US $75 billion grid expansion, will Chinese power equipment see overseas growth? | In-depth analysis | Research report | Potential stocks | AI industry | Power sector

In March 2026, three major regional power grid operators in the US successively received approval for ultra-high voltage transmission expansion projects totaling $75 billion, marking the official start of an epic upgrade cycle for the North American power grid entering its implementation phase. This round of North American grid expansion is not a short-term event-driven phenomenon but rather a long-term trend driven by four major rigid demands: the explosive growth of AI computing power consumption, replacement of aging grid infrastructure, bottlenecks in renewable energy integration, and increased terminal electrification rates. Currently, there is severe hollowing out of domestic production capacity in the North American power grid, with a growing supply-demand gap for core equipment. Delivery times for key products such as transformers have extended to over 120 weeks, significantly increasing reliance on imports. Chinese power equipment companies, leveraging globally leading technology reserves, scaled production capacity, cost control capabilities, and fast delivery advantages, have gradually broken through market access barriers in North America, entering a golden window period for order fulfillment and earnings realization. We are optimistic about the sustained momentum of the power equipment sector amid the North American grid expansion cycle, with key players poised to benefit from both market expansion and global market share increases.

US Grid Expansion Project Brings Golden Development Period for Power Sector?

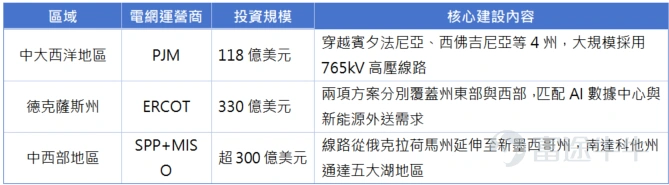

According to industry outlet The Information, over the past few months, America's three major regional power grid operators (covering Texas, the Mid-Atlantic region, and the Midwest) have successively approved transmission expansion projects totaling $75 billion. The core of this round of expansion is the construction of 765-kilovolt ultra-high voltage lines – currently the highest operational voltage level in the U.S., with a single line’s transmission capacity up to six times that of traditional lines; upon completion of these projects, the total mileage of these 'electricity highways' will expand from about 2,000 miles to 10,000 miles, quadrupling in size.

Specifically for the three regions, the layout of this expansion is clear: PJM Interconnection in the Mid-Atlantic region recently approved an $11.8 billion construction plan in February, with lines crossing Pennsylvania, West Virginia, Virginia, and Maryland, all adopting the 765-kilovolt ultra-high voltage specification for key sections; the Electric Reliability Council of Texas (ERCOT) has finalized investment plans totaling $33 billion across two large areas in the east and west; the Southwest Power Pool (SPP) and the Midcontinent Independent System Operator (MISO) in the Midwest are also advancing expansion projects with a combined scale exceeding $30 billion, covering vast areas from Oklahoma to New Mexico, and South Dakota to the Great Lakes. If all these projects come to fruition, it will establish the largest and most capable backbone power line network in U.S. history. Notably,Texas is simultaneously considering a third ultra-high voltage grid initiative – the 'Panhandle Plan.' American Electric Power has formally submitted this proposal to ERCOT, planning to invest approximately $10 billion to create an 'AI Power Corridor' specifically designed to support gigawatt-scale data centers in northern Texas; under full load, this project could theoretically support a maximum data center electricity load of 24 gigawatts.

The driving force behind this large-scale grid expansion lies in the growing anxiety over the imbalance between electricity supply and demand in the U.S. According to statistics from the International Energy Agency (IEA), in 2024, U.S. data centers accounted for 45% of the global data center electricity consumption, nearly double the scale of China. At the same time, the electricity demand of U.S. data centers continues to grow explosively. Bloomberg New Energy Finance predicts that by 2035, the share of U.S. data center electricity consumption in the nation's total electricity usagewill rise from 3.5% in 2024 to 8.6%, leading the growth rate across all industries, with its electricity consumption increase over the next five years even surpassing that of the new energy vehicle sector.

