Alibaba released a financial report without guidance, and the mystery is hidden in these two key words.

On the evening of May 26, Alibaba Group (hereinafter referred to as Alibaba)...$Alibaba (BABA.US)$$BABA-W (09988.HK)$Released the fourth quarter and 2022 fiscal year performance report, unlike in the past, this is a report without 'guidance'.

Since mid-March 2022, many companies' business operations have been severely affected by the epidemic, especially in Shanghai. Alibaba stated that due to the risks and uncertainties brought about by the epidemic, many situations are difficult to control and predict. The decision to temporarily suspend the practice of providing financial guidance at the beginning of the new fiscal year is a prudent one.

In the past, Alibaba has always provided financial guidance at the beginning of the new fiscal year, making a prediction about the next financial situation, in order to convey and release some signals to the market. Investors invest in a company, often buying based on expectations.

Although Alibaba did not provide financial guidance as usual this year, by carefully reviewing the entire financial report and closely observing the recent frequent actions and statements of Alibaba's major platforms and management, it is not difficult to find that Alibaba's outlook and 'guidance' for 2023 are already hidden in these two key words: sustainable growth, high-quality growth.

For this question, another perspective can be considered: In the third year since the pandemic black swan flew across the globe, in a business world full of volatility, ambiguity, and complexity, how will Alibaba, with a market cap exceeding $200 billion, find a certain growth opportunity in the next year?

Solidify core competitiveness

The market believes that this quarter's financial report will be a good opportunity for Alibaba to demonstrate its recovery from the heavy blow of 2021. The facts are indeed so: both the quarterly and annual reports exceeded market expectations in revenue and net income—

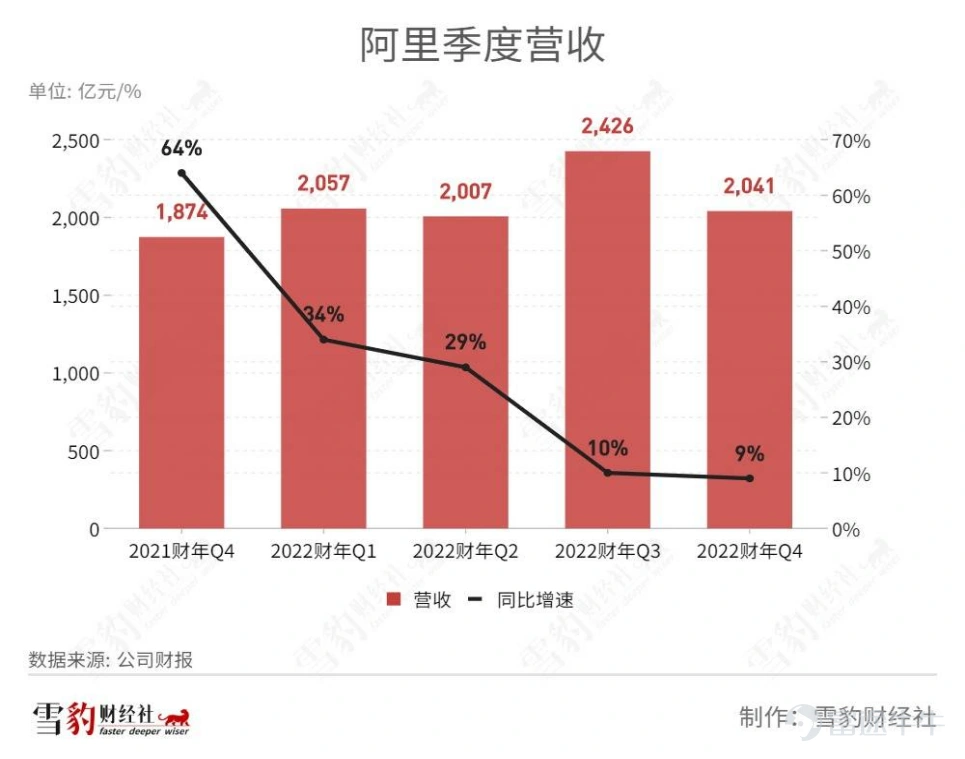

In the fourth quarter of the fiscal year 2022 (January-March 2022), Alibaba achieved revenue of 204.05 billion yuan, a year-on-year increase of 8.9%, higher than the Bloomberg consensus estimate of 200.6 billion yuan; adjusted net income was 19.8 billion yuan, a year-on-year decrease of 24%, but higher than the Bloomberg consensus estimate of 18.5 billion yuan.

