Rocket Lab's revenue guidance accelerates, but the Neutron launch is delayed again. Is it still worth investing in this formidable rival of SpaceX?

$Rocket Lab (RKLB.US)$ Rocket Lab released its Q4 and full-year financial results for 2025 after the market close on February 26 EST. The company reported record quarterly revenue and annual revenue of $602 million, achieving a 38% year-over-year growth rate, with order backlog surging 73% year-over-year to $1.85 billion. However, due to prior issues with the first-stage fuel tank design, management disclosed that the maiden flight of the Neutron rocket has been postponed to Q4 of this year. Additionally, revenues from the Space Systems segment, which involves satellite manufacturing, declined 9.1% quarter-over-quarter.

Core Financial Indicators

Q4 revenue reached $179.7 million, representing a 35.70% increase year-over-year, surpassing expectations of $178.2 million.

Net loss amounted to $52.02 million, marking a 1.1% decrease year-over-year but slightly better than expected.

Earnings per share: Adjusted net loss per share in Q4 was $0.09, with losses widening quarter-over-quarter primarily due to the recognition of a $41 million tax benefit in Q3. Adjusted EBITDA loss was $17.4 million, below the guided range of a $23-29 million loss.

Business Breakdown

Rocket Lab’s operations are divided into two segments: launch services and space systems. Revenue and gross profit by segment are as follows:

Launch Services:

This segment generated $75.9 million in revenue for Q4, reflecting an 85% surge quarter-over-quarter.

The Electron rocket completed seven launches in Q4, bringing the total number of successful missions for the year to 21. Rocket Lab secured 30 new dedicated launch contracts in 2025. However, the market is most anticipating updates on the progress of the Neutron rocket, which has a payload capacity of 13 tons. This remains the single biggest factor impacting Rocket Lab's stock price.

The maiden flight of the Neutron rocket has been postponed from its original schedule to the fourth quarter of 2026. Earlier in January 2026, Rocket Lab experienced a tank rupture incident during testing. Management disclosed on the recent earnings call that the root cause of the fault was identified as defects arising from the manual layup process. The mechanism behind the fault has been understood and related investigations have been completed. The company stated it will prioritize the rocket's reliability and not rush the timeline.

Space System:

Revenue for the Space Systems segment in the fourth quarter was $103.8 million, a 9.1% decrease quarter-over-quarter. The decline in revenue for this segment was primarily due to non-linear project revenue recognition and delays from subcontractors.

Previously, in December 2025, the company secured a contract with the US Space Development Agency (SDA), under which Rocket Lab plans to design and manufacture 18 satellites. Other winning contractors include Lockheed Martin, Northrop Grumman, and L3Harris. Given Rocket Lab’s relatively smaller revenue scale compared to other contractors, this contract is expected to bring significant revenue growth. Following the earnings announcement, the company reaffirmed the value of this contract at $816 million.

