Dividend Season Guide: May brings a wave of dividends, with the highest payout reaching 1,638 Hong K

“HALO” assets are gaining popularity, but is the underlying reason actually a dividend strategy?

I.HALO trading heats up: As the market begins to search for assets with “Lower substitutabilityassets”

Recently, “HALO” trading has gained momentum, drawing widespread attention in the market.

HALO does not refer to an industry portfolio, but rather a type of asset characteristic: Heavy Assets, Low Obsolescence—meaning assets that are capital-intensive and have low rates of obsolescence. Simply put, these are assets that are difficult for AI to quickly replace and require significant capital investment.

The rise of this concept is closely related to changes in the current market environment. In recent years, the rapid development of AI technology has driven the tech sector to become the core focus of the market. However, as AI continues to evolve, market perceptions of AI have started to shift from optimistic expectations to a more rational review.

On one hand, tech giants continue to make large-scale capital expenditures in the AI field, which puts pressure on corporate cash flows; on the other hand, the “creative destruction” effect brought by AI has also begun to capture market attention. On March 6, US non-farm data significantly underperformed expectations, with the February non-farm employment population decreasing by 92,000, far below market expectations of a 59,000 increase. Additionally, some light-asset industries that are more susceptible to AI replacement shocks have seen noticeable adjustments. For instance, the US software sector fell over 30% from its peak, prompting funds to reassess the long-term competitiveness of different assets.

At the same time, the macro environment is also changing. The past environment of low interest rates and loose liquidity allowed growth assets to enjoy a valuation premium over the long term. However, at the current stage, with escalating conflicts involving the US and Iran, increased geopolitical disruptions, stronger trends towards regionalized supply chains, and rising capital costs, the market’s focus on physical production capacity and resource security has significantly increased. Against this backdrop, industries supported by tangible assets are regaining attention. Sectors such as energy, resources, infrastructure, transportation, and utilities often have long construction cycles, high replication costs, and long asset lifespans, and their value is being repriced in the new macro environment.

Recent trend comparison between the software sector and the energy sector

II.HALO assets actually overlap significantly with dividend-paying assets.

If we further break down the characteristics of HALO assets, we find that they often possess another important feature — relatively stable cash flows and strong dividend-paying ability.

Capital-intensive industries typically require long-term capital investment and have high barriers to entry. Once these assets are built and enter a stable operational phase, their profit models tend to be mature and their cash flow relatively stable. This allows many companies to maintain consistent dividend payouts. For example, sectors like energy, electricity, transportation, and utilities not only have high asset intensity but are also traditionally high-dividend sectors. Therefore, in the capital markets, these industries represent typical HALO assets and are important sources of dividend-paying assets.

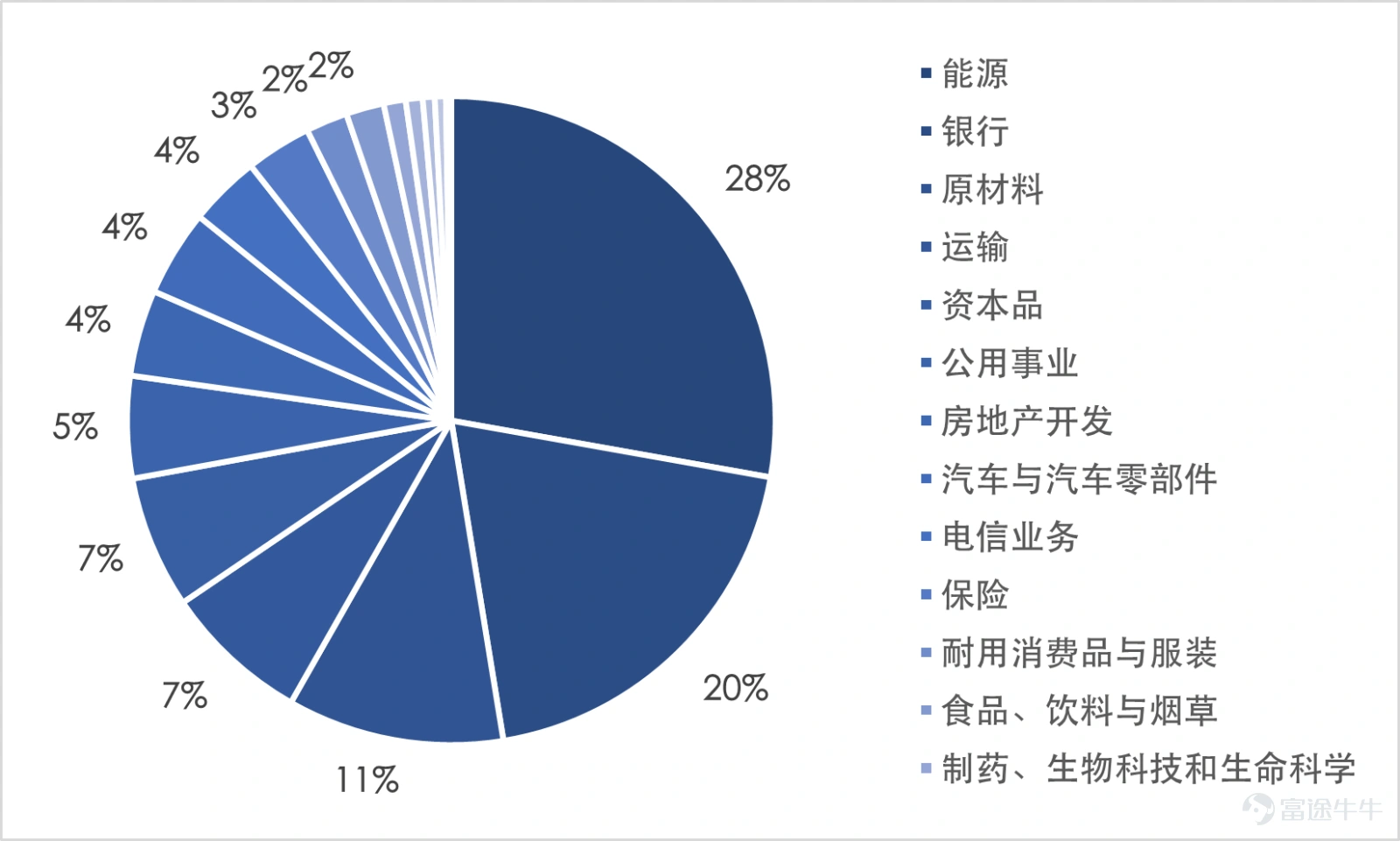

Taking the MSCI Asia Pacific Select High Dividend Index as an example, its top five weighted industry groups are: energy, banking, materials, transportation, and capital goods. Among them, except for banking, the other four major weighted industries are typical HALO assets, collectively accounting for nearly 55% of the index. For funds seeking stable returns, these assets offer both tangible asset backing and potential ongoing cash returns.

MSCI Asia Pacific Select High Dividend Index Industry Distribution

Data source: Bloomberg, according to GICS industry group distribution, as of March 12, 2026.

Meanwhile, the MSCI Asia Pacific Select High Dividend Index is not limited to a single market; it includes representative HALO assets from multiple mature markets across the Asia-Pacific region within one portfolio. From the perspective of industry distribution, different markets show strengths in capital-intensive sectors, creating clear structural division of labor.

MSCI Asia Pacific High Dividend Index Regional and Sectoral Distribution

Data source: Bloomberg, according to GICS industry distribution, as of March 12, 2026.

In the Australian market, index components are mainly concentrated in the energy and resources sectors. As a globally important resource exporter, Australia is home to numerous mining and energy companies. These firms typically possess long-cycle, capital-intensive physical assets and benefit from changes in global commodity demand and resource supply dynamics. Under the HALO framework, these resource-based enterprises not only exhibit heavy-asset characteristics but also often demonstrate strong cash flow generation capabilities, making them typical representatives of 'hard assets.' $BHP Group Ltd (BHP.US)$

In the Hong Kong market, weighting is more concentrated in the financial and energy sectors. The Hong Kong market hosts a large number of regional banks and major financial institutions with mature business models, relatively stable profitability, and high dividend levels. Additionally, telecommunications, energy, and some utility companies occupy significant positions in the index, providing relatively stable cash flow sources for portfolios. $PETROCHINA (00857.HK)$$CHINA SHENHUA (01088.HK)$$ICBC (01398.HK)$$ABC (01288.HK)$$CCB (00939.HK)$

In the Japanese market, the industrial structure presents more diversified characteristics. Japanese companies have long-standing accumulations in industries such as industrials, consumer goods, and finance. Many firms possess well-established manufacturing systems and infrastructure assets. Furthermore, driven by corporate governance reforms, dividend payouts and shareholder return levels have continuously improved in recent years. Consequently, the Japanese market forms an index structure characterized by industrials and consumer goods, supplemented by finance. $SoftBank (9434.JP)$

From an overall structural perspective, energy, finance, and materials are the core industries with higher representation in the index. These industries are precisely typical heavy-asset sectors with long asset lifespans, stable industry structures, and robust dividend-paying capabilities.

More importantly, differences in industrial structure across markets result in varying performance of these HALO assets during economic cycles. For instance, resource-based economies are more likely to benefit from commodity cycles, while financial and industrial sectors are more closely tied to regional economic growth rhythms. Cross-market allocation not only consolidates the most representative heavy-asset enterprises in the Asia-Pacific region but also helps mitigate single-market volatility to a certain extent.

As a result, the risk-return efficiency of the MSCI Asia Pacific Select High Dividend Index significantly outperforms similar indices. Over the past year, the index's volatility was only 7.96%, markedly lower than other Asia-Pacific high-dividend indices in the Hong Kong market. Extending the timeframe to three and five years, the index's volatility remains consistently lower, reflecting superior risk-return characteristics.

Comparison with similar indices

Data source: Bloomberg, Wind, as of February 27, 2026.

According to the current index compilation rules, applying the weight composition of constituent stocks retroactively to historical dates calculates the simulated historical performance. The above only objectively displays the historical performance of the benchmark index; past performance of the index does not predict future results and should not be considered investment advice. Investors should be aware of the risks associated with index volatility. Actual fund returns may differ from index performance due to management fees and tracking errors, which investors should note.

Therefore, from the perspective of asset characteristics, the MSCI Asia Pacific Select High Dividend Index can be understood as a HALO asset portfolio with broader regional exposure: focusing on core industries with heavy assets and low obsolescence rates, while enhancing the stability and comparative advantages of the portfolio through multi-market allocation across the Asia-Pacific region.

As the market begins to reassess assets using the concept of HALO, the MSCI Asia Pacific Select High Dividend Index may provide a more intuitive answer — consolidating the most representative HALO assets in the Asia-Pacific region into a single basket. Follow for more insights.E Fund (Hong Kong) MSCI Asia Pacific Select High Dividend Index ETF (3483) $E FUND (HK) MSCI Asia Pacific Select High Dividend Index ETF (03483.HK)$ ,Seize the relatively stable investment opportunities presented by HALO assets.

Important Information:

1) E Fund (Hong Kong) MSCI Asia Pacific Select High Dividend Index ETF ('Sub-fund') is a sub-fund under the E Fund ETF Trust, which is an umbrella unit trust established under Hong Kong law. The Sub-fund is categorized as a passively managed ETF under Chapter 8.6 of the Code on Unit Trusts and Mutual Funds issued by the Securities and Futures Commission ('SFC'). Units of the Sub-fund ('Units') are traded on the Stock Exchange of Hong Kong Limited ('HKEX') like stocks. Its investment objective is to provide investment returns that closely track the performance of the MSCI Asia Pacific Select High Dividend Index ('Index') (before deducting fees and expenses).

2) Investment involves risks. This fund is exposed to the following risks: a) investment risk, b) stock market risk, c) new index risk, d) concentration risk, e) risks associated with small- and mid-cap companies, f) risks related to regulations in the Australian and Japanese stock markets, g) concentration in high-dividend stocks and associated risks, h) securities lending transaction risk, i) different trading hours risk, j) passive investment risk, k) trading risk, l) tracking error risk, m) multiple counter risk, n) currency risk, o) risk of distributions being paid out of capital / effectively paid out of capital, P) reliance on market maker risk, Q) termination risk. The value of the Sub-fund can go up or down, and may experience significant declines. Investors may incur losses.

The issuer of this content is E Fund Management (Hong Kong) Co., Ltd. This content does not constitute an invitation or recommendation to invest in fund units. Dividend payouts are not guaranteed and may be distributed from capital. Investment involves risks, and fund prices can go up or down. Before investing, investors should carefully read the fund's prospectus (including the “Risk Factors” section) to understand the investment risks associated with the fund. This content has not been reviewed by the Securities and Futures Commission of Hong Kong. For detailed important notices and disclaimers regarding the above fund, please visit the E Fund Hong Kong website: E Fund (Hong Kong) MSCI Asia Pacific Select High Dividend Index ETF (3483).https://www.efunds.com.hk/tc/products/47/important/

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

3