In the fiscal year 2022, Alibaba's revenue was 853.062 billion yuan, a year-on-year increase of 19%, higher than the Bloomberg consensus estimate of 850.2 billion yuan; adjusted net income was 136.388 billion yuan, a year-on-year decrease of 21%, but higher than the Bloomberg consensus estimate of 131.7 billion yuan.

Alibaba's financial performance this quarter also outperformed other mainstream domestic e-commerce platforms in the market.

jd.com$JD-SW (09618.HK)$$JD.com (JD.US)$The first-quarter report released on May 17 showed a net income of 239.7 billion yuan, an 18% year-on-year growth. The net loss attributable to common shareholders was 3 billion yuan, compared to a net profit of 3.6 billion yuan in the same period last year.

Although Alibaba's revenue growth rate is not as good as JD.com, which is primarily self-operated, Alibaba is profitable while JD.com is in a loss-making state.

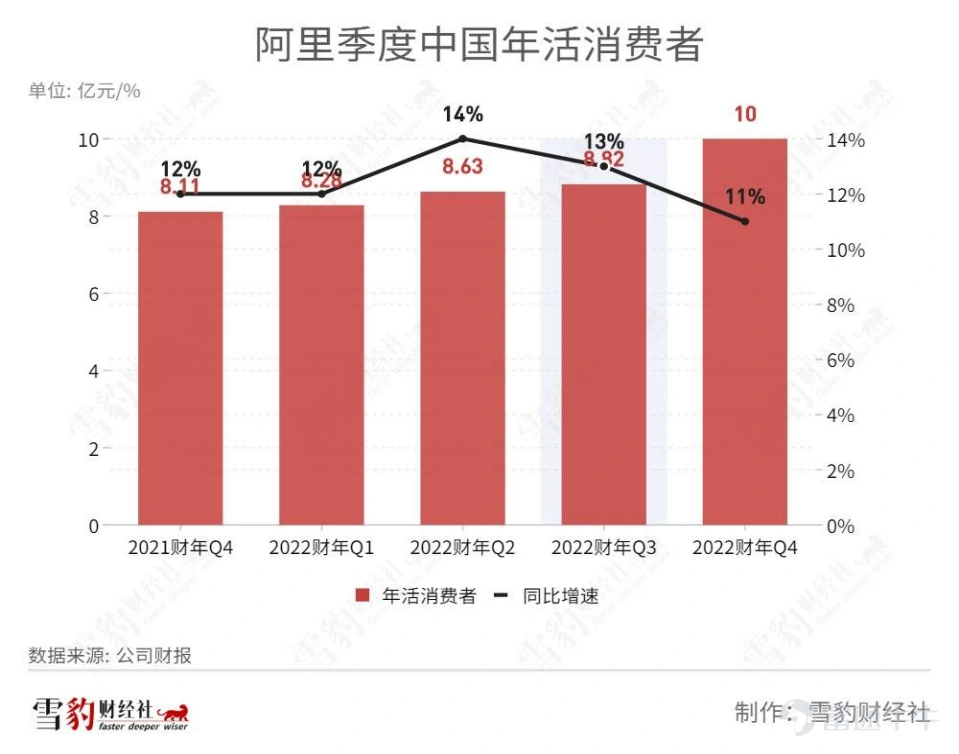

Even as traffic reaches its peak, Alibaba still maintains an annual net increase of 0.177 billion users, with approximately 1.31 billion annual active consumers, including over 1 billion consumers in China and 0.305 billion overseas consumers, achieving the goal set earlier to reach 1 billion annual active Chinese consumers.

During the same period, JD.com's user growth performance was inferior to Alibaba's. JD.com added 10 million new users in the first quarter, while Alibaba added 28.3 million users in the quarter.

For Alibaba, one of the advantages lies in its high-quality consumer cohorts; Taobao and Tmall have become essential parts of daily life for Chinese consumers.

According to financial reports, consumers on Taobao and Tmall continue to achieve high retention rates. In the 2022 fiscal year, over 0.124 billion annual active consumers on Taobao and Tmall had an average spending of over 0.01 million yuan. In the 2021 fiscal year, about 98% of annual active consumers spending over 0.01 million yuan on Taobao and Tmall remained active in the 2022 fiscal year.

