Post-earnings 'flash crash'! Smoore International plunges over 18%, what exactly went wrong with the latest earnings report?

March 18th,$SMOORE INTL (06969.HK)$ 、 $TME-SW (01698.HK)$ 、 $160 HEALTH (02656.HK)$Several stocks experienced significant declines. Among them, Smoore International saw a dramatic plunge during trading, described as a 'waterfall-like' drop.As of the time of writing, it plummeted more than 18% on heavy volume, breaking below the consolidation range of the past few months.

Just the day before, after market close, Smoore International had just released its full-year 2025 'report card': record-high revenue and explosive growth in HNB business.

On one side are impressive growth figures, but on the other, the stock price is being rejected by investors. Positive earnings turned into negative sentiment for the stock. What 'landmines' are hidden in Smoore's financial report that are causing panic among investors?

Record-high revenue, but profits are lagging behind.

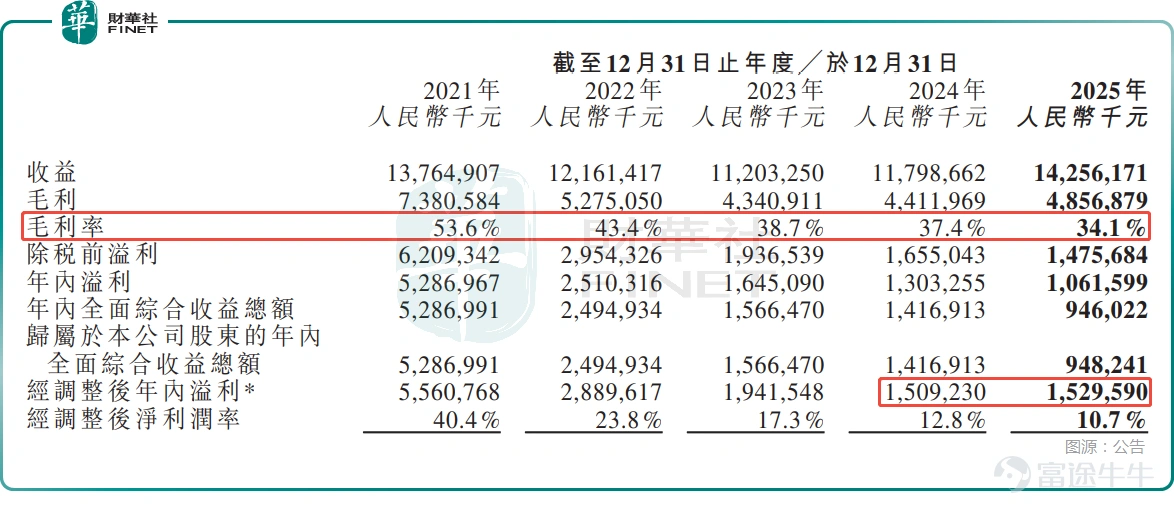

First, let's look at the headline numbers for 2025.Smoore International reported revenue of RMB 14.256 billion (RMB), a year-on-year increase of 20.8%, setting a new high since its listing, with an outstanding performance.

Smoore International mainly operates in two business segments: (1) Business-to-Business (B2B) operations, which focus on researching, designing, and manufacturing atomization products, Heat-Not-Burn (HNB) products, special-purpose atomization products, and atomized medical products for leading tobacco companies, independent vaporizer brands, and other corporate clients, while also providing related technical services around these products; (2) In-house brand operations, which focus on researching, designing, manufacturing, and selling proprietary electronic atomization products and atomized beauty products.

In 2025, the ToB business contributed revenue of 11.344 billion yuan, representing a year-on-year increase of approximately 21.7%.This growth was mainly driven by the performance of the atomization business.

Among this, HNB, which Smoore International has placed high hopes on, achieved notable commercial success after years of research and development—In 2025, HNB's revenue exceeded 1.2 billion yuan, helping strategic clients launch products in Japan and Europe, becoming the most certain growth driver for the future.

In 2025, the proprietary brand business recorded revenue of approximately 2.912 billion yuan, representing a year-on-year increase of about 17.6%,Benefiting from flagship product iterations, expanded channel coverage, and continued market share growth, the company’s proprietary atomization brand VAPORRESSO achieved growth again.

Despite impressive revenue performance, Smoore International faced challenges on the profit side, directly hitting a sensitive point in the market. Data shows that in 2025, the company's net profit was 1.062 billion yuan, a significant year-on-year decrease of 18.5%;The adjusted net profit was approximately 1.530 billion yuan, with only a slight year-on-year increase of 1.3%, almost 'zero growth'; an interim dividend of 20 Hong Kong cents per ordinary share was declared.

