Micron delivers a stellar earnings report! Will the memory sector keep rising?

TensThink | A thirty-fold surge in a year—what’s behind this storage giant SanDisk's phenomenal rise?!

Over the past year, $SanDisk (SNDK.US)$ the stock price of SanDisk has experienced a remarkable and powerful upward climb. This was not due to a single accidental catalyst but rather the inevitable result of multiple forces overlapping over time. From the underlying logic of the industry cycle to the strong injection of artificial intelligence demand, from the company’s own strategic restructuring to the warming risk appetite of global capital, every dimension has contributed to fueling this dramatic stock price surge.

The industry cycle provided the fundamental profit elasticity, while the spin-off independence triggered a revaluation window for valuation recovery. The AI narrative opened up the ceiling for mid- to long-term growth imagination, and ample liquidity in the capital markets acted as an accelerant.These four main logical threads are intertwined and build upon one another, together forming a complete and coherent upward narrative.

Looking ahead, as long as NAND prices remain resilient, AI demand continues to grow, and the company’s strategic execution stays stable, SanDisk’s stock will still have a solid foundation to maintain its strength. Conversely, if any of these logical factors weaken, the market's tolerance for its high valuation may also decline.

The dynamics of change and continuity within these factors represent the core proposition most worthy of ongoing tracking for anyone investing in SanDisk.

Industry Cycle Turning Point: Storage Market Transitioning from a Deep Freeze to Recovery

The NAND flash memory industry where SanDisk operates has always been known for its pronounced cyclical fluctuations. After enduring a prolonged downturn from 2022 to 2023 marked by weak demand, high inventory, and plummeting prices, the entire industry witnessed a fundamental reversal in supply-demand dynamics in the second half of 2024.

The contraction on the supply side was the starting point of this cycle — $Samsung Electronics (005930.KR)$ 、 $SK Hynix (000660.KR)$ 、 $Micron Technology (MU.US)$ and $Western Digital (WDC.US)$ Major original equipment manufacturers such as (SanDisk's former parent company) have cut capital expenditures and lowered capacity utilization to unprecedented levels, resulting in a prolonged period of reduced supply of NAND wafers.

At the same time, demand recovery, though slow, is steady: end markets such as smartphones and PCs are beginning to enter a restocking phase after two years of inventory reduction. Meanwhile, the demand for storage capacity driven by AI edge inference is quietly rising. The balance of supply and demand is starting to shift from a buyer’s market to a seller’s market, triggering an unexpectedly strong upward cycle in NAND prices.