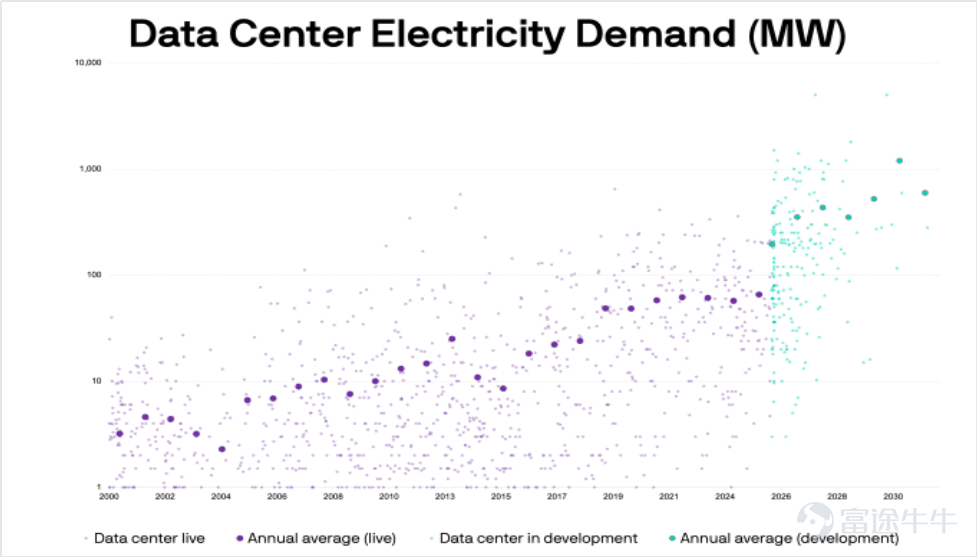

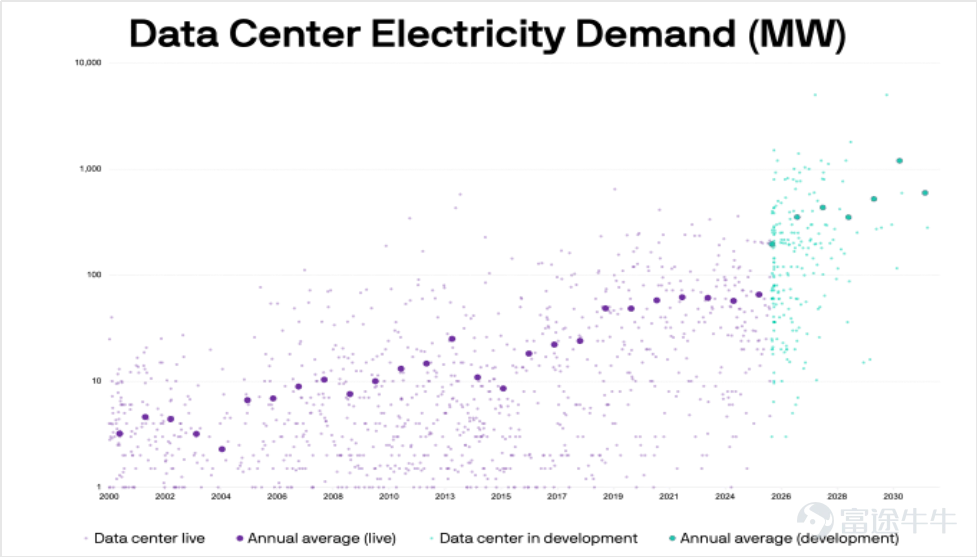

Figure 1: Power Demand Situation of Data Centers

Source: BloombergNEF

– North American Grid Expansion Amid AI Compute Surge

*Surge in AI computing drives exponential increase in data center electricity demand, pushing grid capacity to its limits

