Negotiations remain deadlocked—will the U.S.-Iran deal materialize on schedule?

Global Weekly Talk | Fed rate cut expectations weighed down by inflation and geopolitical risks, China's economy off to a good start in January-February

On the macroeconomic front

United States: The Federal Reserve kept interest rates unchanged for the second consecutive time, as expectations for rate cuts were dampened by inflation and geopolitical risks.

Last week, the key focus in the U.S. was on the Federal Reserve’s March interest rate meeting, alongside attention to adjustments in inflation and economic forecasts, as well as Powell's potential departure or retention. The Fed announced that it would maintain the target range for the federal funds rate at 3.5%-3.75%, marking the second consecutive hold this year. Among the 12 FOMC members, 11 supported the decision, while only one member advocated for a 25-basis-point rate cut.Members who previously opposed pausing rate cuts have shifted to supporting the status quo. The meeting emphasized the uncertain impact of geopolitical conflicts in the Middle East.The transmission of high oil prices to inflation needs to be continuously monitored. Meanwhile, the forecast for PCE inflation in 2026 was revised up to 2.7%, with a slight upward revision to GDP growth to 2.4%. The unemployment rate projection remained unchanged at 4.4%.The dot plot shows that officials’ divergence has converged towards fewer rate cuts, with the median projection expecting one rate cut this year.Market expectations for rate cuts have receded. Additionally, Powell clearly stated that he does not intend to leave the Federal Reserve Board before the completion of an ongoing investigation. If the nomination for a new chair is not confirmed in time, he will serve as the interim chair, though his role in providing personal policy guidance has diminished.

China: The national economy showed a good start from January to February, with consumption, industry, and investment exhibiting structural characteristics.

Last week, domestic data for January-February on the national economy was released, showing a strong start overall with steady improvement.On the consumption front, total retail sales increased by 2.8% year-on-year, strongly supported by online consumption. Growth in catering consumption rebounded, and discretionary consumption continued to recover. However, auto-related consumption declined significantly. Excluding autos and petroleum, core retail sales growth reached 8.9%. In terms of industry, value-added industrial output for enterprises above designated size grew by 6.3% year-on-year, with private enterprises leading the growth.High-end manufacturing industries such as computer communications, railways, shipping, and aviation have shown notable growth rates, while energy production has remained stable.Crude oil production turned from a decline to an increase, and the growth rate of electricity production accelerated. In terms of investment, national fixed asset investment increased by 1.8% year-on-year, infrastructure investment grew by 11.4%, industrial investment rose by 5.4%, but private investment declined year-on-year. The drop in real estate development investment narrowed, but sales and new construction starts continued to fall.In terms of employment, the average urban surveyed unemployment rate for January-February was 5.3%, unchanged from the same period last year.The youth unemployment rate for ages 16-24 fell for six consecutive months, and overall employment remained stable.

