Three major optical communication stocks have doubled this year. Will the momentum continue?

In the AI era, chase 'light'! The birth of three major alliances on the same day accelerates the innovation of optical interconnects. Who are the true core winners in the industry chain?

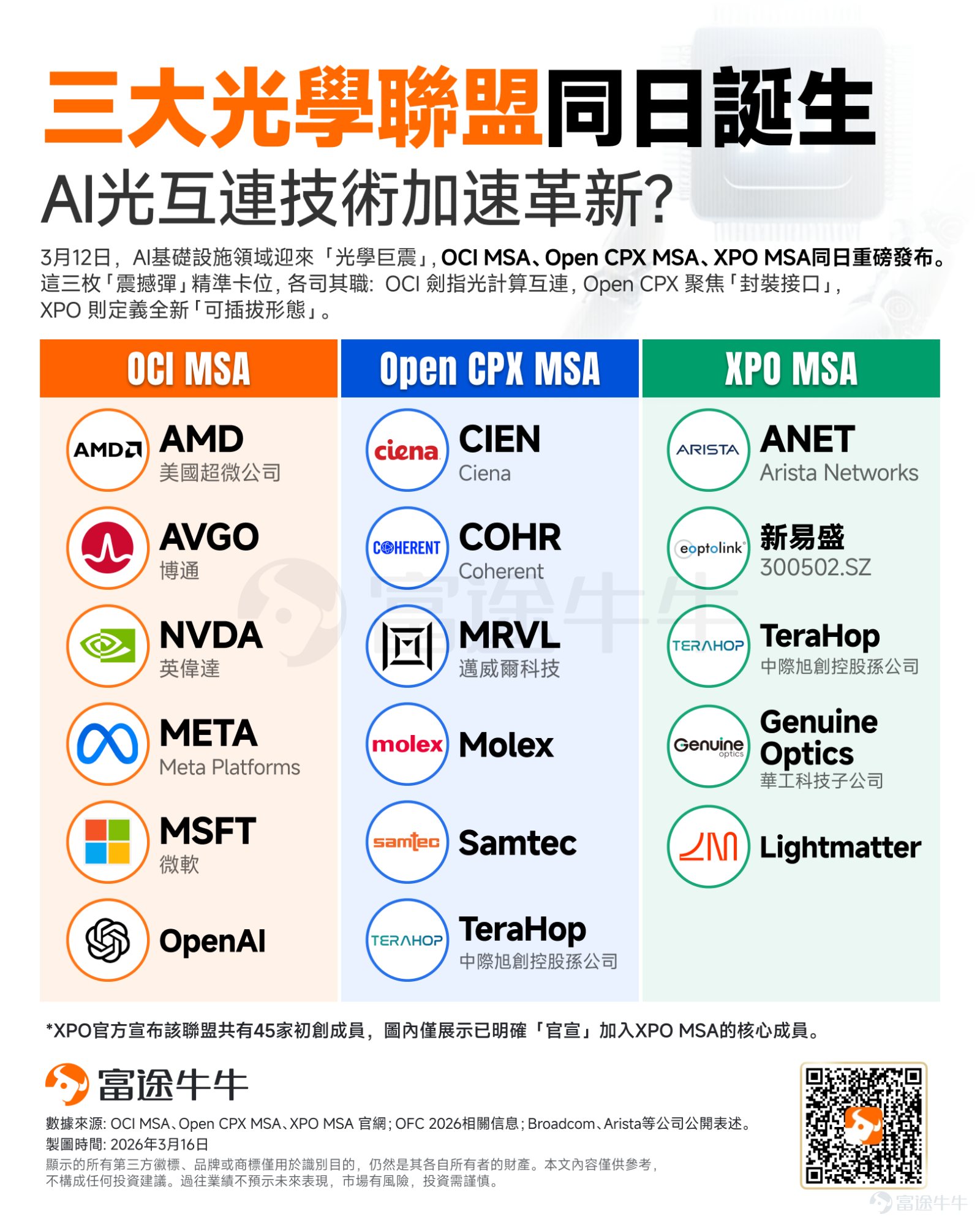

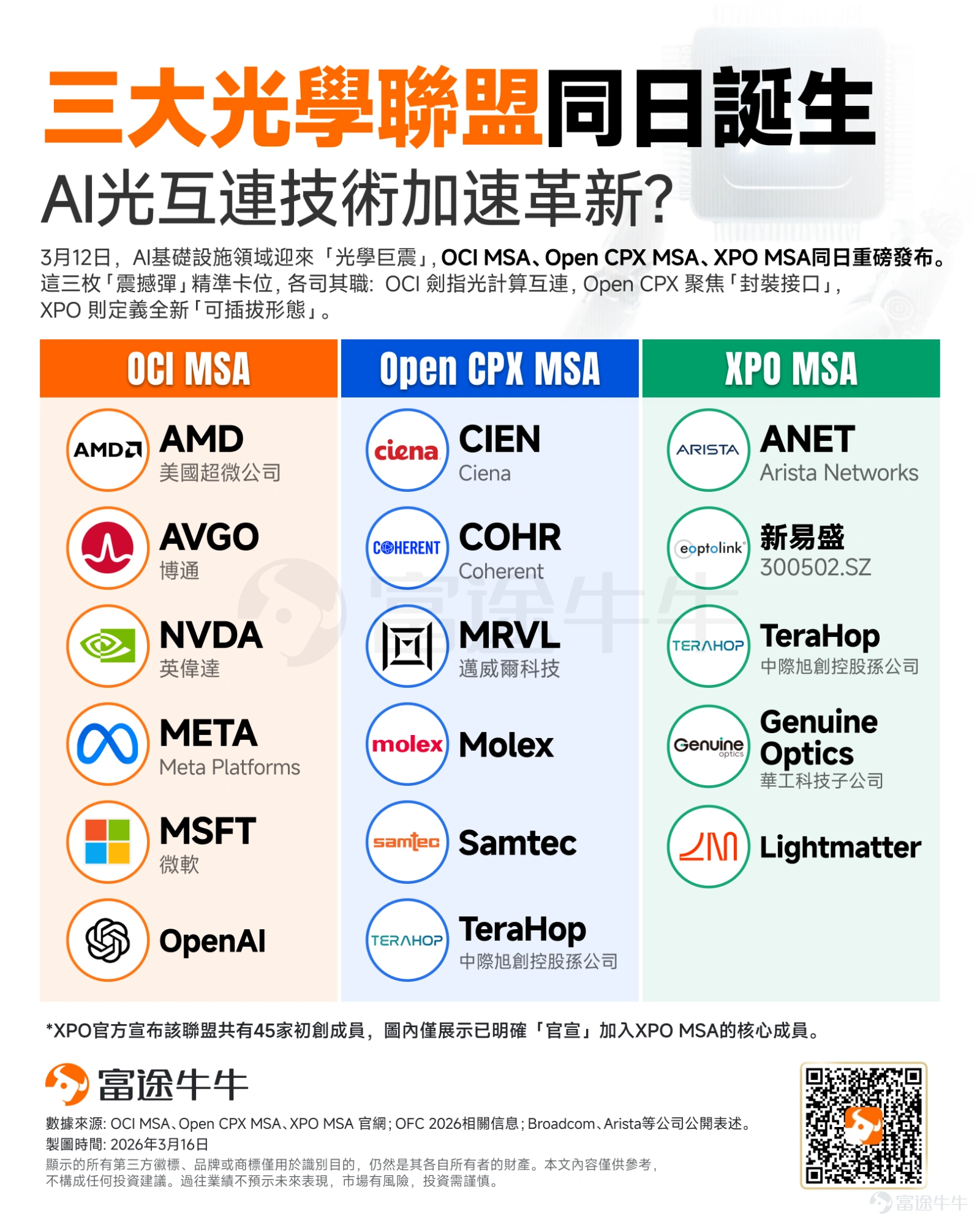

On March 12, just...$NVIDIA (NVDA.US)$Just before the opening of two major industry events, the GTC Conference and the prestigious international Optical Fiber Communication Conference (OFC), the AI infrastructure sector is experiencing an 'optical revolution'.OCI MSA, Open CPX MSA, XPO MSAreleased on the same day with significant impact.

In fact, the explosive growth of AI has placed unprecedented demands on data center networks (higher bandwidth, lower latency, denser clusters, and longer transmission distances).