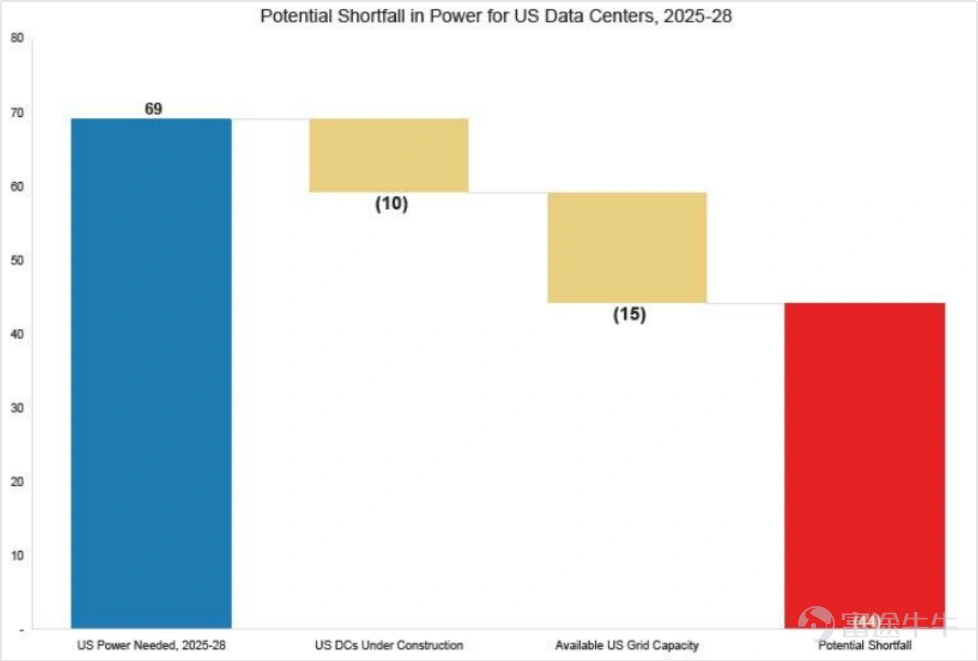

The explosive growth of the AI industry has directly driven up electricity demand at North American data centers, becoming the primary short-term catalyst and long-term incremental source for grid expansion. By the end of 2025, operational data center capacity in the U.S. will reach 44 GW, with 10 GW under construction and planned capacity exceeding 70 GW. It is estimated that from 2026 to 2030, U.S. data centers will add 80 GW of installed capacity, reflecting an annual compound growth rate as high as 23%. In terms of electricity scale, U.S. data center electricity consumption grew from 76 TWh in 2018 to 176 TWh in 2023, increasing its share of the nation’s total electricity usage from 1.9% to 4.4%, with projections indicating it will reach 325-580 TWh by 2028, accounting for 6.7%-12.0% of the total. Morgan Stanley forecasts that the cumulative electricity shortfall for U.S. data centers will rise from 44 GW in 2025-2028 to 47 GW, equivalent to the total electricity consumption of nine Miami cities. The continuous growth of AI computing has become a rigid constraint on the U.S. power grid, making grid expansion and upgrades to related distribution facilities a prerequisite for the development of the AI industry.

In addition to AI computing power, the rapid advancement of electric vehicles, heat pumps, and industrial electrification is continuously driving up the long-term growth rate of electricity demand in the United States. The U.S. Department of Energy forecasts that annual electricity demand growth will reach 3.2% by 2030, more than three times the growth rate of the previous decade, with data centers alone contributing 2% annual growth. Regarding electric vehicles,The United States aims for a 50% penetration rate of new energy vehicles by 2030, which corresponds to a charging station installation demand of over a million units, bringing significant distribution network upgrade requirements. The popularization of civilian electrification equipment such as heat pumps and electric heating, along with the increase in industrial electricity consumption due to the return of manufacturing, will continue to drive up grid load, forcing a comprehensive upgrade of the grid's transmission and distribution capabilities.

Figure 2: Potential electricity gap for U.S. data centers from 2025-2028

Source: Morgan Stanley Research

* Severe aging of grid equipment, replacement demand has strong rigidity

North America’s grid construction began in the 1960s-70s, and core equipment has now generally reached the end of its service life, with the aging problem being extremely severe. By 2025, 70% of transformers and 70% of transmission lines in the U.S. will have been in use for over 25 years, while 60% of circuit breakers will be over 30 years old. The average service life of grid infrastructure exceeds 40 years, far beyond its designed lifespan. Aging equipment directly leads to a significant decline in power supply reliability; in 2024, the average annual outage duration per U.S. customer surged to 662.6 minutes, an 80.74% year-on-year increase. In Texas, where data centers are concentrated, the annual outage time reached 1,614.3 minutes, a 176.85% year-on-year increase. The American Society of Civil Engineers rated the U.S. grid at only C-, with outdated equipment experiencing failure rates seven times higher than new equipment under extreme weather conditions. Replacement demand for existing equipment is urgent, forming the foundation of grid investment.

