Raised $1.3 Billion in Seven Weeks, Yet SpaceX’s Weight Halved: The Dilution Trap of the NASA ETF

Author: DeepTide TechFlow

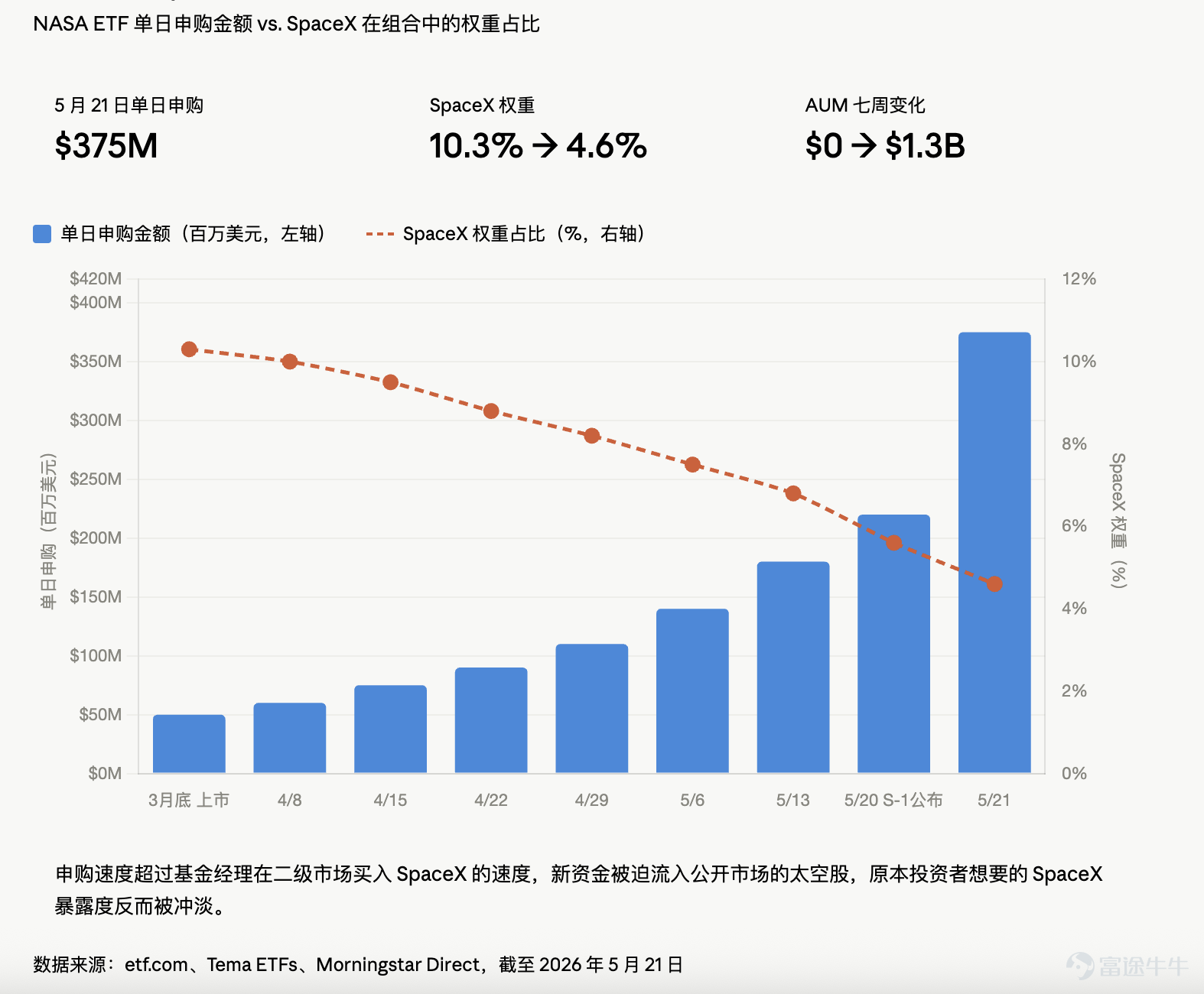

On May 20, SpaceX’s S-1 registration statement appeared on the SEC’s website. The next day, a fund with the ticker symbol 'NASA' attracted $375 million in a single day, tripling its assets under management (AUM) within a week. This fund had only been launched seven weeks earlier.

Seven weeks later, it has become the world’s largest space-themed ETF, leaving the seven-year-old UFO ETF far behind. The amount it raised in seven weeks exceeds the total raised by UFO over seven years combined.

Everyone rushing into NASA really wants to buy SpaceX—but the actual amount of SpaceX they end up holding keeps shrinking.

NASA ETF markets itself as 'the only pure-play space ETF in the entire market that holds SpaceX.' As of May 21, NASA indirectly held the equivalent of 232,000 shares of SpaceX common stock through a special-purpose vehicle (SPV), with a book value of $147.4 million, implying a valuation of approximately $1.51 trillion.

The numbers look solid at first glance. But there’s a detail ordinary investors simply won’t notice: according to ETF.com, just one week ago, NASA’s position in SpaceX accounted for 10.3% of the fund; a week later, it had been diluted to 4.6%.

