Global tourism recovery accelerating, Fosun Tourism (01992) may welcome valuation repair.

In November of last year, the sudden emergence of Omicron caused a sharp drop in the European and American stock markets, however, the market overestimated the toxicity of Omicron. The high transmission rate means low toxicity, which supports market confidence in mild cases. The US travel services sector began to rebound continuously in late December, and the market remains bullish on the future recovery of the travel industry.

Since 2022, the new cases of Omicron in Europe and the United States have replaced Delta. Despite the continuous increase in the number of new cases, they are generally mild. Moreover, European countries have not implemented strict restrictions on tourism, with most countries requiring vaccination and a 48-hour negative test certificate. Travel bans are the biggest risk to the tourism industry. In Europe, the mild symptoms of Omicron have led some countries to relax restrictions, such as Germany gradually lifting the blockade on the United Kingdom. This is also why the travel services sector has become less sensitive to the increase in new cases.

According to the Wall Street News app, the leading comprehensive travel$FOSUN TOURISM (01992.HK)$In December, the 2021 Investor Day was held, expressing optimism towards the tourism industry, and also recently announced the 2022 New Year operating data. Despite the epidemic disruption, during the New Year's period, Club Med's turnover increased by over 50% compared to the pre-epidemic New Year in 2020, and the turnover of Atlantis Sanya grew by 12% year-on-year.

Fosun Tourism and Culture's stock price has been consolidating at a low level for nearly five months, lacking driving factors in the short term under the bearish impact of the epidemic. Looking ahead, the industry's recovery trend remains unchanged. In the beginning of 2022, Fosun Tourism and Culture's operating performance exceeded expectations, providing an opportunity for upward valuation adjustment.

The European and American tourism markets are accelerating recovery, brewing a new landscape for the industry.

From a global perspective, the compound annual growth rate of the global tourism industry was 4.3% from 2015 to 2019, with China's growth rate much higher at 13.75%. The industry experienced a significant decline in 2020 due to the pandemic, but continued to recover in 2021, with a strong outlook expected for 2022. The core of the global tourism market includes China, Europe, and the Americas, with some variations in performance between the three major markets in the first and second halves of 2021.

The Chinese market had a strong performance in the first half of the year, but the recovery slowed down in the third quarter due to local outbreaks. According to data from the Ministry of Culture and Tourism, in the first three quarters of 2021, total tourist arrivals and tourism revenue increased by 39.1% and 63.5% respectively year-on-year. Despite ongoing local outbreaks during the New Year holiday in 2022, provinces like Sichuan, Hunan, and Beijing saw a double increase in tourist numbers and revenue, with Beijing's tourism revenue doubling, showing a rapid overall recovery trend.

The European and American markets were only affected by the pandemic starting in Q2 of 2020. In the first half of 2021, the European tourism industry was significantly impacted, while the picture in the Americas was quite optimistic. Contrary to the overall and domestic performance after the third quarter, the industry's strong recovery led to good performance growth for most overseas travel companies. Taking the example of the USA market, according to Morgan Stanley research, the Q4 RevPAR in the USA only decreased by 4% compared to 2019, far higher than the expected 16% decrease, and forecasted growth in the RevPAR by 14% and 7% in 2022/2023.

In fact, the pandemic is reshaping the tourism industry structure in the three major markets. In 2020, most tourism companies incurred losses, with some participants being eliminated from the market. The industry started to recover in 2021, combined with the expectation of new drugs coming out, leading companies driving growth, and further market share concentration. Changes in consumer behavior among the middle class, affluent population, and the younger generation are reshaping the industry landscape.

Under the structural adjustment, the tourism industry may follow two trends: quality products and services being in high demand, while poor products and services will lack interest. Fosun Tourism, as an industry leader, has shown resilience in both the challenging year of 2020 and during the industry recovery in 2021, having the ability to consistently introduce innovative products. It may emerge as the biggest beneficiary in this industry structural adjustment.