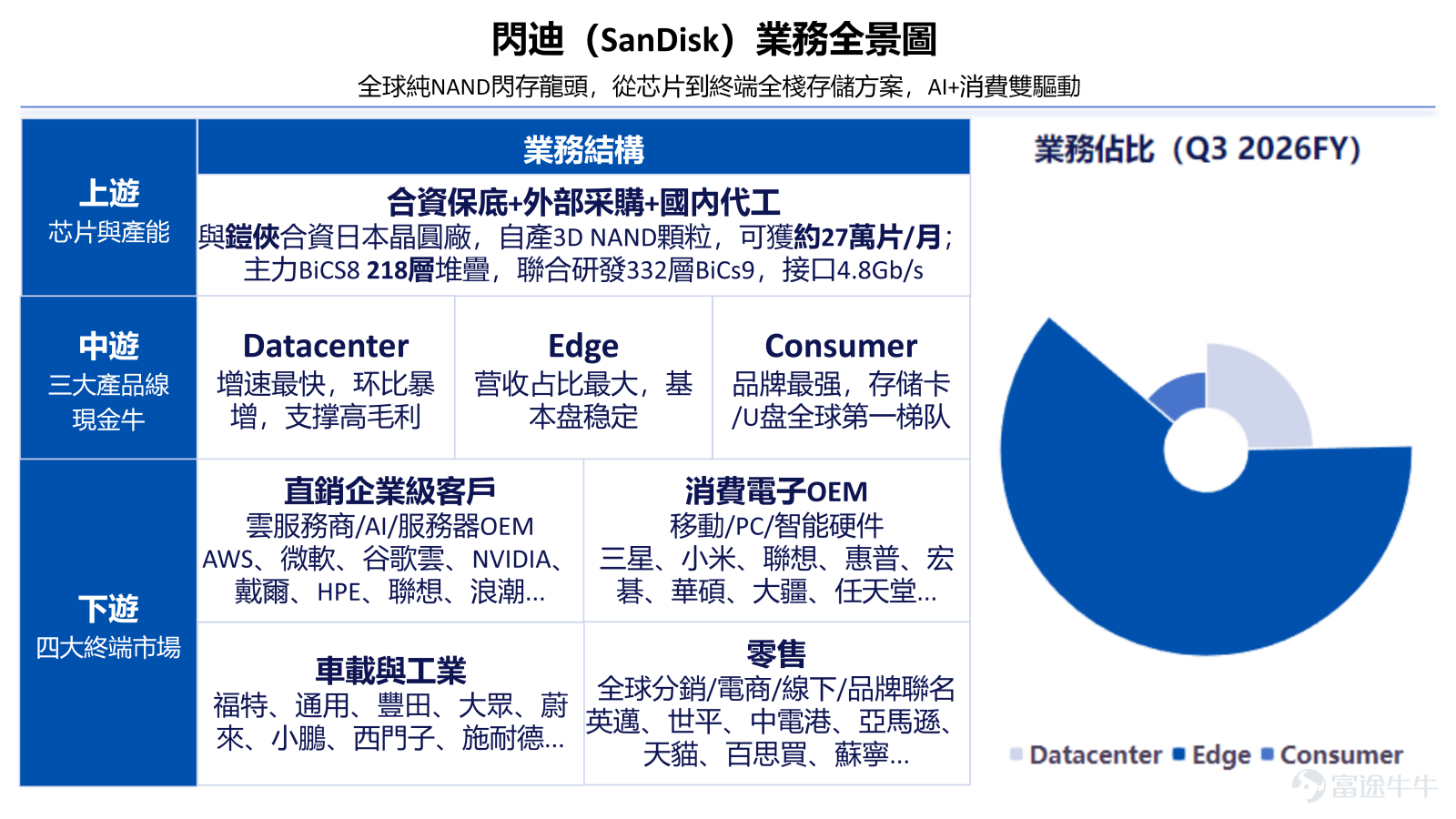

Datacenter One of Sandisk's three major business lines, this refers to the business line that provides high-performance enterprise-level NAND flash memory and solid-state drive (SSD) solutions for hyperscale cloud providers, enterprise data centers, and AI computing clusters. It is a core enabler for AI training/inference, cloud computing, and data center storage infrastructure scenarios.

SanDisk's Q3 of fiscal year 2026: Real-time Q1 of 2026, same below

Edge refers to the business line targeting enterprise and smart endpoint scenarios outside traditional data centers, offering industrial-grade, automotive-grade, and embedded NAND flash memory and storage solutions. It emphasizes high reliability, wide temperature tolerance, long lifespan, compact size, and low power consumption.

Consumer primarily targets individual end users and consumer electronics scenarios such as digital devices, photography, and everyday portable storage. It provides standardized civilian-grade flash memory products, emphasizing plug-and-play functionality, portability, and cost-effectiveness.

As a globally significant NAND flash memory supplier, its profitabilityis highly positively correlated with NAND prices. When industry prices experience cyclical increases, the company’s gross margin and operating margin significantly recover, forming the most fundamental earnings support for stock price growth.

For a technology company with storage chips as its core asset, a turning point in the industry cycle is the most decisive macro force. Like a hurricane filling sails, it quickly lifts SanDisk's share price from its lows.

Spin-off Independence: A Value Reassessment from 'Empire Dependency' to 'Self-Determination'

If the recovery of the industry cycle serves as the"favorable timing"for SanDisk’s rising stock price, then the formal spin-off from Western Digital represents the"harmonious human factors"in this market movement. In February 2025, Western Digital officially completed the split of its two major businesses—HDD and NAND—with SanDisk re-entering the capital market as an independent entity.

The strategic significance of this spin-off should not be underestimated. During the merger period, SanDisk's value was long overshadowed by Western Digital’s overall structure, making it difficult for the market to assign a clear valuation. Management's attention was also divided between two vastly different product lines, resulting in suboptimal capital allocation and R&D investments.

After becoming independent, SanDisk has been given a fresh strategic canvas. Management can now focus on the NAND and SSD sectors, formulating more targeted investment strategies while gaining an independent equity structure and capital operation tools. For investors who have long been focused on the storage sector, this kind of “reaffirmation”-style spin-off is akin to a triggering event for value discovery.

