Earnings reports from Chinese giants raise concerns! Is it a good time to buy on dips?

Earnings Preview: Can Alibaba's growth offset cash pressures amid the food delivery war, Qwen subsidies, and surging chip expenses?

$Alibaba (BABA.US)$$BABA-W (09988.HK)$ Earnings report scheduled for release pre-market on March 19 Eastern Time.

Core Financial Indicators

• Revenue for Alibaba's third quarter of fiscal year 2026 is estimated at RMB 289.73 billion, representing a year-over-year growth of 3.42%;

• Net profit is projected at RMB 24.17 billion, marking a year-over-year decrease of 50.62%.

The reason for the revenue growth being only in the low single-digit percentage range is that Alibaba has divested its low-margin offline retail businesses in China, including Intime Retail and Sun Art Retail, which were not yet excluded from last year’s financial reports during the same period. Although Alibaba did not separately disclose the revenue scale of Intime Retail and Sun Art Retail, referring to previous management statements, the group’s actual overall revenue growth should be in the low double digits.

Four key highlights

1. The main focus in the Chinese e-commerce segment will be on the reduction in losses from food delivery services

Management had already indicated during the previous earnings report that since October, per-order losses in instant delivery have halved, while market estimates suggest that the battle for instant delivery likely cost approximately RMB 36 billion in the previous quarter. Market expectations are that losses for this quarter could be around RMB 20 billion. Reasons for reduced losses include higher average order value, an increase in the proportion of non-food orders, and economies of scale. Fellow investors can observe the indicator of sales expenses.

In the long term, management’s profit expectations for Taobao's instant delivery may not be high. Due to traffic diversion via Taobao's instant delivery, the daily active users (DAU) of the main Taobao app have once again surpassed PDD Holdings. Management may allow instant delivery to maintain a slightly negative or slightly profitable status.

2. Cloud business revenue

In terms of B2B large model applications, according to Frost & Sullivan data, Alibaba's large model held over 30% market share in the enterprise sector in the second half of last year, ranking first in the Chinese market. The previous earnings report indicated that external demand growth for Alibaba Cloud was catching up with internal growth. The previous 30% growth rate was one of the factors supporting Alibaba's valuation. Investors can continue to monitor the demand situation this time.

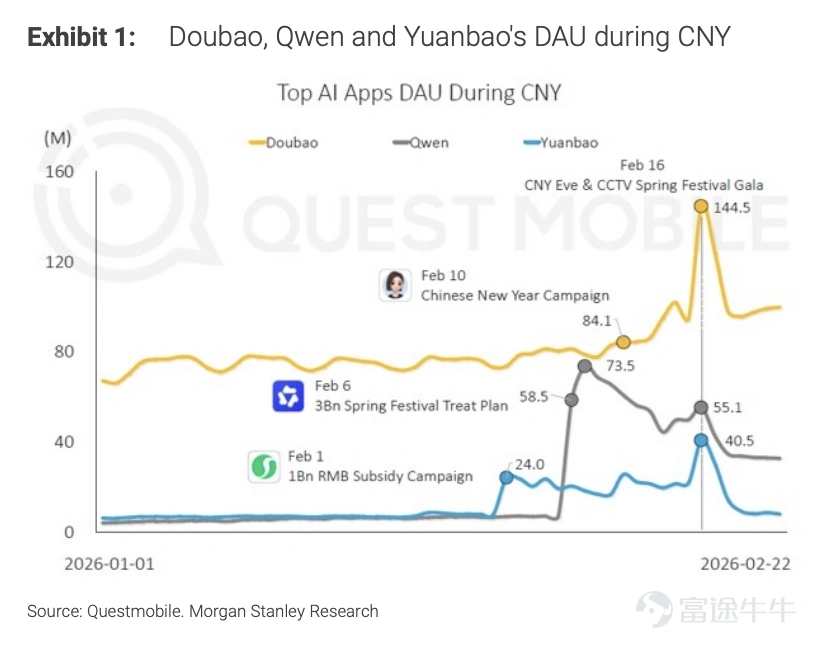

3. Qwen App-related losses

Currently, Alibaba’s consumer-facing AI product, Qwen, has not established a clear differentiated positioning. Following Spring Festival subsidies amounting to billions, its DAU peaked at 55.3 million and quickly dropped back to 40 million, widening the gap compared to ByteDance’s DouBao. Additionally, recent management changes within Qwen have brought uncertainty. The company previously projected that the 'all other' segment, which includes Qwen, would incur a loss of about 10 billion yuan this quarter, reflecting an increase of approximately 6.6 billion yuan in losses from the previous quarter, mostly due to investments in user acquisition for Qwen; other losses include expenses on AI functionalities for AutoNavi Street View and Quark Browser.

Source: Morgan Stanley

4. Will free cash flow continue to deteriorate?

Alibaba has repeatedly provided guidance indicating that its three-year CapEx will reach 380 billion yuan, averaging more than 30 billion yuan per quarter. Apart from CapEx spent on purchasing chips, the ongoing flash sales war continues to erode operating cash flow, significantly reducing the scale used for buybacks in the previous quarter.

Options market signals

Alibaba’s current put/call ratio is 1.42, showing a weakening of bearish momentum compared to the last earnings season. Its implied volatility stands at 46.23%, higher than during the release of the previous financial report.

Summary

– Potential positive factor: Growth in Alibaba Cloud

– Risks to watch: E-commerce competition; increased capital expenditure

– Valuation: Alibaba’s P/E ratio is 18.19x, placing it at the 33rd percentile of its historical range over the past five years.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

7

8