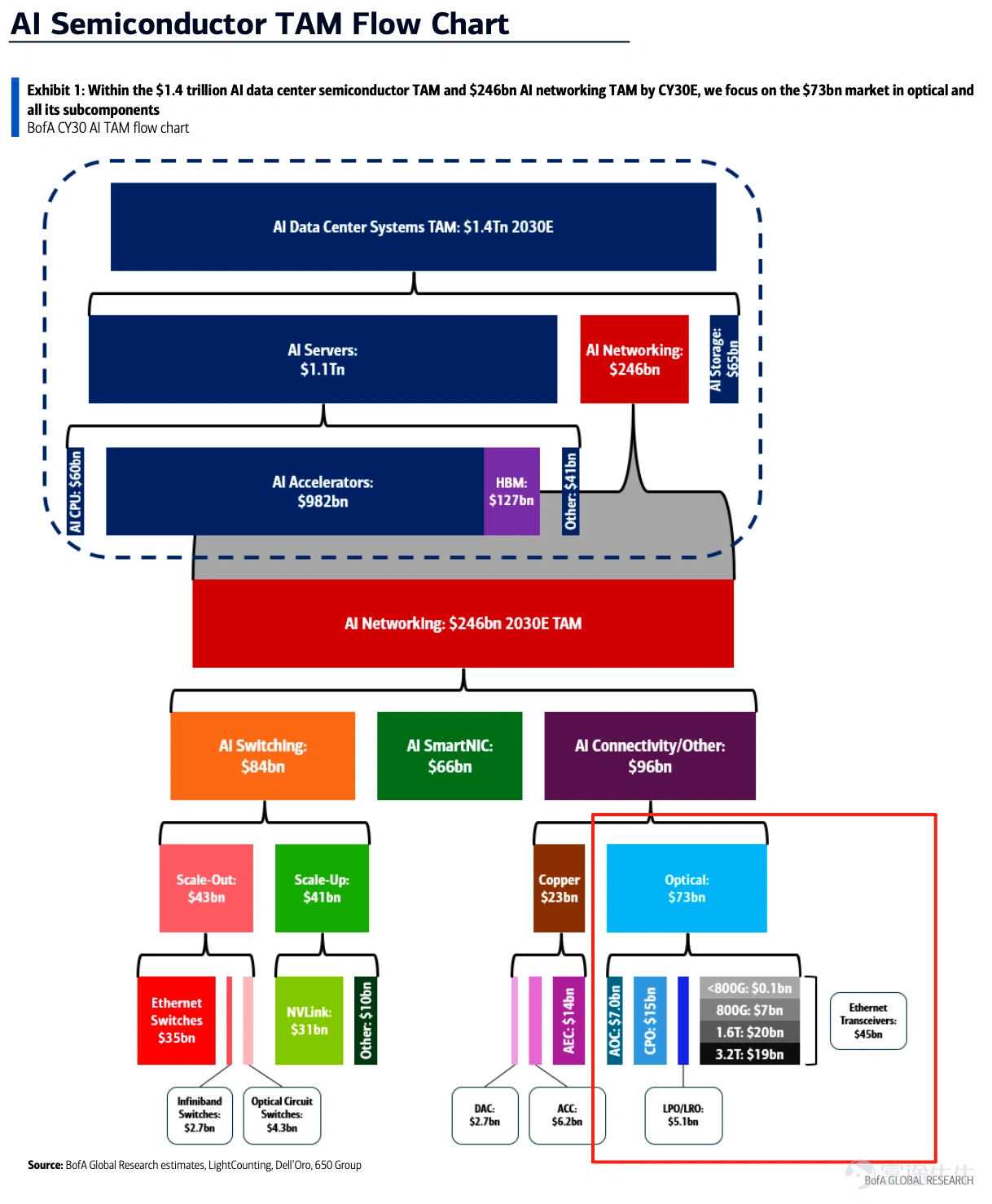

A Bank of America report highlights that the optical interconnects industry is in a highly advantageous position, with expectations that by 2030,the core market size for AI optical communications (TAM) will reach $73 billion, accounting for 29% of the total $245 billion AI network TAM.

The strong emergence of these three optical interconnect MSAs signals what exactly? Why is optics essential for AI data centers? This article will unravel these mysteries for fellow investors and provide an overview of unmissable investment opportunities across the upstream and downstream supply chain.

What signal is released behind the strong debut of these three optical interconnect MSAs?