Positive Signals from the Earnings Report

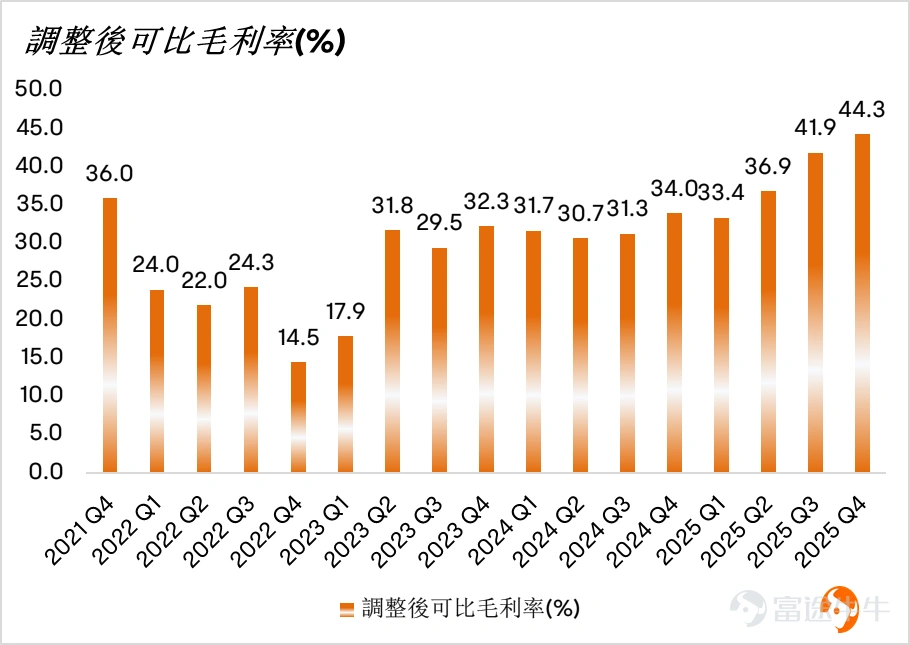

Both divisions of the company achieved record-high gross margins. Rocket Lab's overall adjusted gross margin for Q4 also hit a new high, mainly driven by increased launches of the Electron rocket, which optimized fixed-cost amortization.

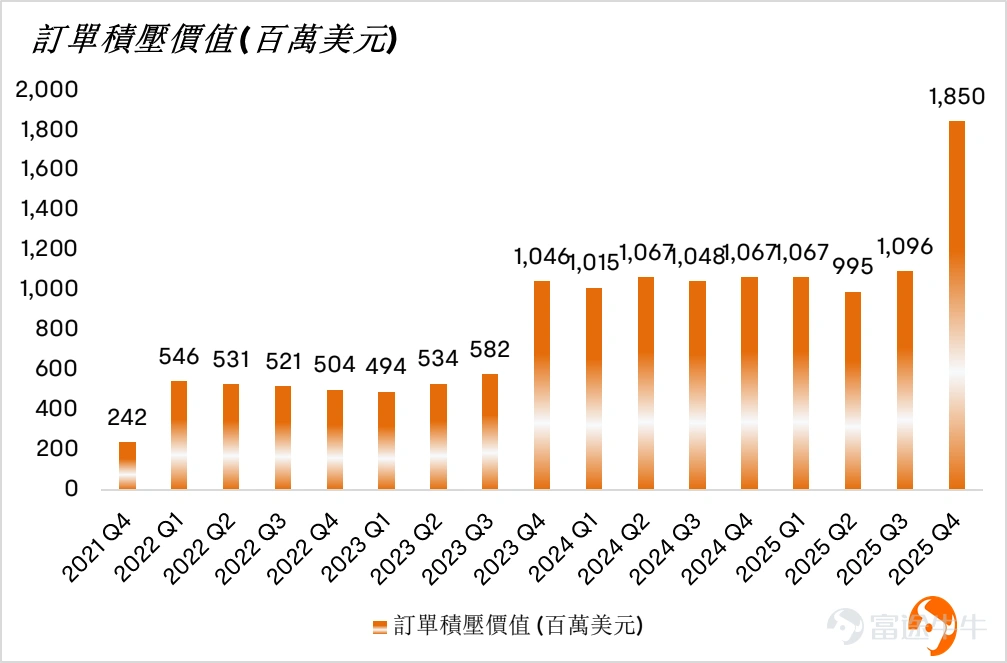

Additionally, order backlogs significantly increased, driven by orders from the Space Development Agency.

profit guidance.

The company forecasts Q1 2026 revenue to be between $185 million and $200 million, representing a 57% year-over-year growth based on the midpoint of the range, indicating an acceleration in revenue growth. Rocket Lab also expects the next quarter's GAAP gross margin to be 34%-36%, with non-GAAP gross margin at 39%-41%.

This gross margin guidance indicates a significant decline in the next quarter.

Management explained that this is due to the lower gross margin associated with large SDA projects, although operating margin and contribution margin remain high (as no additional significant R&D investment is required). Additionally, the gross margin of the Space Systems segment's component business experiences notable fluctuations, with non-GAAP gross margins varying between 30% and 70%, making long-term predictions difficult. Management noted that the gross margin is trending upward over the long term but may fluctuate quarterly depending on business mix. After the first launch of the Neutron rocket, its gross margin will follow a similar expansion curve as the Electron rocket—starting low or even negative initially but quickly turning profitable and approaching target gross margin levels as production scales up and processes are optimized. The company plans to disclose detailed gross margin data for both the Electron and Neutron rockets in the future to enhance transparency.

Overall, this Q4 earnings report was mixed. The Neutron rocket will directly impact whether Rocket Lab can narrow the gap with SpaceX in terms of carrying capacity. Furthermore, variables investors need to monitor going forward include the timing of revenue recognition for the Space Development Agency contract. Following the release of the earnings report, the stock price fell more than 5%.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

14

18