Additionally, the U.S. Department of Energy has set a goal of achieving 100% clean electricity by 2030, planning for 300 GW of wind power capacity and 700 GW of photovoltaic capacity by then. However, there is a serious geographical mismatch between U.S. renewable resources and load centers — wind energy is concentrated in the Midwest plains, solar power in the southwestern deserts, while load centers are clustered in densely populated areas on the east and west coasts. The aging grid system and insufficient inter-regional transmission capacity have become core bottlenecks for renewable energy integration. By 2025, the national curtailment rate of wind and solar power in the U.S. has risen to 12%, with certain areas in West Texas seeing curtailment rates exceeding 25% due to transmission bottlenecks. Grid Strategies estimates show that the U.S. needs to build 5,000 miles of high-voltage transmission lines annually to match renewable energy installation demand, but only 888 miles were completed in 2024, resulting in a severe supply-demand imbalance.Only through the construction of ultra-high voltage transmission lines, creating cross-regional 'electricity highways,' can renewable energy installations truly be activated and energy transition goals realized.

– Policy implementation and planning lead to a substantial increase in grid companies' capital expenditures.

In March 2026, the three major regional grid operators in the United States were successively approved for a total of $75 billion in transmission expansion projects. The core focus is constructing ultra-high voltage 765kV lines, the highest voltage level in the U.S., with a transmission capacity six times that of traditional 345kV lines, serving as the key solution to address inter-regional transmission bottlenecks. After project completion,The mileage of high-grade transmission lines in the United States will increase significantly from 2,000 miles to 10,000 miles, a fourfold expansion, marking the largest upgrade to the U.S. power grid in decades.

On the policy front, the U.S. government has continued to remove obstacles for grid expansion. On one hand, it has greatly streamlined the approval process for energy projects, reducing the approval cycle for grid and power projects from several years to around 60 days, significantly accelerating project implementation. On the other hand, the Inflation Reduction Act (IRA) provides tax credits and subsidies for grid upgrades and new energy grid integration projects, offering long-term funding guarantees for grid investments. Meanwhile, the White House convened seven major tech giants—Amazon, Google, Meta, Microsoft, and others—to sign the 'Electricity Payer Protection Commitment,' stipulating that newly built AI data centers must be self-sufficient in electricity, with their own power sources and supporting transmission facilities, without encroaching on public grid capacity or driving up residential electricity prices. This policy directly encourages tech giants to increase investment in microgrids, distribution equipment, and self-owned power sources, creating a dual-driven investment pattern of public grids and corporate self-built grids, further amplifying the market demand for power equipment.

Leading power companies have simultaneously increased their capital expenditure plans, with grid investments entering the substantive implementation phase. American Electric Power (AEP) announced a five-year capital expenditure plan of $72 billion, a significant increase of 33% over previous plans, primarily targeting 765 kV transmission projects in Texas and the PJM Interconnection region. By 2030, the company expects its peak load to reach 65 GW, a 76% increase from current levels. Additionally, Duke Energy, Southern Company, and other leading North American utility companies have also raised their transmission and distribution investment plans for 2025-2030, fully verifying the feasibility and sustainability of grid investments.

In terms of market sizing, if the $75 billion ultra-high voltage (UHV) transmission projects are implemented as planned, combined with the replacement demand for existing equipment, the market size for core UHV transmission and transformation equipment alone exceeds $50 billion, with the complementary distribution equipment market exceeding $30 billion, bringing the total market size to over $80 billion. Among this, transformers, GIS switches, and cables are the key growth areas, accounting for over 60% of the value.

Figure 3: Distribution of the $75 billion ultra-high voltage transmission project by region

Source: The Information

– Which domestic companies are likely to benefit?

The U.S. power system is experiencing the largest investment cycle since the 1970s, compounded by the surge in electricity demand driven by the rapid development of the AI industry. Relevant grid construction projects are unlikely to be completed in the short term. Currently, there is a severe bottleneck in the supply of power equipment in North America. For core equipment, only the Hyundai HICO factory in Memphis, Tennessee, within the U.S., is capable of producing 765 kV ultra-high voltage transformers, and domestic production capacity cannot meet project demands, with 80% of large power transformers being imported. The supply-demand mismatch has directly led to extended delivery times for core equipment and continuously rising prices. Currently, overseas grid equipment companies' high-voltage transformer schedules extend to 2030, with large transformer delivery cycles in the U.S. now exceeding 120 weeks, and distribution transformer delivery cycles surpassing 52 weeks. By 2025, the shortfall in large transformers in the U.S. is expected to reach 14,000 units, while the gap in distribution transformers will rise to 123,000 units. Subsequent supply-demand pressures on high-voltage switches, insulation materials, and other supporting components will also intensify, making the already scarce 765 kV ultra-high voltage capacity even more strained.

