The Real Reason Behind Micron's Surge: No Longer a 'Cyclical Stock'—UBS Group Is Revaluing It as a 'Growth Stock'

Author: XinGPT

Micron surged sharply today, with one key reason being that UBS Group directly raised its price target for Micron to USD 1,635!

Therefore, I carefully reviewed UBS Group’s report released today, which significantly upgraded Micron’s rating—the core change lies in the valuation methodology.

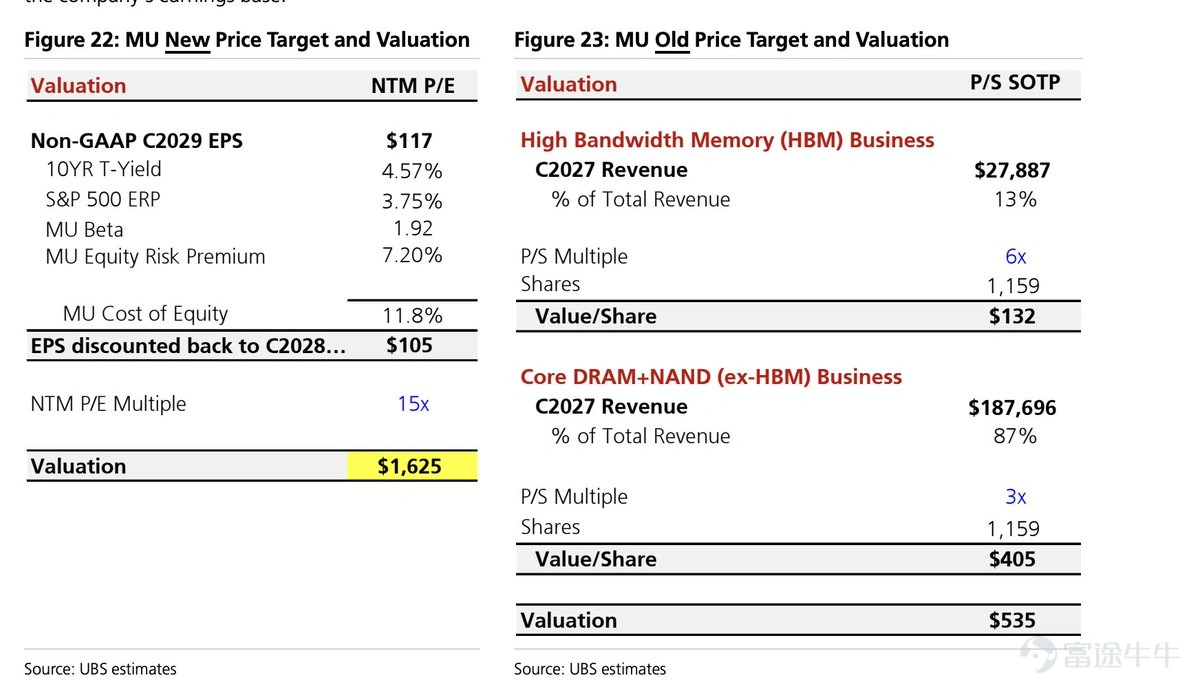

Previously, UBS Group valued Micron using a sum-of-the-parts (SoTP) approach based on price-to-sales (P/S) multiples, breaking Micron into two segments:HBM business and core DRAM+NAND business。

The HBM segment, benefiting from AI server demand and exhibiting faster growth, was assigned a higher multiple—valued at 6x P/S on projected 2027 revenue of approximately USD 27.89 billion, translating to roughly USD 132 per share;

The core DRAM+NAND segment was valued at 3x P/S on projected 2027 revenue of approximately USD 187.7 billion, corresponding to roughly USD 405 per share.

Adding the two parts together yields the original target price of USD 535. The implicit logic behind this approach is that Micron remains a strongly cyclical memory company, but its HBM business is of higher quality, warranting separate revenue multiples.(Figure 1)

UBS has now switched to an overall P/E-based valuation, raising its target price from USD 535 to USD 1,625. The new methodology applies a forward P/E multiple of approximately 15x to 2029 EPS of about USD 117 and discounts it back to 2028 using an equity cost of around 12%.

UBS selected 2029 EPS because it believes that by then, the model will already incorporate a mild downturn in the memory cycle. If Micron can still generate EPS above USD 100 at that point, it would indicate earnings are not merely driven by peak-cycle dynamics but reflect a more 'cycle-resilient profitability.' (Figure 2)

The core reason for this shift in valuation methodology is LTAs—long-term agreements.

UBS believes that the latest generation of enhanced LTAs not only locks in shipment volumes but also includes commitments for fixed quantities over three to five years and partially fixed pricing mechanisms. It estimates that roughly 20% to 30% of industry DDR shipments in 2027 will be covered by such agreements—about 20% for Micron—and that hyperscalers have already locked in approximately 60% to 70% of the industry’s server DDR5 volume. As a result, Micron’s revenue and profit visibility improves, and peak-to-trough fluctuations in DDR pricing could be reduced by roughly half.

Therefore,UBS concludes that Micron is no longer just a company profiting from upswings in the memory price cycle; rather, thanks to AI demand and long-term agreements that lock in both price and volume, its earnings stability has been systematically enhanced.

Consequently, the valuation framework has shifted from 'segmented revenue multiples' to 'consolidated earnings multiples.' The key change is an upgrade from 'revaluing HBM separately' to 'revaluing Micron as a whole.'

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1