A recent research report by Sealand Securities believes that looking at both domestic and international aspects, Alibaba is steadfastly advancing towards its ultimate long-term goal of serving a total of 2 billion consumers worldwide.

Boosted by the financial report news, on the evening of the performance release, Alibaba's U.S. stock rose by over 14%.

The inflection point of growth may occur in the second half of the year.

It must be pointed out that while alibaba is maintaining growth, it is also facing a slowdown in growth. This is due to external pressures such as the macro environment, international situation, and the impact of the pandemic. Under the complex situation and multiple pressures, the slowdown in growth has become inevitable.

Although there is no explicit performance guidance, the management expressed concerns about the second quarter of 2022 during the earnings call.

Due to the pandemic, according to the retail sales data released by the National Bureau of Statistics in April, sales decreased by 11% that month, the most severe decline on record.

Since March, some regions in China have experienced a resurgence in the pandemic, affecting the supply chain and logistics. Some e-commerce platforms have delayed shipments or suspended shipments. According to Anxin Securities, due to the impact of the pandemic, express delivery has been suspended in some domestic regions, affecting the logistics capacity of Tmall Supermarket and Hema.

As for the performance in May, Zhang Yong stated during the conference call, 'In the past week or two, with the recovery of express delivery, including the easing of the situation in Shanghai, the overall situation is gradually improving, but it still takes time to digest the previous parcels.' Therefore, the growth of GMV will also be affected.

Debon Securities believes that with the gradual introduction of stabilizing growth measures, the macroeconomy is expected to reach an inflection point within the year. This will alleviate the pressure on the business growth and profit release of e-commerce platforms, and alibaba's performance will also improve within the year. Currently, merchants in the Taobao e-commerce ecosystem have begun preparations for the 618 promotional event.

In a research report, China Merchants Securities stated that influenced by the macro and competitive environment, the domestic retail e-commerce GMV growth rate has temporarily fallen to a low single-digit level. The short-term pandemic has had a certain impact on residents' disposable income, consumption convenience, and willingness, which is expected to improve after the pandemic.

On May 20, during an online exchange with 300 Alibaba merchants, Zhang Yong mentioned the uncertainty of the overall situation multiple times. He said, "I like to quote an old saying, 'Strive to find certainty in uncertainty.' In this special period, we are doing as much as we can to provide certainty to merchants through Alibaba's services."

Regarding the impact of the epidemic on e-commerce, Zhang Yong reiterated his views during the financial report conference call. He stated that ensuring the stability and smoothness of the supply chain and logistics with certainty under the uncertain epidemic situation is essential for stable business operations and the recovery of consumer sentiment and willingness. Whenever the supply chain and logistics are smooth, it is the lifeline of e-commerce, and even all economic development.

According to the opinions of multiple institutions, the market generally believes that a significant turning point in performance improvement may occur in the second half of the year. This is also a challenge faced by all enterprises and merchants: adapting to the new growth cycle under the epidemic, striving to find certainty in uncertainty.

Regarding high-quality growth.

An industry consensus is that e-commerce has transitioned from a focus on traffic to retention.

This judgment is reflected in business operations, where the current industry has limited space for new user growth, and the next battleground for users is user quality and operational capabilities. According to a report by CNNIC (China Internet Network Information Center), the scale of Chinese internet users was 1.032 billion by the end of 2021. Alibaba reported that it has successfully completed its target of serving 1 billion annual active consumers in China.

How to serve such a large user cohort?

Internally at Alibaba, starting from Taobao Tianmao, a return from focusing on speed to focusing on experience is underway.

It is understood that in the new fiscal year, Taobao and Tmall have already anchored the goal of fully improving consumer experience. Zhang Yong has emphasized on multiple occasions that consumption is not just a trade. Before the consumption behavior occurs, it can better establish consumer mentality, stimulate consumption interest, and thus influence consumption decisions; after the consumption behavior occurs, it can better improve fulfillment and post-sales experience.

For example, this year, Alibaba has been strengthening its self-operated business. In the first quarter, the Tmall App added the 'Cat Enjoy Self-Operated' and 'Cat Enjoy Flash Sale' sections, where some Cat Enjoy self-operated products enjoy services such as home delivery and guaranteed compensation if not delivered. This is an expansion of Alibaba's e-commerce platform diversification, transitioning from light to heavy, from traffic to physical entities, and Alibaba will face a whole new challenge.

