Atour: Retail Surge, Is the Hospitality Industry's 'Haidilao' Smiling Again?

By Dolphin Research

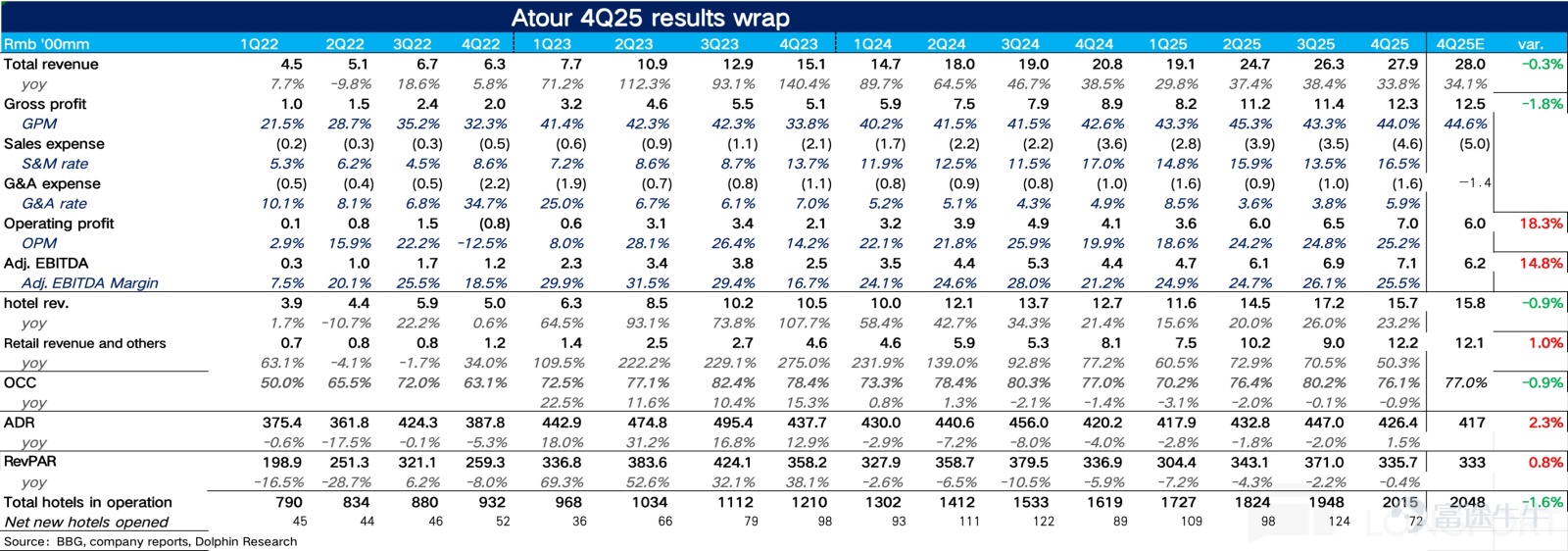

Before the US stock market opened on March 17, 2026, Beijing time, Atour (ATAT) released its Q4 2025 earnings report. Overall, Atour's performance this quarter was quite good, with revenue meeting expectations andbenefiting from the rapid growth of its retail business, operational leverage drove profits to exceed market expectations. Specifically: $Atour(ATAT.US)

1. Price stabilization and volume control, RevPAR slightly exceeded market expectations. Looking at the core operating metric, revenue per available room (RevPAR), Atour's RevPAR in Q4 was 336 yuan per night, representing a slight year-on-year decline of 0.4%, with the rate of decline continuing to narrow。Breaking it down,due to Atour's decision to scale back promotional efforts during the off-season, coupled with an increase in the proportion of high-end product lines such as S and X, the average daily rate (ADR) ended two consecutive years of negative growth and returned to positive growth, surpassing market expectations,while occupancy rate (OCC) seasonally declined during the off-season, showing mediocre performance.

2. The proportion of Qingju has further increased. In terms of store openings, Atour added a net total of 67 stores in Q4, bringing the total number of stores to over 2,000,with Atour 4.0 (Jianye) and Qingju being the main contributors to new openings.Although the pace of store openings was intentionally slowed during the off-season,the implied number of signed agreements suggests a recovery trend compared to Q3. Dolphin Research speculates that franchisees accelerated the signing of Atour 4.0 (Jianye) contracts by year-end to capture the business travel market in the upcoming spring season.