Industry leaders continue to strengthen as business recovery exceeds expectations.

Fosun Tourism's performance recovery is ahead of its peers, with a significant 91% increase in Club Med's operating revenue in Q3 2021. The capacity has recovered to 72% of 2019 levels, surpassing the profit level from the same period in 2019. In the second half of the year, the overall company orders have already reached 83.8% of the same period in 2019. Although the capacity of the resorts has reached 72% in Q3, there is continuous improvement, with expectations of maintaining high capacity in Q4. During the New Year holiday in 2022, Club Med's operating revenue performed remarkably well, significantly surpassing pre-pandemic levels, with some Chinese resorts achieving an occupancy rate of 90%.

Club Med's strong performance recovery is mainly attributed to its four-dimensional strategy: namely, upscale, digitalization, eco-friendliness, and globalization. The proportion of high-star hotels in the company has been increasing year by year, now exceeding 90%. Supported by technology, digital transformation continues to empower business operations and reduce costs. Building an eco-friendly FOLIDAY ecosystem centered around family users, the company continuously enhances its ecosystem through acquisitions. With global asset advantages, it has presence in over 40 countries and regions.

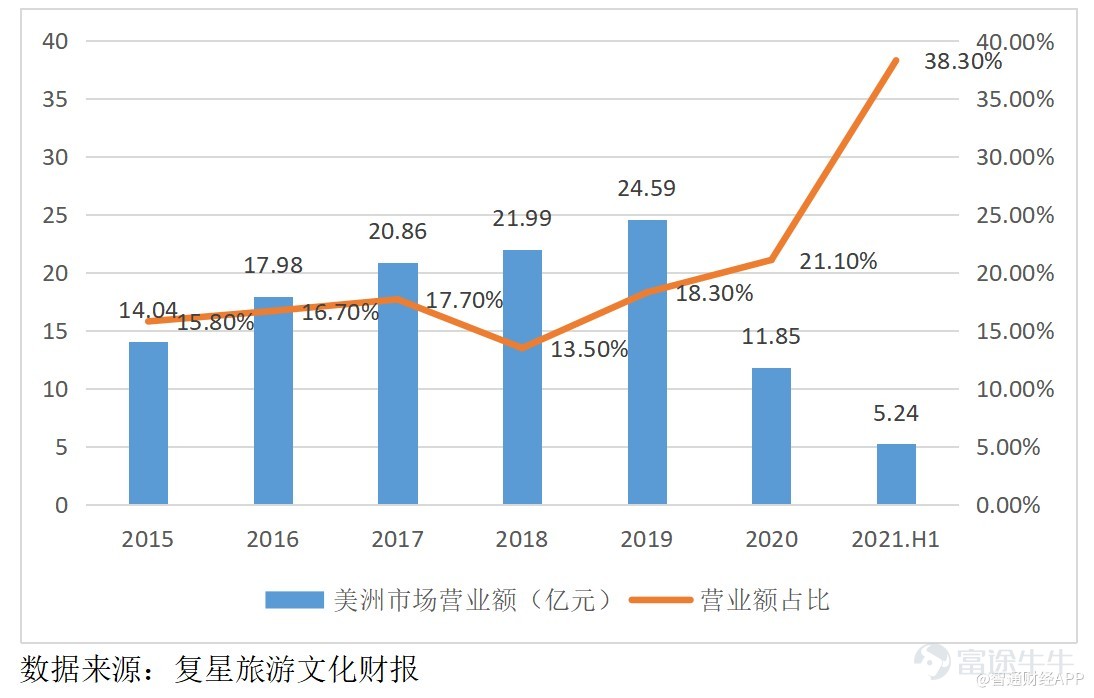

In 2019, the company's revenue in the European and American markets accounted for 82% of Club Med's total, which was acquired by Fosun in 2015. Since then, the performance in major markets has continuously hit record highs. From 2015 to 2019, the compound growth rates of revenue in Europe, the Middle East, the Americas, and the Asia-Pacific region were 9%, 15%, and 16% respectively. In 2020, there was a significant decline, but in the first half of 2021, the Americas market showed strong recovery, increasing its revenue share to 38.3%.

Under the "Four Transformation" strategy, the company's solid ecosystem continues to create products and services that are more competitive than its peers, attracting more tourists and expanding market share.

The FOLIDAY ecosystem framework continues to enhance and expand the matrix of Club Med and tourist destination projects by operating Sanya Atlantis, acquiring the Thomas Cook brand, and creating the FuYouCheng brand domestically, among others. At the same time, improving peripheral supporting services and increasing the attractiveness of one-stop service pricing, including entertainment projects, Fanxiu, mini-camps, and AiBinong, not only enhances revenue generation for business operations but also adds new sources of income.

Since its operation in 2018, Sanya Atlantis, as the first domestic tourist destination, has maintained strong growth levels. In the first and second quarters of 2021, it maintained strong double-digit growth, although there was a slight decline in the third quarter due to localized domestic epidemics. However, the overall performance is excellent, with annual revenue from June 2020 to June 2021 reaching 1.73 billion yuan, a 32% increase from 2019. Based on the data from the New Year's Day holiday in 2022, revenue has grown by double digits, and Sanya Resort has also reached nearly 90% occupancy.

It is worth noting that FuYouCheng may become a new bright spot in performance. Lijiang FuYouCheng began operation in the fourth quarter of 2021, while the property part of Taicang FuYouCheng has been presold. The project includes Club Med, Casa Cook, and will also build the leading indoor skiing venue in East China. The Alps Snow World, Snow World, and Club Med are now in full construction, and it is expected that Club Med Joyview will start trial operations by the end of 2023.

Expansion is steadily progressing, potentially welcoming opportunities for the right-side layout.

It is understood from the Zhitong Finance and Economics app that during the epidemic period, the company did not stop its development pace. In early 2021, a plan was made to open 16 new resorts by the end of 2023, eight of which are located in China. By June 2024, renovations of 12 existing resorts globally are planned to be completed. In September of last year, Lijiang successfully opened, followed by a new ski resort in Quebec, Canada, marking its first entry into the North American market.

Ice and snow tourism is brewing a trillion-dollar market. In February of last year, the Ministry of Culture and Tourism and other departments jointly issued the "Ice and Snow Tourism Development Action Plan (2021-2023)". In October, the Ministry of Culture and Tourism classified ski resorts, as the Beijing Winter Olympics approaches, provinces will make full efforts to achieve the goal of "encouraging 300 million people to participate in ice and snow sports." From this year's New Year's Day data, ice and snow tourism has sparked a climax, becoming a hot spot in tourism projects.

The company is the largest provider of skiing facilities in europe, actively catering to the development trend of ice and snow tourism, by 2023, it is expected that there will be 6-8 Club Med ice and snow resorts in the northeast asia region. In China, Club Med changbai mountain resort is scheduled to open at the end of January this year, located in the changbai mountain international ecological tourism resort demonstration area, and the alps snow world is also steadily progressing, with a comprehensive opening expected in 2023.

In summary, despite the significant challenges still faced by the external environment, the mild cases are gradually weakening the impact of the new crown on the tourism industry, and in the long term, the recovery trend remains unchanged. The industry is brewing a new pattern, with fosun tourism having scale advantages, product competitive advantages, market layout advantages, etc., leading in business recovery capabilities compared to peers, it is expected to maintain a leading position in the new pattern and continuously capture a larger market share.

For 2022, Club Med continues to recover, Sanya Atlantis maintains strong growth, while the Foye City Taicang and Lijiang projects may become new growth highlights, and the trend of tourism + culture integration also brings more revenue to the company's surrounding service products. The plan to open 16 new resorts in the next two years is steadily progressing, with long-term performance growth sustainability. The company's stock valuation is consolidating at the bottom, looking at the monthly chart, it may usher in an opportunity for a right-side layout.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4