Anthropic launches enterprise AI plugin, could this mark a turning point for the software sector?

Salesforce: The narrative of AI replacing SaaS is gaining momentum, has the SaaS leader become a 'discarded piece'?

By Dolphin Research

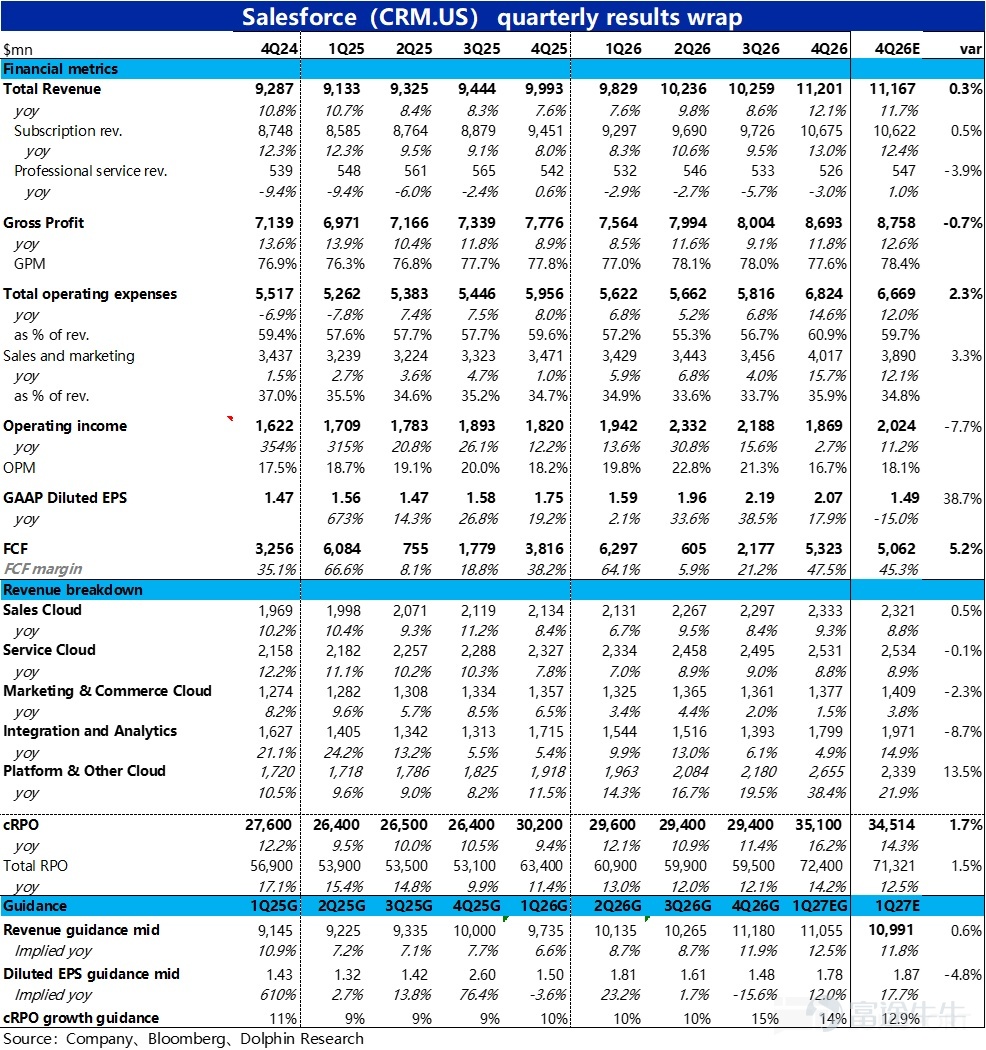

Recently, amidst the narrative of 'AI killing SaaS,' one of the hardest-hit sectors, CRM, released its Q4 2026 earnings report (as of January 31) during pre-market trading in the US this morning, showing overall mediocre performance.