3. Retail business maintained rapid growth.Looking at revenue breakdowns, Atour's hotel business grew 23% year-over-year in Q4, remaining stable overall. Retail business revenue surged 50% year-over-year, and based on channel research information,Atour Planet achieved a record-high conversion rate on Douyin Live and Xiaohongshu in Q4, reaching a large number of non-hotel customers.,In addition, as Q4 is the peak season for down comforters and temperature-control blankets, Dolphin Investment estimates that the contribution of temperature-control blankets to GMV across the entire retail business further increased, driving stronger-than-expected retail performance.

Profitability reached a three-year high.Benefiting from explosive sales of high-priced, high-margin products in the retail segment,Atour’s gross margin in Q4 improved by 1.3 percentage points year-over-year.Sales and administrative expenses declined due to operating leverage, ultimately leading Atourto achieve an adjusted EBITDA of 710 million yuan, growing 61% year-over-year, surpassing market consensus (2.34 billion yuan).

Guidance for 2026 indicates growth of 20%-24%.Compared with market expectations of 21%-22% growth, the company's guidance aligns closely with expectations.

Overall view by Dolphin Intelligence:

First, regarding Atour's core business — its hotel operations — tightened travel budgets combined with survey data indicate that the industry aggressively promoted discounts like “50% off weekends” and “stay-longer discounts” in Q4 to maintain occupancy rates. For mid-to-upscale hotels, ADR fell 3%-5% year-over-year.

In contrast, Atour achieved positive growth in ADR by strictly controlling prices and increasing the proportion of its mid-to-high-end product lines, offsetting the seasonal decline in OCC.,Dolphin Investment believes this not only validates Atour's brand loyalty (users are willing to pay for value rather than opting for low prices) but also demonstrates to the market that it can escape the growth trap of 'cutthroat price competition.'

Additionally, regarding the high-growth retail business that the market is more focused on, looking ahead to 2026, short-term data combined with survey information shows that Atour's official Douyin sales reached 160 million yuan in January, a year-on-year increase of 67%.Compared to the 37% growth rate in December, this represents a clear acceleration month-on-month and indicates it is still in the rapid penetration phase.

To put it simply, considering the explosive growth of the Deep Sleep memory pillow over the past three consecutive years, traditional home textile giants have started upgrading memory pillows from previously peripheral complementary categories to strategic core products, attempting to capture market share from Atour Planet.Dolphin Investment conservatively assumes that the growth rate of Atour's pillows will further slow down from 40% in 2025 to 20% in 2026, corresponding to a GMV of 2.5 billion yuan.;

As for temperature-regulating quilts,given that the current market share is only 5% (compared to 18% for the Deep Sleep pillow), and traditional home textile giants have not quickly followed up, the competitive landscape remains relatively favorable.Therefore, Dolphin Investment assumes that the growth rate of temperature-regulating quilts will slightly moderate from 86% in 2025 but still maintain high growth at 65%, corresponding to a GMV of 1.4 billion yuan. For other product categories, assuming they double in size (over the past three years, the growth rate of Atour Planet’s non-quilt and non-pillow categories exceeded 150%), totaling 5.1 billion yuan, representing growth of more than 30%.Meanwhile, the market expects Atour's retail GMV to grow by 25%-30% in 2026. Therefore, Dolphin Investment believes there is a high probability that the retail business will exceed expectations.

The following is a detailed analysis:

1. Price protection and volume control, RevPAR slightly exceeded market expectations

1.1 ADR returned to year-on-year positive growth

Looking at the core operating metric of revenue per available room (RevPAR), in Q4 Atour's RevPAR was RMB 336 per night, a slight decline of 0.4%, but the trend shows the rate of decrease is still narrowing.

Breaking it down by volume and price,As Q4 is traditionally the low season, coupled with Atour’s deliberate reduction in promotional efforts, occupancy rate (OCC) experienced a seasonal decline.