What is certain is that from the far field to the near field, combining platforms with self-operated, relying on a multi-scene consumer app matrix across multiple businesses, supporting merchants to serve China's largest high-quality consumer cohort with multilevel fulfillment services is one of Alibaba's certainty paths towards future high-quality growth.

The shift from speed to experience return is essentially seeking high-quality growth, which has also been repeatedly reflected in this financial report.

Zhang Yong stated in the financial report: 'We will continue to strengthen the construction of digital business infrastructure, focus on high-quality growth, and create long-term value for customers, shareholders, and other stakeholders in the ecosystem.' CFO Xu Hong stated: 'We are determined to focus on sustainable, high-quality revenue growth, concentrate on optimizing operating cost structure, and enhance overall returns in uncertainty.'

Not only emphasizing 'high-quality revenue growth,' in the 'Business and Strategic Progress' section of the financial report, the management reiterated for the third time: 'Looking ahead to FY 2023, our operational principles include a focus on creating sustainable, high-quality revenue growth.'

Zhang Yong has repeatedly emphasized 'believing in the power of consumption in economic development.' What changes are the consumption trends, while the unchanged are the consumption demands themselves. Undoubtedly, Alibaba's core strengths are distinct in this respect.

During the analyst conference call, Zhang Yong also said that historically, the development of any economy always progresses through twists and turns. Long-term, believing in the resilience and potential of China's economic development, at this particular time, will solidify the business foundation, focus on innovation and customer value, and plan well for Alibaba's long-term development.

However, it must also be acknowledged that Alibaba's development is closely related to the global economy. Faced with the uncertainty of the global economic environment, what is the 'anchor' that determines Alibaba's future performance growth?

Zhang Yong stated that a key factor in high-quality growth is high-quality technological innovation. Alibaba will leverage high-quality technological innovation to develop and utilize the vast potential of cloud computing. Cloud computing and big data services are fundamental services required by every enterprise and industry for digital transformation. Looking ahead, China's cloud computing industry is a vast market exceeding trillions of yuan.

In the past year, Alibaba has invested over 120 billion yuan in technology-related costs. In the past three years, over 60% of Alibaba's patent investments have been concentrated in hardcore technology areas such as cloud computing, artificial intelligence, and chips, with the cloud computing field's patent authorization volume growing at an annual rate of over 50%.

These investments are not only results but also the foundation for the high-quality development in the next phase. Once the industry enters a recovery cycle, Alibaba will have more possibilities. In other words, it is expected to be one of the earliest companies to recover and emerge from the cycle.

In fact, some savvy institutional investors have already entered the market before the financial reports were released.

According to the 13F holding documents submitted to the U.S. Securities and Exchange Commission (SEC) by multiple well-known institutions for the first quarter of 2022, Alibaba is still the most favored Chinese concept stock by institutions, with a total of 1247 institutions holding positions in Q1 2022, and 76 institutions listed it as one of the top ten heavily weighted stocks.

According to Whalewisdom data, the world's top hedge fund Bridgewater Associates significantly increased its holdings in Alibaba and Nio in the first quarter of this year.$NIO Inc (NIO.US)$, Xiaopeng$XPeng (XPEV.US)$Hold positions in more than 20 popular china concept stocks. Bridgewater's top 10 holdings include alibaba, coca-cola. $Coca-Cola (KO.US)$, Pepsi$Coca-Cola (KO.US)$, Costco$Costco (COST.US)$, etc., totaling 33.94%, with Alibaba ranked sixth in position.

Singapore's sovereign wealth fund Temasek's top 10 holdings in the first quarter include blackrock. $Blackrock (BLK.US)$Visa$Visa (V.US)$Paypal$PayPal (PYPL.US)$Mastercard$MasterCard (MA.US)$Alibaba and others together account for 54.05% of the total holdings, with Alibaba's position ranking sixth.

The financial report shows that on March 22 of this year, Alibaba's board of directors has authorized an expansion of the share repurchase program, increasing the total amount from $15 billion to $25 billion. As of March, $9.6 billion has been used.

(Authors: Yi Ming, Chen Zhongshan)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

1

18