Revenue growth did pick up slightly as expected, but this was primarily due to the impact of acquisitions and consolidation; underlying business growth remained weak. Gross margins continued to face pressure and declined further, while expenses across the board increased significantly, causing GAAP operating profit to underperform expectations considerably. Another key metric—cRPO short-term unfulfilled balance growth—also came in below buyer expectations, resulting in negative market feedback.

Specifically:

1. Growth appears to be accelerating, but in reality, it is still slowing: This quarterCore business--Subscription revenue grew by 13% year-over-year, or 11% when excluding currency benefits, marking an acceleration of 2 percentage points compared to the previous quarter.HoweverOf this, 4 percentage points of the growth were attributed to the consolidation of Informatica,Excluding this impact,the growth of the existing business has indeed slowed down.

Looking at different business lines,apart from the significant acceleration in platform cloud growth driven by the acquisition of Informatica, the growth of other business lines(in constant currency)has generally declined quarter-over-quarter, with the best outcome being flat performance.It is evident that although the company's previous guidance suggested revenue growth would bottom out and rebound, there has been little evidence of this as of this quarter.

AI-related revenue showed slight acceleration but remains in a very early stage: This quarter, the annualized revenue from Data & Agentforce reached $2.9 billion,of which approximately $1.1 billion came from consolidation effects. Excluding this impact, AI-related revenue grew 29% quarter-over-quarter, marking the fastest growth sincethe disclosure of this data.

Among this, the annualized revenue from Agentforce reached 800 million, a year-on-year increase of nearly 170%,The company's AI business growth has indeed seen a slight acceleration.But in terms of absolute scale,AI-related revenue accounts for less than 7% of total revenue, and if we only consider Agentforce, it is less than 2%.It is evident that customer adoption is still in a very early and trial stage; the so-called 'acceleration' is only relative to this small base.

3. The growth of leading indicators is also lackluster:Core metriccRPO (short-term unfulfilled balance) has seen its nominal growth rate rise sharply to 16%,which seems good at first glance.However, after excluding currency benefits, the actual year-on-year growth rate is 13%,Among which, similarly4 percentage points of the growth rate came from the contribution of consolidated financial statements.That is, after excluding this impact,the actual growth rate of the existing business cRPO slowed compared to the previous quarter.

Dolphin Intelligence learned that before the earnings report,the more optimistic buy-side expected a growth rate of 14% to 15%,the actual performance was somewhat disappointing for bullish investors. There were also no signs of acceleration.

4. Gross margin continues to decline under AI investment:The trend of gross margin pressure continued this quarter,with an overall gross margin of 77.6%, slightly lower both year-over-year and quarter-over-quarter, and below Bloomberg's expectation of 78.4%.

Just lookingLooking at the core subscription business this quarter, the gross margin was 82.4%, a sequential decline of about 0.5 percentage points and a contraction of nearly 1 percentage point year-over-year.Dolphin Group believes that this is likely due to the drag from AI-related businesses with high backend computing power requirements, such as Agentforce, which have relatively low gross margins.

5. The growth of expenses has明显提速.: While revenue growth remains lackluster,the year-over-year growth rate of total operating expenses this quarter surged to nearly 15%(for many years prior, it was only in the single digits %), higher than both market expectations and this quarter's revenue growth rate.

Specifically,The year-over-year increase in R&D, marketing, and administrative expenses was around 15%, indicating an across-the-board rise in investments.In the previous quarter, the company was still strictly controlling costs, but this quarter it has made a significant shift, suggesting that management’s intention to accelerate growth is quite evident.

6. Pressure on gross margins, rising costs, and poor profitability:Flat growth, shrinking gross margins, but significantly higher costs,The result isThis quarter's GAAP operating margin was 16.7%, narrowing by 1.5 percentage points year-over-year, the first decline since fiscal year 23(i.e., the post-pandemic low in calendar year 22).