The market is reassessing SanDisk’s asset quality, technological reserves, and growth prospects, granting it a valuation premium closer to industry leaders. This is directly reflected financially by an upward shift in the P/E ratio center—even if profit forecasts remain unchanged, the rise in valuation multiples alone is enough to drive significant stock price increases.

AI Narrative Infusion: Transition from Traditional Storage to Computational Storage

In the grand narrative of artificial intelligence infrastructure construction, GPUs and HBM (High Bandwidth Memory) have captured most of the spotlight, but the role of the storage layer, especially SSDs, is gradually being repriced by the market. AI training clusters require massive data throughput capabilities, and the demand for low latency, high-capacity storage during the large model inference phase is equally rigid—whether it’s rapid checkpoint writing or instant loading of model weights, high-performance NVMe SSD support is essential.

SanDisk is no mere spectator in this field. The company boasts deep technical expertise in the enterprise SSD market, particularly with forward-looking deployments in technology roadmaps such as Zoned Namespaces (ZNS), enabling superior storage efficiency and lower total cost of ownership in data center scenarios.

As the explosive growth in AI inference needs takes hold, this logic is starting to gain acceptance among more investors. SanDisk is no longer viewed merely as a manufacturer of consumer memory cards but is instead being redefined as a foundational participant in AI infrastructure.This cognitive shift has given stocks a higher growth outlook, thereby attracting growth-oriented investors and further raising the valuation benchmark of the stock price.

Support from the capital side: Resonance between the global liquidity environment and technical patterns

Lastly, the supportive external capital environment cannot be ignored. After an aggressive interest rate hike cycle, the Federal Reserve entered a rate-cutting phase in the second half of 2025, which led to a recovery in risk appetite across global capital markets. Technology stocks, as high-beta assets, were among the first to benefit from capital inflows. Sandisk, with its dual attributes of"Cyclical recovery"and"AI growth narrative", naturally became one of the preferred directions for institutional capital allocation in an environment where funds were seeking high-elasticity targets.

From a technical perspective, the trading volume of Sandisk's shares was relatively limited after its IPO, and most of the equity was held long-term by institutional investors, meaning there wasn’t much freely tradable floating stock available in the market. The combination of abundant capital and a relatively concentrated shareholding structure caused the stock price to exhibit clear signs of"low volume but high price gains", also known as the"empty rise effect."Once this technical pattern forms, it will in turn attract trend traders and quantitative funds to chase the uptrend, creating a positive feedback loop that accelerates the upward slope of the stock price.

However, over the past year, Western Digital'sinstitutional ownership ratiohas been gradually decreasing. Despitecontinuous purchases by small and medium shareholders,which has provided relatively stable conditions for the rise of Western Digital’s stock price, the current share price has already exceeded Morningstar’s USD 1,000fair value, investors still need to be mindful of the risks behind the stock price bubble.

In conclusion

Western Digital's moat is composed of a joint venture with Kioxia locking in 50% of advanced 3D NAND capacity + proprietary BiCS architecture and HBF technology + $42 billion in LTAs binding top cloud vendors + holding the No. 1 global market share in consumer segments, forming a“Capacity - Technology - Customers - Brand”Closed loop, gross margin for Q3 of fiscal year 2026 is 78.4%, year-over-year + 247.62%, with precise positioning in the AI inference and automotive memory sectors, which will be difficult to replicate in the short term. However, its share in high-end enterprise SSDs is only 2%-3%(J.P.Morgan, 2025.12), facing long-term pressure from IDM giants like Samsung and Yangtze Memory Technologies.

The reality is that due to the demand for AI training, the mainstream market has gradually shifted from high-performance SSDs to large-capacity, low-cost SSDs. SanDisk's QLC high-capacity technologyhas gone from being non-mainstream to becoming a highly sought-after commodity。

This means that SanDisk can not only navigate through the storage cycle, maintain ultra-high gross margins, consolidate its industry position, and benefit from AI and automotive memory growth, but also faces an upper limit to its development due to its reliance on Kioxia and weaker high-end technical ecosystem, making it difficult to break into the top tier of global premium storage. The market’s investment thesis on it will gradually shift from a cyclical storage stock to a growth + cash blue-chip stock.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

17

16