Dividend Season Guide: May brings a wave of dividends, with the highest payout reaching 1,638 Hong K

Guozheng International Research Report: Binhai Investment Target Price at HKD 1.43, Maintain 'Buy' Rating

$BINHAI INV (02886.HK)$ Binhai Investment Target Price at HKD 1.43, Maintain 'Buy' Rating

Q1 gas sales increased significantly year-over-year, attractive dividend yield

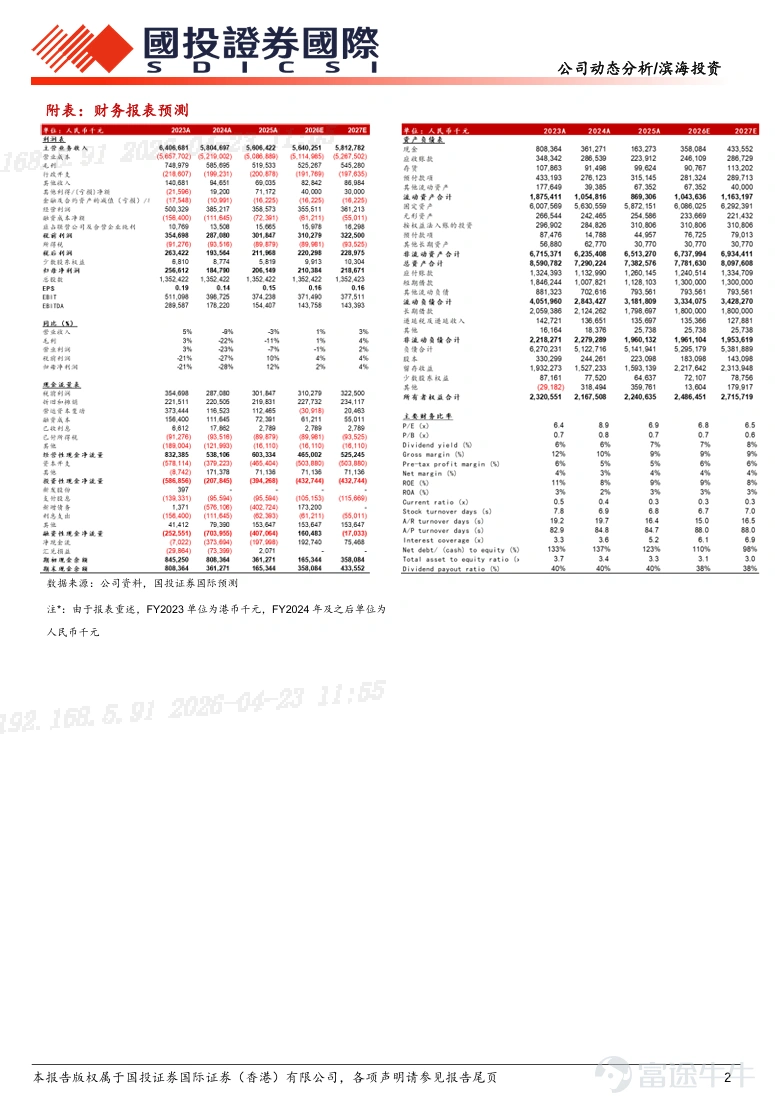

Event: The company announced its Q1 2026 operating results. The company's pipeline gas sales volume reached 794 million cubic meters in Q1, yoy+21%; including 585 million cubic meters of piped gas, yoy+23%. Previously, the company disclosed its full-year 2025 performance, reporting revenue of RMB 5.606 billion, down 3% year-on-year; net profit attributable to shareholders was RMB 206 million, up 12% year-on-year. The company has achieved remarkable cost reductions and efficiency improvements, with an attractive dividend yield of 6.9%. Considering peer valuations and industry trends, we assign the company a forecasted P/E ratio of 8x for 2026 (exchange rate assumption: 1 RMB = 1.15 HKD), corresponding to a target price of HKD 1.43, maintaining a 'Buy' rating.

Report Summary

Q1 gas sales achieve relatively good year-on-year growth

The company’s pipeline gas sales volume reached 794 million cubic meters in Q1, yoy+21%; including 585 million cubic meters of piped gas, yoy+23%, comprising 439 million cubic meters sold to industrial and commercial users, yoy+31%, and 146 million cubic meters for residential use, yoy+4%; pipeline transport volume was 209 million cubic meters, yoy+15%. Earlier, the company announced its 2025 annual results, reporting gas sales revenue of RMB 5.25 billion (yoy-2%); gross profit of RMB 310 million (yoy-1%). Despite a weak broader market, it still demonstrated resilient performance. Gas connection revenue was RMB 220 million (yoy-26%); gross profit was RMB 120 million (yoy-34%), mainly impacted by the real estate sector. Natural gas pipeline business revenue was RMB 52 million (yoy-17%); gross profit was RMB 44 million (yoy-18%). Value-added services saw rapid growth, generating revenue of RMB 76 million (yoy+14%); gross profit was RMB 50 million (yoy+13%). The company forecasts total gas sales volume of 2.5 billion cubic meters in 2026, including 1.9 billion cubic meters of pipeline gas sales (yoy+6%) and 600 million cubic meters of pipeline transport volume (yoy-7%); urban gas gross margin at 0.51 yuan, with 43,000 new connections, and value-added service gross profit increasing by 15%.

Significant achievements in cost reduction and efficiency enhancement

Two major shareholders firmly support the company's development

In 2025, the company’s financing costs were RMB 75.2 million, down 41% year-on-year; the average annual loan interest rate was 4.4%, down 90 basis points compared to the same period last year. The company continues to optimize its debt structure, proactively repaying high-interest debt; it is also expanding its financing channels, successfully implementing innovative financing products from multiple large financial institutions. The company expects further financing cost reductions this year in the range of RMB 10-15 million. The two major shareholders, Tianjin Teda and Sinopec Natural Gas, have signed a 'Framework Agreement on Further Deepening Strategic Cooperation to Support the Company’s Development,' providing multi-faceted support for the company’s business development, including gas sources, end markets, and clean energy projects.

Full-year dividend payout ratio at 51%, with an attractive dividend yield

The company declared a final dividend of 8.36 Hong Kong cents per share, an increase of 0.76 Hong Kong cents over last year, with a full-year dividend payout ratio reaching 51%. The company announced a three-year dividend payout guidance: based on the 2024 dividend per share of HKD 0.076, it plans to increase the dividend per share by no less than 10% annually for 2025-2027. Currently, the company’s dividend yield is around 6.9%, which is quite attractive.

Target price HKD 1.43, maintain 'Buy' rating

The group is exploring a favorable implementation path for developing new energy businesses under the 'Dual Carbon' policy, thereby accelerating its transformation into a comprehensive energy supplier.

We assume a slight increase in gas sales volume, a modest rise in gross margin, and a small decline in newly connected households. Considering peer valuations and industry trends, we assign the company a forecast P/E ratio of 8x for 2026 (exchange rate assumption: 1 RMB = 1.15 HKD), corresponding to a target price of 1.43 Hong Kong dollars. We maintain a 'Buy' rating.

Risk warnings: Demand below expectations, significant cost increases, and continued downturn in the real estate sector.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1