The simultaneous launch of these three alliances marks the potential for AI interconnects to fully transition to 'optics.' They have clear divisions of labor, moving beyond mere technical experimentation into a new phase of standardization, mass production readiness, and multi-supply chain collaboration.

1. OCI MSA: Defines the 'physical transmission layer'

Full name Optical Compute Interconnect, it is currently the most representative optical interconnect alliance. Its rarest aspect lies in assemblingan "all-star lineup": covering AMD, Broadcom, Meta, Microsoft, NVIDIA, and OpenAI.

Core Significance: Chip giants, interconnect suppliers, supercomputing buyers, and pioneers in large models have gathered together, which means OCI is not targeting pain points of a single vendor but rather aims to collectively overcome the physical limits commonly faced in the AI scale-up domain.。

2. Open CPX MSA: Defining the "packaging interface"

If OCI solves "how to transmit," then Open CPX solves "how to install." This is a "standard socket alliance" built specifically for the era of co-packaged/near-packaged optics (CPO/NPO)."Standard Socket Alliance"。

Core pain point: Once CPO and NPO enter mass production, if optical engines lack unified standards, system manufacturers will face compatibility issues across different suppliers. The birth of Open CPX is precisely to standardize mechanical and electrical interfaces, thereby substantially reducing yield loss, maintenance difficulties, and replacement costs.

3. XPO MSA: Defining the 'Pluggable Form Factor'

Short for eXtra-dense Pluggable Optics, this route is being calledthe 'Counterattack of the Pluggable Camp'. For system manufacturers not yet ready to fully bet on CPO but urgently needing to boost bandwidth density, this represents a highly practical compromise solution.

Key metrics: Focused on defining the next generation of ultra-high-density pluggable optical module form factors. The target per-module rate aims directly at 12.8Tbps, significantly enhancing single-rack switching capacity; it also incorporates extreme high-power consumption challenges such as liquid cooling plates and over 400W heat dissipation considerations into the initial design phase.

The simultaneous establishment of these three MSA alliances may signal that the next round of AI infrastructure arms race has officially moved beyond the simple 'competition for computing chips'.A full-scale upgrade has turned into a battle for the underlying discourse power over who can dominate the framework of the optical era system.

Why are data centers moving towards an 'all-optical' necessity for AI?

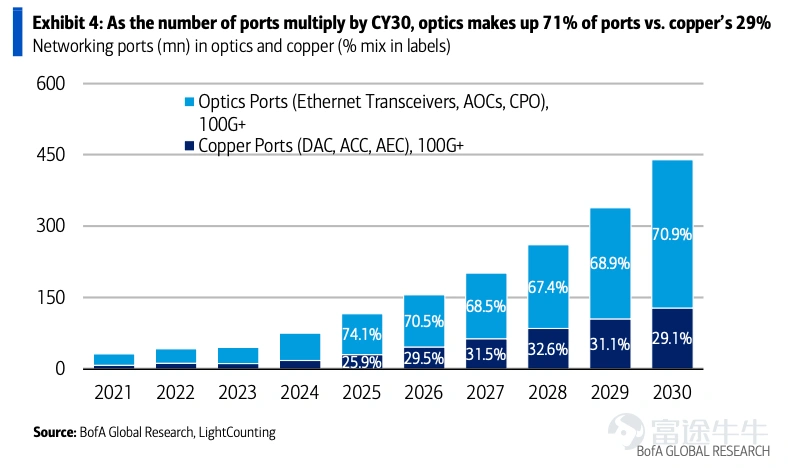

In data center networks, the industry traditionally follows the principle of 'using copper wherever possible and only using optics when necessary.' However, as AI clusters grow larger and denser, with inter-rack and intra-rack connection distances continuously extending, signal attenuation in traditional copper cables at higher speeds (such as 200G SerDes) becomes extremely severe. Even high-quality direct attach copper (DAC) cables typically have an effective transmission distance of only 2 meters.

As a result, optical interconnects have become essential for providing long-distance (over 10 meters), high-bandwidth, and low-latency connections. By 2030, optical ports are expected to account for 71% of total network ports, while copper ports will drop to 29%.

Source: Bank of America

What key technologies should be focused on in this technological transformation?

As AI clusters expand, optical communication equipment is undergoing three core phases of evolution from traditional pluggable modules to highly integrated and pure optical interconnects:

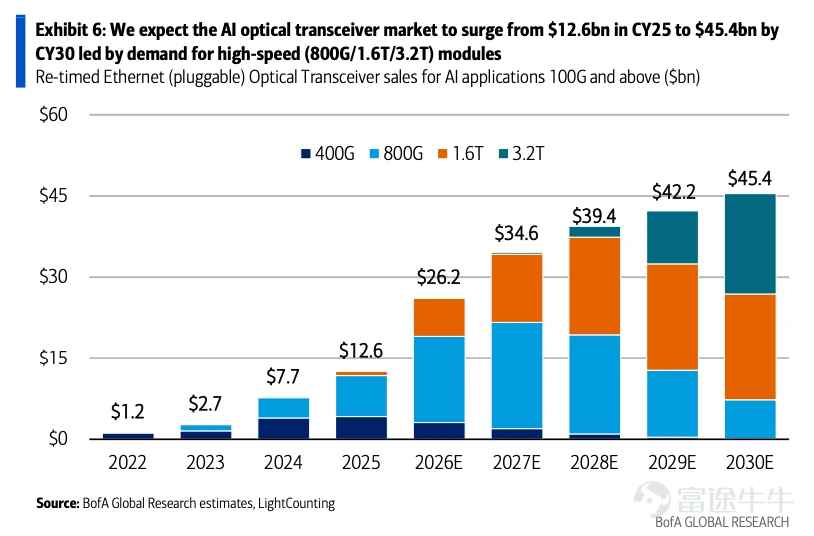

1. Pluggable optical modules: The current dominant force

Market status: Due to their practical form factor, flexible configuration, and strong performance in long-distance high-speed transmission, optical modules have remained the backbone of interconnects. Driven by the robust 800G cycle and the surge in 1.6T demand, this market is expected to grow from $12.6 billion in 2025 to $45.4 billion by 2030 (with a compound annual growth rate of 29%).

Source: Bank of America

Core pain points: Excessive power consumption. To compensate for signal loss at high speeds, optical modules rely on power-hungry DSPs (digital signal processors). At a rate of 1.6T, a single module can consume up to 30 watts, potentially accounting for up to 40% of the interconnect power in large AI clusters.

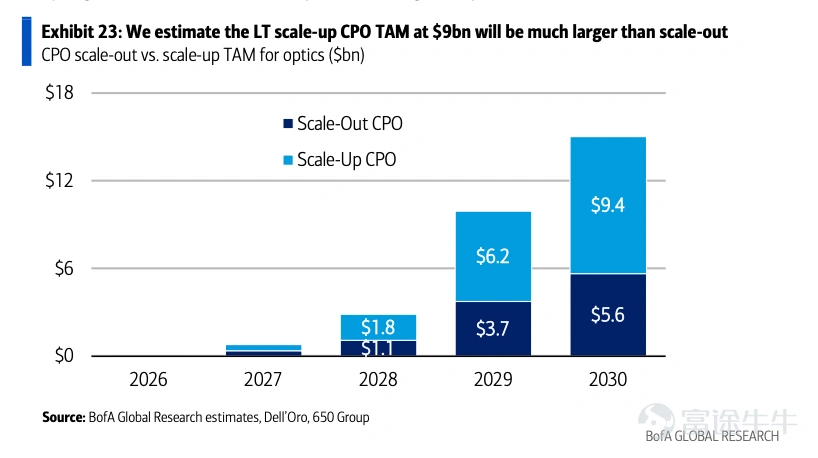

2. Co-Packaged Optics (CPO): The Future Breakthrough in Power Consumption

Technology Advantages:CPO integrates the optical engine and switch chip into a single package, significantly shortening the electrical signal path. This drastically reduces the transmission distance of electrical signals on the PCB, addressing both the power consumption and signal integrity issues of optical modules. For instance, NVIDIA’s Spectrum-X CPO solution cuts signal loss to 4dB with power consumption as low as 9 watts.

Source: Bank of America

Market Expectations: CPO is expected to gain attention by 2027, with its core component TAM projected to reach $15 billion by 2030. Among this, Scale-up networking will be the largest blue ocean for CPO, anticipated to grow into a $9 billion market.

Source: Bank of America

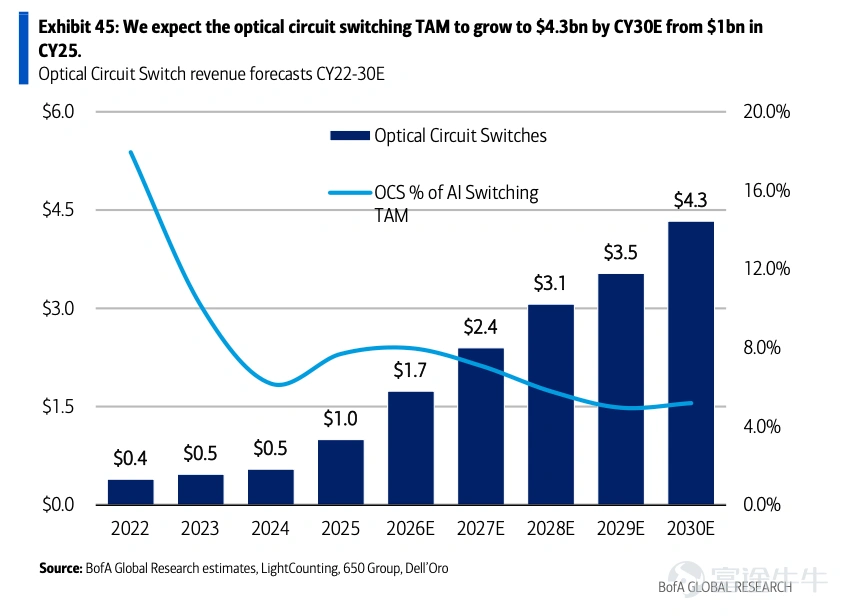

3. Optical Circuit Switch (OCS): Reshaping the Underlying Routing Architecture

Operating Mechanism:OCS is an all-optical network device that establishes optical paths directly between fiber optics using micro-electromechanical systems (MEMS) or liquid crystal technology, without the need to convert optical signals into electrical signals (eliminating OEO conversion).

Disruptive Value:Due to the absence of electrical signal processing and packet forwarding, OCS completely eliminates power consumption and latency caused by DSP. It has extremely low power consumption (only 100-200 watts) and is not limited by transmission speeds, making it compatible with multiple future generations of networks. Currently, it is being used as a replacement for traditional Spine switches and to provide network redundancy. The TAM is expected to grow from $1 billion today to $4.3 billion by 2030.

Source: Bank of America

Which companies in the industry chain are worth paying attention to?

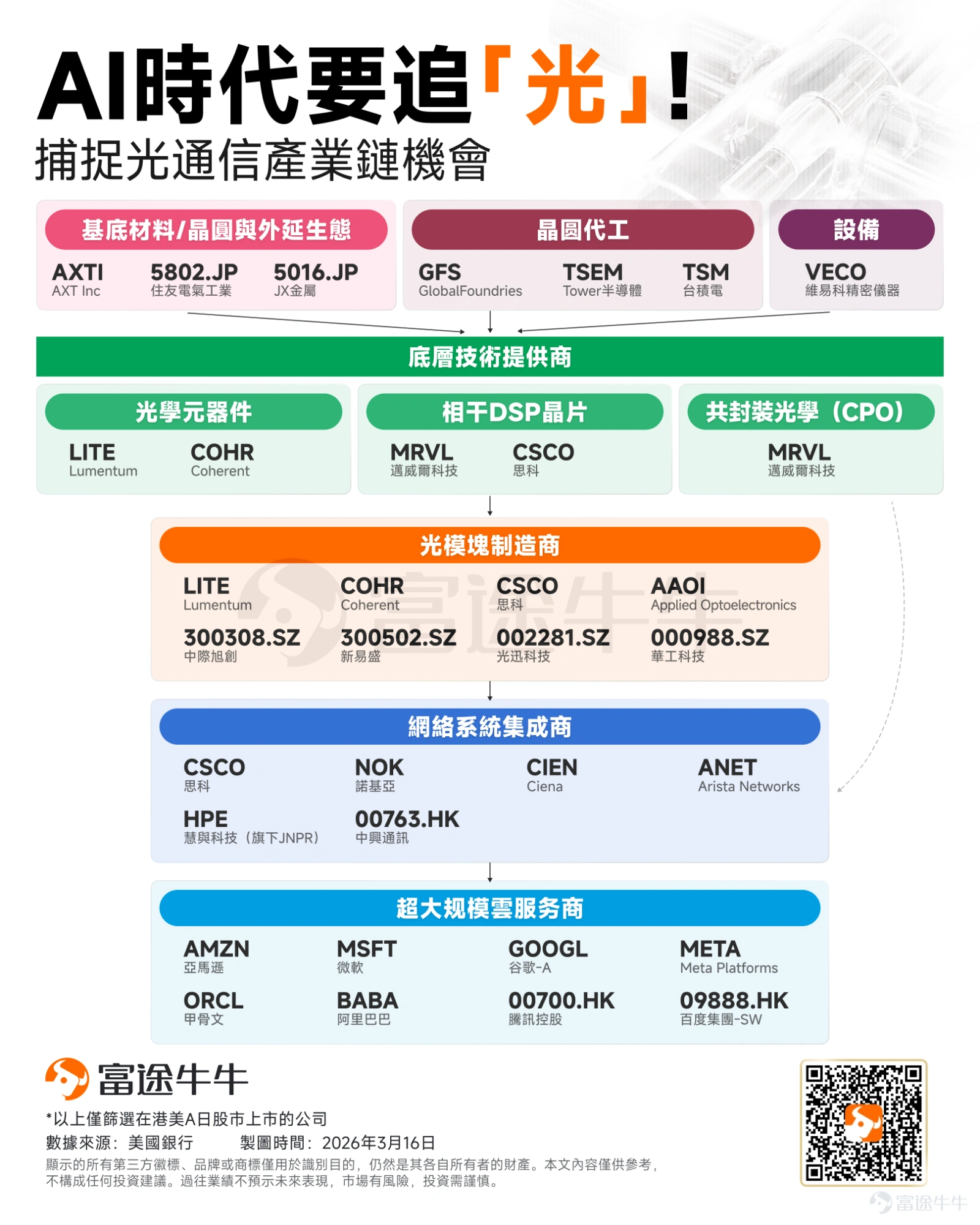

Bank of America also outlined the value chain of optical communications as follows:

1. Basic Technology Suppliers

These are the 'cornerstones' of optical communications, mainly involving underlying materials, manufacturing outsourcing, and core equipment.

Substrate/Wafer and Epitaxy:Representative companies include $AXT Inc (AXTI.US)$ 、 $Sumitomo Electric Industries (5802.JP)$ They provide substrate materials such as Indium Phosphide (InP) and Gallium Arsenide (GaAs), which are essential for manufacturing photonic chips.

Wafer foundry:Representative companies include $Taiwan Semiconductor (TSM.US)$ 、 $GlobalFoundries (GFS.US)$ 、 $Tower Semiconductor (TSEM.US)$ . With the rise of Silicon Photonics technology, photonic chips are increasingly reliant on advanced semiconductor foundry processes.

Equipment:Representative companies include AIXTRON、 $Veeco Instruments (VECO.US)$ . They are key suppliers of thin-film deposition equipment like MOCVD, acting as indispensable 'enablers' in the production of optoelectronic devices.

II. Core Component Suppliers

This is a part of the industry chain with extremely high technical barriers and substantial gross margins.

Optical components:Representative companies are $Lumentum (LITE.US)$ and $Coherent (COHR.US)$ . They provide core light-emitting and receiving components such as laser chips (e.g., VCSEL, EML) and photodetectors.

Commercial coherent DSP:DSP (Digital Signal Processor) is the 'brain' of high-speed optical modules, responsible for signal modulation and demodulation. $Marvell Technology (MRVL.US)$ is an absolute leader in this field, $Cisco (CSCO.US)$ also occupies an important position through the acquisition of Acacia.

CPO (Co-Packaged Optics): $Marvell Technology (MRVL.US)$ Recently announced the acquisition of Celestial AI. Celestial AI focuses on developing photonic interconnect hardware, with its core product being called 'Photonic Fabric (or Photonic Interconnect).' This technology uses optical signals instead of traditional electrical signals to transmit data between chips, aiming to achieve higher data transmission bandwidth with lower latency and power consumption.

III. Optical Module Manufacturers

This stage involves the packaging of optical chips, electrical chips, and structural components into final optical modules, representing the area with the densest competition and collaboration between Chinese and American companies.