Amidst the widening supply gap, in addition to existing high-voltage electrical equipment groups in the U.S. and Europe, relevant demand is likely to spill over to high-voltage/ultra-high voltage enterprises in Japan, South Korea, and China. Companies that have completed product layouts, possess strong reputations, obtained North American certifications, and can deliver quickly will be the first to seize market opportunities, wielding significant pricing power with product premiums reaching 10%-80%. Profitability and earnings certainty will increase substantially, while the lengthy 5-10+ year market validation cycle for overseas high-voltage electrical equipment further reinforces the competitive edge of companies with first-mover advantages.

The implementation of the $75 billion U.S. ultra-high voltage grid expansion project, coupled with explosive growth in electricity demand from AI data centers, not only boosts equipment needs across the entire transmission and distribution industry chain but also creates surging demand for gas turbines in sectors like new energy grid integration and highly reliable distributed power for AIDCs, delivering clear offshore benefits to domestic power equipment companies. Among these, the ultra-high voltage main grid core equipment sector offers the highest certainty and greatest value. Products in this sector have high technical barriers and long certification cycles, meaning companies that have already achieved North American market access and possess scalable production capacity will directly enjoy the dividends of market expansion. Key targets include global transformer leaders.$TBEA Co., Ltd. (600089.SH)$ , high-voltage switch/GIS leader $Henan Pinggao Electric (600312.SH)$ , full industry chain national team for ultra-high voltage $China XD Electric (601179.SH)$ , pioneer in high-voltage switch exports $Sieyuan Electric (002028.SZ)$. In this round of American Electric Power system upgrades, gas turbines are core equipment for peak shaving integration of wind and solar new energy and uninterrupted power supply for AI data centers. Demand has surged simultaneously; currently, global gas turbine giants' order schedules are generally extended to 2028-2030, with the supply-demand gap continuing to widen. Investors may focus on Hong Kong stocks $DONGFANG ELEC (01072.HK)$ and $SH ELECTRIC (02727.HK)$ : $DONGFANG ELEC (01072.HK)$ is a domestic leader in heavy-duty gas turbine localization, with self-developed F-class G50 gas turbines achieving 100% intellectual property autonomy. The cumulative commercial operation time exceeds 12,000 hours, demonstrating fully proven technical reliability. Its core advantage lies in a delivery cycle of 13-14 months, far faster than the overseas giants' average schedule of over three years. At equivalent power, construction and maintenance costs are 15%-20% lower. It has achieved breakthroughs in exporting complete heavy-duty gas turbines, with products fully adaptable to grid peak shaving and distributed energy scenarios for data centers. Sufficient production capacity is in reserve, allowing direct承接of North American market order overflow. $SH ELECTRIC (02727.HK)$ By partnering with Ansaldo, it has mastered the full-chain core technology of F/H-class heavy-duty gas turbines, with capabilities to deliver integrated solutions and full lifecycle services. The independently developed F-class gas turbine is about to achieve mass production, with ongoing overseas market certification. Backlog orders are robust, and it will fully benefit from the dual dividends of American Electric Power's grid flexibility transformation and AI data center power supply demands.

Disclaimer: Any information provided in this report regarding or related to any investment or potential transaction is subject to the applicable laws and regulatory requirements of your jurisdiction, and you are solely responsible for ensuring compliance with such laws and regulations. The content of this report is for reference purposes only and does not constitute investment advice. Our company has made every effort to ensure the accuracy of the financial information provided, but we assume no responsibility or provide any form of guarantee regarding the accuracy, completeness, or effectiveness of all or any part of the content. We will not be held liable for any errors or omissions. Please also note that securities and virtual asset prices can fluctuate, particularly with very high risks associated with virtual assets, and investors should exercise caution and bear investment risks on their own.

———————————————————————

About the author:

Victory Securities - Hong Kong's Leading Virtual Asset Broker

Victory Securities (08540.HK), with over 50 years of history in Hong Kong, is a comprehensive full-service licensed brokerage offering four main business services to retail investors, institutional investors, high-net-worth clients, and enterprises: wealth management, asset management, virtual assets, and capital markets. It has received numerous accolades and essential qualifications in the Asia-Pacific region. In 2023, Victory Securities became the first licensed brokerage in Hong Kong to hold licenses issued by the Securities and Futures Commission for virtual asset trading, advisory, and asset management services. It was also approved by the SFC to provide virtual asset trading and advisory services to retail investors, offering one-stop compliant and legal Bitcoin and Ethereum trading, exchange, and deposit/withdrawal services.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

7