On the pricing side,Considering that the hospitality and tourism industry has entered a phase of slower supply growth,,the recovery in business travel demand, combined with an increased proportion of premium product lines such as S and X, drove Atour's average daily rate (ADR) to achieve year-on-year positive growth in Q4,,offsetting the impact of minor fluctuations in occupancy rate. The average daily rate (ADR) turned from negative to positive, increasing by 1.5% year-on-year to reach RMB 426 per night.

The implied number of contracts signed in Q4 rebounded compared to Q3

In terms of store openings, Atour added a net total of 67 stores in Q4, bringing the total number of stores to over 2,000Among them, Atour 4.0 (Jianye) and Qingju were the main contributors to new store openings

Specifically, after validating the initial model, Atour 4.0 (Jianye) entered a phase of large-scale implementation in 2025, with 49 new stores added in Q4 (accounting for 73% of newly opened stores)These are concentrated in prime business districts of core cities such as Beijing, Shanghai, Guangzhou, and Shenzhen. Dolphin Research speculates that franchisees accelerated signings for Atour 4.0 (Jianye) by year-end to capture the business travel market in the upcoming spring season

In terms of positioningJianye targets both business and vacation scenariosIt meets the needs of business travelers for efficient work while offering a vacation-like relaxation experience, carving out a differentiated niche in the underserved mid-to-high-end hotel marketThis also validates the booming demand for experiential consumption。

Additionally, Qingju 3.0 serves as another key growth driver for Atour's expansion, accounting for 22% of new store openings,The core remains the ultra cost-performance ratio of Qingju. According to research information, the investment cost for a single room of Qingju 3.0 has been optimized to between 100,000 and 110,000 yuan, with the payback period for a single store controlled within three years,attracting a large number of franchisees who hold properties in 'non-core locations', desire quick returns, and pursue high efficiency per square meter。

II. Retail business remains the key growth driver

2.1 Group's overall revenue generally met expectations

In Q4, Atour Group achieved revenue of 2.79 billion yuan, representing a year-on-year increase of 33.8%, which was largely in line with expectations.

Breaking down by segment, hotel operations generated revenue of 1.57 billion yuan, up 23.2% year-on-year,On one hand, the continuous recovery of RevPAR drove an increased contribution from recurring management fees, while on the other hand, with the significant signings and launches of Qingju 3.0 and Atour 4.0, Dolphin Insights expects supply chain sales also saw a temporary rise during Q4.

With the reduction of directly operated stores, the direct operation segment generated revenue of 150 million yuan, reflecting a 9.8% year-on-year decline.

Retail operations achieved revenue of 1.22 billion yuan, growing by 43.9% year-on-year. Based on survey data, apart from Tmall, Atour's conversion rates from product placements on Douyin Live and Xiaohongshu hit new highs in Q4.,Successfully reached a large number of non-hotel customersMoreover, Q4 is the absolute peak season for down comforters and temperature-regulating comforters. The Dolphin analyst speculates that the contribution of temperature-regulating comforters to GMV in the overall retail business further increased, driving up the average order value in Q4.

2.2 Retail Business Gross Margin Significantly Increased

Atour's gross margin in Q4 was 44%, increasing by 1.4 percentage points year-over-year.

Breaking down the business, due to the increase in the proportion of franchise hotel business, newly franchised hotels are in a nurturing period within the first 3-6 months,The rise in labor costs caused the hotel business gross margin to slightly decrease by 1.7 percentage points to reach 35.8%.。

For the retail business,With the increase in high-margin products such as temperature-regulating comforters and deep-sleep pillows, combined with supply chain collaboration for cost reduction, the gross margin significantly improved by 3.9 percentage points to reach 54.4%.。

2.3 Expense Ratio Declined, Core Operating Profit Exceeded Expectations

On the expense side, although Atour continued to actively invest in advertising on platforms like Douyin and Xiaohongshu in Q4 to enhance brand awareness of Atour Planet, the sales expense ratio slightly decreased by 0.5 percentage points to 16.5% due to economies of scale. Due to upgrades in backend systems and talent cultivation, Atour’s Q4 administrative expense ratio temporarily increased. Ultimately, AtourAdjusted EBITDA reached 710 million yuan, a year-on-year increase of 61%, surpassing market consensus expectations (2.34 billion yuan)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment