Tech giants share the electricity costs! Is the power sector entering a golden era?

Oracle Earnings Preview: Unlikely to Turn Around Based on Performance Alone, Market Wants to See a Long-Term Optimistic Outlook!

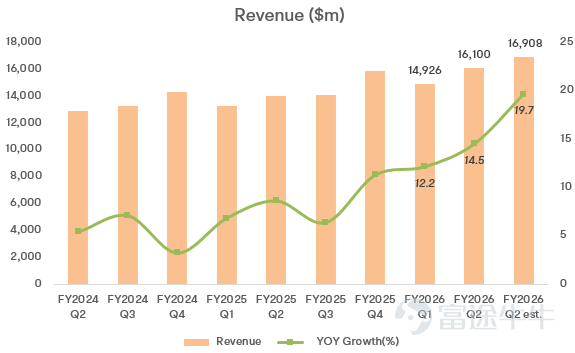

$Oracle (ORCL.US)$ Oracle is set to announce its Q3 FY2026 results after the US stock market closes on March 10. The market currently expects Oracle to deliver a report card showing revenue growth of around 20% year-over-year and adjusted net profit growth of approximately 15% this quarter.

But for investors, the key point of observation now is no longer demand, or even single-quarter performance, but whether the company can convert orders into revenue more quickly while keeping costs, capital expenditures, and financing pace within an acceptable range, and most importantly, provide guidance on whether the return on such large Capex will be sufficiently high.

Earnings Expectations

Wall Street widely expects Oracle's revenue this quarter to be approximatelyUSD 16.9 billion, with adjustedearnings per share between USD 1.70 and 1.71。

In terms of EPS, Oracle's sale of its stake in Ampere, an Arm server chip maker, last quarter brought in aboutPre-tax profit of $2.7 billion, equivalent to approximately$0.75 per share. Therefore, if we only look at the profit growth rate this quarter, it is possible that it will continue to be affected by one-off items, making its reference value lower than revenue and cloud business metrics.

Two key highlights

1. Whether RPO and OCI growth rates can exceed expectations

As of the end of last quarter, Oracle'sRemaining Performance Obligation (RPO) reached $523.3 billion; of which the portion expected to be recognized within the next 12 months increased year-over-year by40%。

In terms of revenue, in the previous quarter the companyTotal cloud revenueis7.98 billion US dollars, growing by34%; currently the largest growth driver - OCI (Oracle Cloud Infrastructure) revenueis4.08 billion US dollars, growing by68%。

The market is now more focused on not how many large contracts Oracle has signed, but rather how quickly these contracts can be converted into deliverable capacity and recognizable revenue.

On the supply side, Oracle's update last quarter was not bad. The company disclosed that there are currently147 customer cloud regions already online, with another64 regions in planning; during the quarter, nearly400 megawatts (MW) of data center capacity, with GPU delivery capability increasing by 50% quarter-over-quarter, and has deployed over96,000 NVIDIA GB200 GPUs。

2. Intensity of capital expenditure and cash flow pressure

Oracle inthe first half of fiscal year 2026has already reached20.5 billion US dollars。

In the past 12 months, the company'soperating cash flowis22.296 billion US dollarsandCapital expendituresas high as35.477 billion US dollars, implyingFree cash flow was negative 13.181 billion US dollars。

More notably, management had previously stated thatCapital expenditures for fiscal year 2026 will be approximately 15 billion US dollars higher than initially expected after the Q1 earnings reportand are highly likely to continue rising in the coming fiscal years.

This is where the market's divergence on Oracle has widened. In the past, investors were more accustomed to viewing it as a high-profit, strong cash-flow software company; however, following the accelerated investment in AI infrastructure, Oracle’s balance sheet and capital expenditure curve have become much heavier, naturally leading to a shift in valuation logic.

To support expansion, the company announced on February 1st its plan to raise 45 to 50 billion US dollars in funding by calendar year 2026. Approximately half of this will come from equity-related financing and common stock issuance, including an ATM offering plan of up to 20 billion US dollars; the other half will come from investment-grade unsecured debt financing.

Oracle stated that these funds will be used to support contracted customer needs, with the client list including AMD, Meta, NVIDIA, OpenAI, TikTok, and xAI, among others.

Option pricing

The current options market implies a potential Oracle stock price fluctuation of approximately +/- 11% post-earnings. Historically, in the last nine earnings reactions, Oracle shares have closed higher five times.

Summary

The market is gradually losing interest in the heavy asset Neo-clouds that continue to burn cash with no returns in sight under the AI theme. In contrast, profiting from the current 'pick-and-shovel' plays in light, storage, and power seems like a much easier proposition.

Unless OCI and RPO significantly exceed market expectations this earnings season, the impact of results alone on boosting the stock price is expected to be very limited. Potential surprises could come from management's discussion during the conference call regarding capacity deployment, customer payment structures, and capital expenditure return cycles, presenting a long-term optimistic and sufficiently attractive outlook.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

13

35