Because new subscription capital flooded in too quickly, fund managers couldn’t acquire enough SpaceX shares in the secondary market fast enough. The influx of fresh capital was forced into publicly traded space stocks instead, diluting the very SpaceX exposure investors originally sought.

Retail investors rush in hoping to buy SpaceX, but what they actually get is Rocket Lab plus AST SpaceMobile plus a bunch of other holdings.

Even more subtly, the valuation mechanism is problematic: the SPV’s holdings are only updated when Tema itself executes trades. In other words, no matter how much SpaceX’s secondary market price fluctuates, the book value of NASA’s stake remains frozen.

This setup goes unnoticed in a bull market. But if SpaceX’s stock falls below its IPO price after listing, the SPV position will react with an almost eerie delay. And don’t forget—the SPV is locked up for six months after SpaceX’s official IPO. If the stock crashes on day one, retail investors can exit, but the SPV cannot.

The ETF charges an annual management fee of 0.87%, yet roughly 65% of its headline return has actually come from names like Rocket Lab and Intuitive Machines—stocks that have already surged wildly. SpaceX itself? It hasn’t contributed much at all.

In essence, NASA today is a thematic fund using SpaceX as bait while holding a basket of small-cap space stocks. The bait’s scent matters—but what’s served on the plate is a different fish altogether.

What many people don’t realize is that some of the key players in this sector have already gone through a significant rally.

Rocket Lab has risen 357% over the past 12 months; Planet Labs surged 979%; LUNR climbed 212%. ARKX gained 62% over the past year, while ROKT rose 75%. SpaceX merely lit a match to dry tinder that was already smoldering.

When you lay out these numbers, questions arise. Planet Labs’ stock has jumped 979% in a year, yet its core business is selling satellite imagery data. Does its fundamentals justify a near tenfold surge in share price?

There were 102 orbital launches globally in 2019, and 342 in 2025—double the number during the peak of the space race in 1967. Grand View Research forecasts the global space industry’s market size at $466 billion in 2024, growing to $769 billion by 2030.

But here’s the problem: even if the industry grows from $466 billion to $769 billion, why should that translate into a tenfold gain in secondary market valuations?

This is a classic case of valuation inversion. Fundamentals are growing linearly, while stock prices are rising exponentially—the gap filled by a 'narrative premium.' And there’s only one source for that narrative premium: SpaceX’s impending IPO.

So what exactly are the ultimate buyers getting?

Let’s return to SpaceX itself.

Revenue reached $18.67 billion in 2024, up from just $10.3 billion in 2023. However, the company reported a loss of $4.59 billion in 2024, compared to a profit of $791 million in 2023—swinging directly from profit to loss.

According to CNN’s report, the company lost nearly $5 billion last year, primarily due to its AI division burning cash to build data centers.

SpaceX disclosed in its prospectus that xAI has already been folded into SpaceX, and X (formerly Twitter) is included as well. This so-called 'space IPO' is essentially a bundled offering of nearly all of Elon Musk’s assets. The prospectus also revealed that Musk controls 85% of the voting power—unless he votes himself out, no one else can remove him.

The $1.75 trillion valuation for SpaceX corresponds to a combined narrative of 'space + AI + satellite internet + social media.' The grander the narrative, the more inflated the price.

But the secondary market doesn’t care about that. What matters to the secondary market is that everyone is rushing to get in—and so I have to get in too.

After all this maneuvering, the biggest winners aren’t SpaceX’s retail shareholders—they haven’t even gotten on board yet—nor are they ETF investors who rushed into NASA-themed funds, since their exposure to SpaceX is being diluted.

The real winners are the ETF issuers. NASA’s expense ratio is 0.87%, the third-highest among similar funds. With $13 billion in assets under management (AUM), that translates to $11 million in annual management fee revenue.

Launching an ETF is fundamentally no different from issuing a token—you need a story, timing, and a seemingly credible benchmark. SpaceX provided all three.

On June 12, SpaceX is expected to list on Nasdaq under the ticker SPCX. The underwriting syndicate is led by several of the world’s largest investment banks, with a fundraising target of $40–80 billion—far surpassing the record set by Saudi Aramco in 2020.

This will be the largest IPO in human history.

If the stock drops below its IPO price on day one, all ETF investors who bought in based on the SpaceX narrative will find that their SPV positions are still marked at the 'stale' price from months ago—they won’t be able to cut losses or exit immediately.

If the ETF surges at the open, those who missed buying it will rush in, pushing its premium even higher and further diluting SpaceX’s actual weight within the ETF—creating a comical reverse flywheel effect: the more people buy in, the smaller each investor’s effective stake in SpaceX becomes.

After SpaceX, a lineup of industry giants is waiting to go public. Each new 'flagship stock' from a hyped sector will spawn a batch of new ETFs—and each new batch of ETFs will replay the same dilution game.

The market isn’t short on new stories—it’s short on people asking, 'Did I really buy what I thought I was buying?' There will be an answer after June 12. But by then, those rushing into NASA today won’t care anymore—they’ll either be counting profits or filing complaints.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

14

8