Overseas Giants: $Coherent (COHR.US)$ 、 $Lumentum (LITE.US)$ 、 $Cisco (CSCO.US)$ as well as those focusing on cost-effectiveness $Applied Optoelectronics (AAOI.US)$ 。

Chinese Players:Chinese manufacturers account for a significant portion of the global optical module market, such as $Zhongji Innolight (300308.SZ)$ 、 $Eoptolink Technology Inc., (300502.SZ)$ , and $Accelink Technologies (002281.SZ)$ 、 $Hgtech (000988.SZ)$and others. They are the most direct beneficiaries of the current surge in AI optical modules.

IV. Network Equipment Integrators

These companies plug optical modules into their own switches and routers to build vast neural networks for AI data centers.

Core companies: $Arista Networks (ANET.US)$ is a leader in AI Ethernet switches, competing head-to-head with NVIDIA's InfiniBand architecture; traditional networking giant $Cisco (CSCO.US)$ 、 $Hewlett Packard Enterprise (HPE.US)$ under JNPR, $Ciena (CIEN.US)$ is also actively deploying AI networks; $Nokia Oyj (NOK.US)$ 、 $ZTE (00763.HK)$ is also a major global provider of telecom and data communication equipment.

5. Super cloud customers

The end point of the industry chain, and the driving force behind this explosive growth — the ultimate buyer of computing power.

North America Big4 + 1: $Microsoft (MSFT.US)$ 、 $Alphabet-A (GOOGL.US)$ 、 $Amazon (AMZN.US)$ 、 $Meta Platforms (META.US)$ , and $Oracle (ORCL.US)$ . Their capital expenditure (Capex) guidance directly determines the prosperity of the upstream optical communications sector.

Chinese Internet Giants: $Alibaba (BABA.US)$ 、 $TENCENT (00700.HK)$ 、 $BIDU-SW (09888.HK)$ , among others.

Bank of America notes that the entire value chain is benefiting,but there are a few core players worth paying attention to:

Component suppliers: $Lumentum (LITE.US)$ Hold a leading position in the high-speed laser field; $Coherent (COHR.US)$Leveraging its advantage in indium phosphide (InP) materials to expand its share in transceiver and CPO fields.

Lumentum: A leader in EML and CW lasers, and a key ultra-high-performance (UHP) laser partner for NVIDIA’s CPO systems. Additionally, LITE is the absolute leader in the MEMS optical circuit switch (OCS) market (e.g., R300 products).

Coherent: With capacity advantages in indium phosphide (InP), it continues to expand its share in lasers used for transceivers and CPO. Not only has it secured substantial CPO supply agreements with NVIDIA, but it is also currently the only supplier offering digital liquid crystal OCS (Liquid Crystal OCS) on the market.

DSP chip vendors: $Marvell Technology (MRVL.US)$A key beneficiary in the pluggable optical module market, its DSP chips are crucial in the transition from 800G to 1.6T.

Marvell Technology: Holds a strong market share in the DSP sector during the transition from 800G to 1.6T. Additionally, through the acquisition of Celestial AI, Marvell is aggressively entering the Scale-up CPO interconnect market for custom AI accelerators (XPU).

System and Ecosystem Builders: $NVIDIA (NVDA.US)$and$Broadcom (AVGO.US)$They are not only demand drivers but also technology enablers. NVIDIA is pushing its own CPO platform, while Broadcom positions itself as the leader in open, non-NVIDIA ecosystem-based CPO solutions.

NVIDIA: As the dominant player in the ecosystem, NVIDIA showcased its CPO-based Quantum-X (InfiniBand) and Spectrum-X (Ethernet) switch systems. It has signed multi-billion-dollar, multi-year supply agreements with LITE and COHR.

Broadcom: Provides a robust alternative for non-NVIDIA ecosystem CPO solutions. Its third-generation CPO switch ASIC, Davisson (TH6), offers a capacity of 102.4 TB/s, twice that of current competitors, while delivering 3.5 times better power efficiency.

Summary

Over the past two years, the focus of the AI supply chain has been on GPUs and computing servers. However, as model sizes continue to expand, along with explosive growth in computing density and data traffic, network infrastructure is becoming a new critical bottleneck. According to Bank of America, this signifies that the AI investment cycle is transitioning from a 'computing cycle' to a 'dual cycle of computing + networking.'With the upcoming NVIDIA GTC conference and OFC 2026, this could mark the beginning of a supercycle for optical modules.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

101

315