, with a combined rate at 27%. Since fees may still be charged through third-party payments, the likelihood of small developers developing software independently is low. Estimated based on this, assuming 20% of developers choose to bypass the Google tax, the resulting impact is approximately $2 billion, accounting for less than 1% of total revenue in 2023, with limited impact.

(2) Google Search Monopoly Case: Went to trial in September 2023, expected to last 10 weeks. The federal court believes that Google's position as the default search engine on iPhone's Safari may involve a monopoly. To maintain this position, Google pays a share to Apple. The specific revenue Google obtains from iPhone's Safari search is unknown. Unbinding may affect a small portion of search advertising revenue but would also reduce the share given to Apple. However, considering Google's dominant position in search, the impact on this revenue segment is likely within controllable limits.

Overall, Google's financial report is not particularly bad. The significant drop in the stock price after the earnings announcement indicates that, given the current valuation of technology stocks is not low, investors will also have higher expectations for growth. Google will continue to benefit from the demand brought by AI this year, and related applications are expected to gradually commercialize this year. However, unlike last year, this year investors will pay more attention to the tangible performance improvement brought by AI. From the current valuation perspective, Google's upside potential is relatively limited. It is expected that the stock price will remain in a consolidation phase until there are clear performance contributions or new catalysts.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

17

28