While Smoore International's revenue scale grew rapidly, its profits couldn't keep up, which might be the core trigger for investors voting with their feet.

What are the root causes behind the earnings 'turnaround,' and where did the money go?

The reason for Smoore International's significant revenue increase but only a slight rise in adjusted net profit is not complicated.

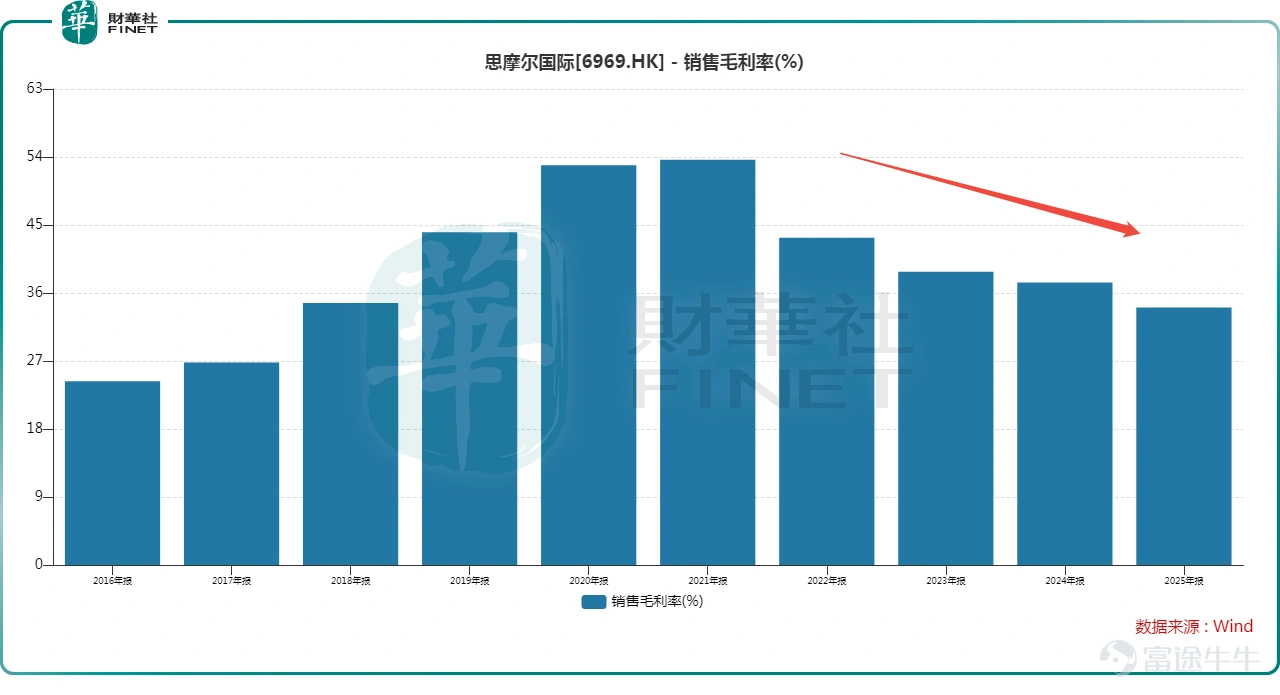

On one hand, the gross margin has been continuously declining, eroding the profitability base. Data shows,the company’s gross margin continued to drop to 34.1% in 2025,far below the levels of over 50% in earlier years.

On the other hand, the pressure from 'three high' expenses erupted, eating into profits. In 2025, Smoore International’s administrative expenses reached 1.286 billion yuan, surging 40.6% year-over-year, mainly due to increased share-based payments and compliance legal fees; R&D expenses amounted to approximately 1.523 billion yuan, down about 3.1% year-over-year, but still remained at a high level; although distribution and sales expenses slightly decreased, global investment in its own brand continued to increase.

In addition, the company recorded a foreign exchange loss of 151 million yuan for the full year, litigation settlement expenses of 176 million yuan, and income tax expenses increased by 17.7% year-over-year to 414 million yuan. Combined, these factors significantly dragged down net profit performance.

In terms of cash flow, Smoore International's net operating cash flow in 2025 was 487 million yuan, sharply declining from 1.753 billion yuan in the previous year, which is also worth noting.

Conclusion

Overall, Smoore International’s HNB and compliance logic have not been disproven, and its leading position remains solid. However, margin recovery, cost control, and cash flow improvement have become the market's most pressing questions. For the company, whether it can truly convert 'scale growth' into 'profit growth' in 2026 will determine if it returns to growth or continues to face valuation declines.

Author: Mingxi

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

8