In terms of the equity market

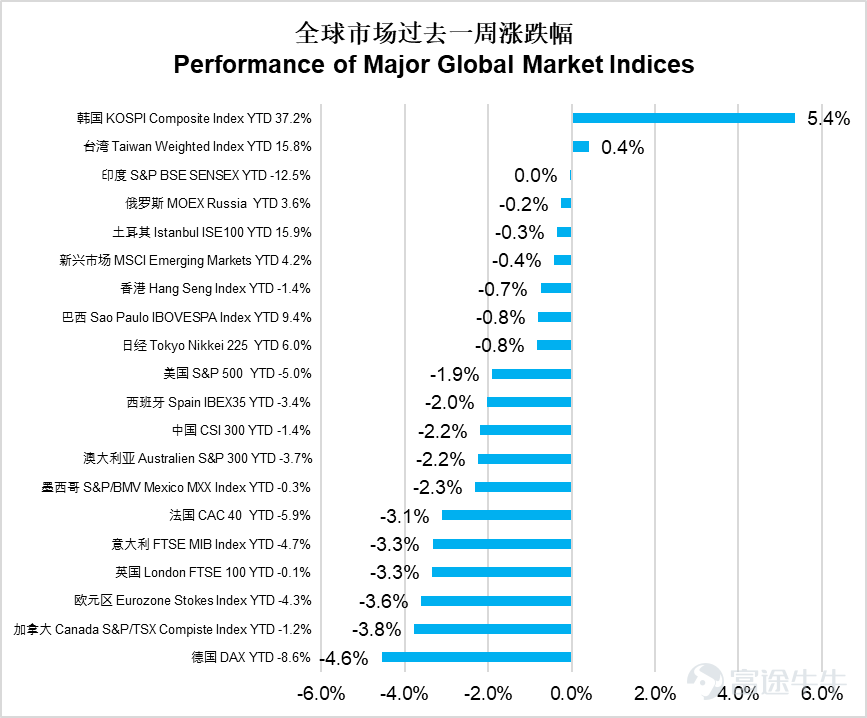

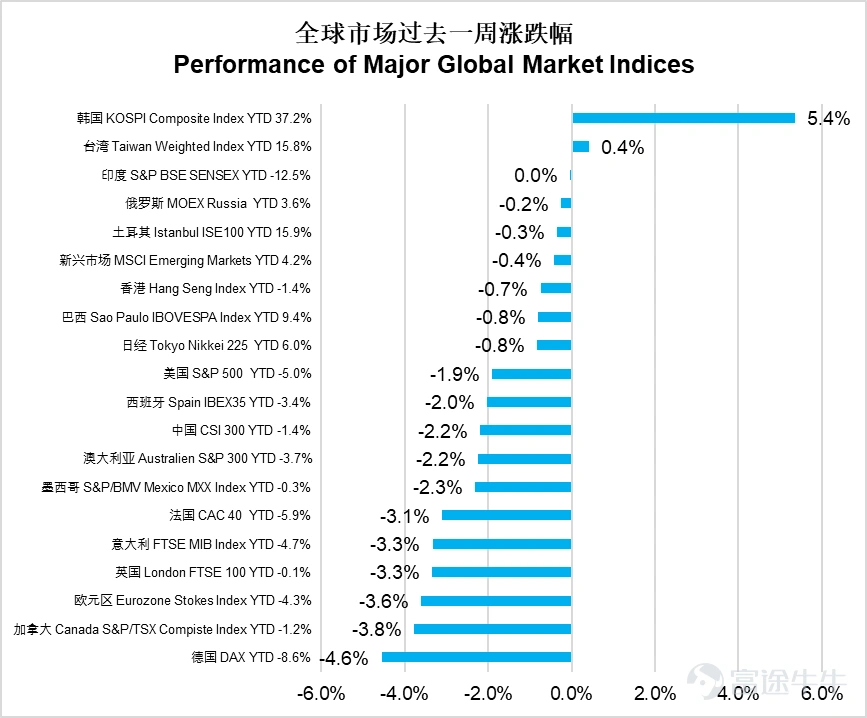

Last week, global markets generally fell, with European markets leading the declines. Germany's DAX index plummeted by 4.6%, Canada’s S&P/TSX dropped by 3.8%,and the Eurozone's STOXX fell by 3.6%. Emerging markets overall declined by 0.4%, a relatively moderate drop. South Korea’s KOSPI surged by 5.4%, standing out as the top performer; Taiwan’s weighted index edged up by 0.4%, and India’s Sensex remained flat. The U.S. S&P 500 fell by 1.9%, Hong Kong’s Hang Seng Index dropped by 0.7%, and China’s CSI 300 fell by 2.2%.Overall, Asian markets outperformed those in Europe and America.

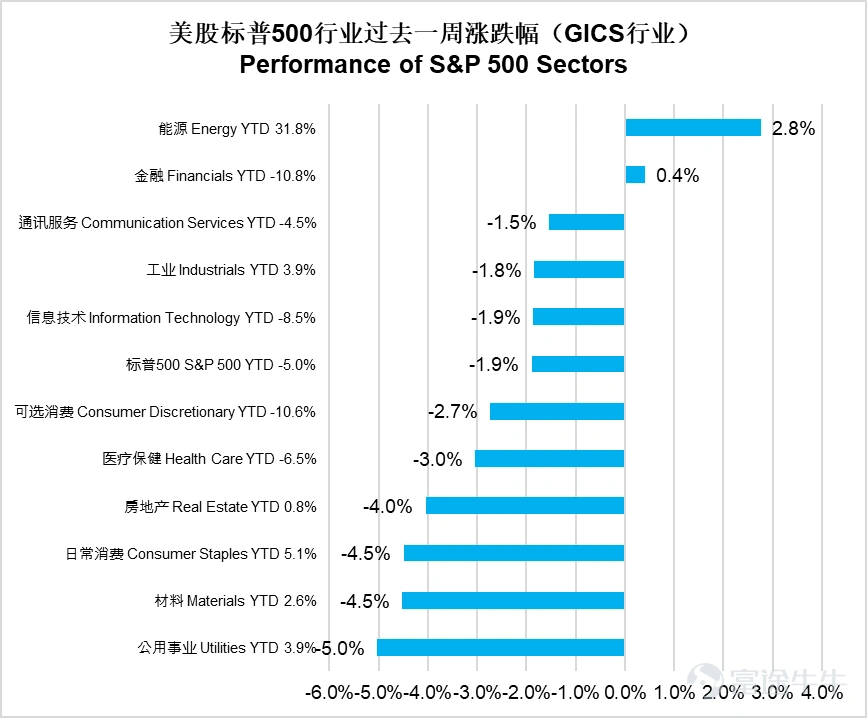

The U.S. energy sector performed best, rising against the trend by 2.8%, while the financial sector increased by 0.4%, becoming one of the few sectors to rise.However, the utilities sector plunged by 5.0%, materials and consumer staples both fell by 4.5%, real estate declined by 4.0%, healthcare dropped by 3.0%, and discretionary consumption fell by 2.7%. Information technology moved in line with the broader market (-1.9%), industrials fell by 1.8%,and communication services dropped by 1.5%. The market showed a pattern of energy and finance sectors rising alone, while defensive sectors led the declines.

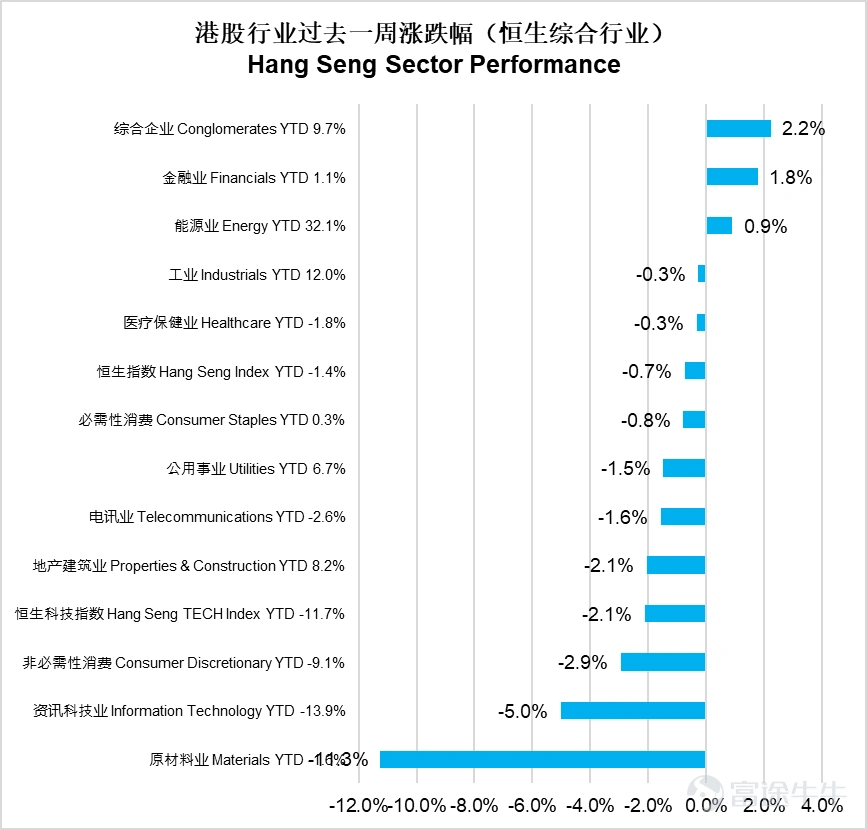

Hong Kong-listed diversified enterprises performed best, rising by 2.2%; the financial sector climbed by 1.8%, and the energy sector rose by 0.9%.However, the raw materials sector plummeted 11.3%, leading the declines, followed by a 5.0% drop in the information technology sector and a 2.9% decline in non-essential consumption. Both the real estate construction industry and the Hang Seng Tech Index fell by 2.1%, while the telecommunications sector dropped 1.6%. Utilities declined by 1.5%, and essential consumption fell by 0.8%.Healthcare and industrials each edged down by 0.3%. The market exhibited an extreme divergence, characterized by financials and energy sectors leading gains, while raw materials and technology sectors led losses.

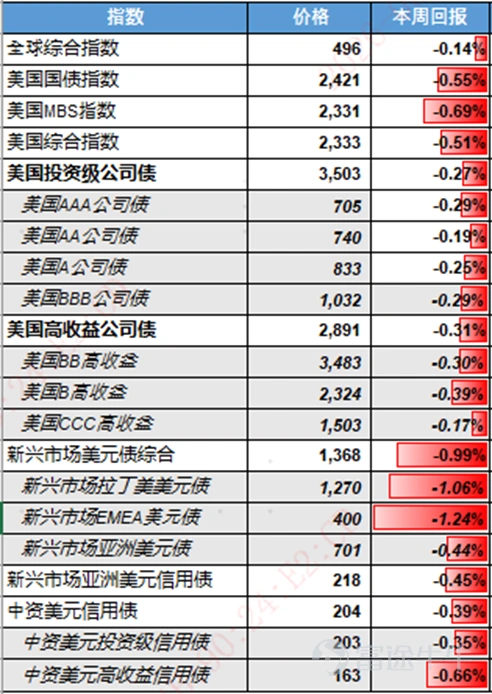

In the bond market,

Global bond markets continued to retreat overall over the past week.The global composite index fell by 0.14%, the U.S. composite index dropped by 0.51%, U.S. investment-grade corporate bonds fell by 0.27%, and U.S. high-yield corporate bonds declined by 0.31%. The emerging market USD bond composite index decreased by 0.99%.The Chinese USD credit bond index fell by 0.39%.

In terms of interest rates, U.S. Treasury yields moved higher overall.The 2-year U.S. Treasury yield rose by 18 basis points to 3.90%, while the 10-year U.S. Treasury yield increased by 10 basis points to 4.38%.

Market Outlook

– The market witnessed rising crude oil prices and U.S. Treasury yields, alongside falling gold and equities.

The Middle East geopolitical conflict has entered its fourth week, with the intensity of the conflict escalating this week as Iran and Gulf state energy infrastructures were attacked. Additionally, the Strait of Hormuz remains closed, further driving oil prices higher during the week. As the conflict continues,Market expectations for the Federal Reserve's rate cuts this year have been completely erased, and according to data from betting sites, investors now see a 21% probability of the Fed raising rates this year.The market reacted with crude oil rising, US Treasury yields climbing, gold falling, and stocks declining. Based on the currently available information, the conflict is still heading towards further escalation, with the US further deploying personnel and warships from global military bases to the Middle East.Betting sites have hit a new high, with nearly 70% odds of US ground troops invading Iran.In addition, at this week's FOMC interest rate meeting, Powell publicly stated that he does not rule out continuing as Fed Chair after his term ends in May if the new Fed candidate Kevin Warsh fails to secure parliamentary confirmation, further increasing uncertainty about the direction of policy rates. The S&P 500 has retreated less than 7% from its January peak.Analysts have not revised down their earnings expectations despite the sharp rise in oil prices, so the recent decline has mainly been due to apparent valuation adjustments.However, valuations are still relatively high by historical standards. If the conflict escalates or drags on, analysts are expected to lower their earnings forecasts, which could be accompanied by further market declines.

Key economic data and events this week

On Tuesday, the US will release the preliminary S&P Global Manufacturing PMI for March.

On Friday, the US will release the University of Michigan Consumer Sentiment data for March.

All rights reserved © 2026. E Fund Management (Hong Kong) Co., Limited.The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may go up or down, and past performance is not indicative of future results. Before investing, investors should carefully read the investment risks related to the fund in the fund prospectus (including the 'Risk Factors' section). This report may only be distributed within certain jurisdictions. In any jurisdiction where distribution of such information or making any invitation or recommendation is prohibited, or if distributing this report or making an invitation or recommendation to any person constitutes a violation of the law, this report does not constitute such distribution or invitation or recommendation. This document is exempt from prior review and approval by the Hong Kong Securities and Futures Commission (SFC) and has not been reviewed by the SFC. SFC recognition does not imply a recommendation or endorsement of the scheme, nor does it guarantee the commercial merits or performance of the scheme, nor does it represent that the scheme is suitable for all investors, or endorse its suitability for any individual investor or class of investors.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

2