This resulted in a profit of $1.87 billion, up less than 3% year-over-year, and nearly 8% below Bloomberg consensus, leaving a very poor impression. Excluding non-cash expenses (mainly share-based compensation expenses and changes in operating assets), the company focuses more onfree cash flow profit, which this quarter reached $5.32 billion, surpassing both expectations and previous guidance.The discrepancy between the two metrics, one positive and one negative, is mainly due to the recognition of a significant amount of advance payments on the balance sheet.

7. Shareholder returns show strong commitment:As promised at the recent Dreamforce conference, once the company's growth becomes limited, returning value to shareholders has become one of the main ways to maintain its appeal to equity investors.For the entire fiscal year 26, the company spent a total of $14.3 billion on shareholder returns., the vast majority of which was through buybacks.The company's current market value corresponds to an 8% return rate., which is quite impressive.

AdditionallyThe company also announced a new buyback authorization of up to 50 billion.(Replacing the previous buyback authorization). The company has been quite generous in terms of shareholder returns.

Dolphin Research's view:

1. As analyzed above, Salesforce's performance this quarter was clearly not good. Excluding the benefits from consolidation and exchange rates,the growth of the company's existing business did not accelerate but continued to slow down.The management’s guidance for a rebound in revenue at the start of the year has not materialized this quarter. (Including the benefits from exchange rates and consolidation, total revenue growth did recover to over 10%, but this is not particularly meaningful.)

Although after more than a year of promotion and iteration, Agentforce and otherAI-related businesses are indeed experiencing accelerating revenue growth, but this is still negligible compared to the overall base and has little substantial impact on boosting total revenue growth.

Meanwhile, due to the higher costs associated with AI-related businesses and the significant increase in investment (whether aimed at further accelerating revenue or as a defensive measure against perceived AI replacement threats), profitability has also suffered.

The overall impression is that growth was mediocre and profits were also lackluster.

As for the subsequent guidance and outlook:

In the short-term outlook,Under constant currency, total revenue for the next quarter is expected to grow by 10%~11% year-over-year, similar to this quarter with a slight improvement. The contribution from acquisitions remains at 4 percentage points, roughly in line with Bloomberg's expectations. This indicates a slight improvement over this quarter but also suggests no significant acceleration in the core business.

The guidance for cPRO’s year-over-year growth rate stands at 13% (under constant currency), unchanged from this quarter. Although it did not disclose how much of this growth came from acquisitions, there is clearly no acceleration either.

In terms of profitability, the guided diluted EPS was about 5% below Bloomberg’s expectations. Though on a Non-GAAP basis, the results slightly exceeded expectations. However, unlike the market consensus, Dolphin Analytics generally disagrees with the notion that stock-based compensation should not be considered an expense. Therefore, under GAAP standards, the performance still does not look good.

Overall,This means that growth in the next quarter will remain stable, with no significant acceleration, while profit margins will continue to be under pressure.

However, as Openclaw has shown the market that AI Agents are evolving and maturing faster than anticipated, top-tier large models like Claude and Gemini have also been accelerating their iterations recently. At present,the narrative around 'how AI will change/revolutionize software and even all industries' has a greater impact on share prices than actual performance results.

To be honest, Dolphin Analytics believes that: a. Existing software giants possess sufficient industry 'know-how' and proprietary data, allowing them to maintain a leading position in the AI era, turning AI into an advantage rather than a competitor;

b. AI will significantly reduce the cost for companies to develop internal tools and achieve office automation, making 'expensive' SaaS services lose competitiveness. Alternatively, as Agents replace employees, the number of chargeable seats (Seats) for SaaS could drop substantially. These are just some scenarios that could seriously damage the profitability of SaaS companies.

Of the two drastically different scenarios above, which one is more likely remains an unanswered question at present. The only certainty is the high level of uncertainty. And uncertainty means risk, a risk that will likely amplify further with the evolution of AI.

Thus, similar to Dolphin's previous view on Uber. On one hand, the company’s current performance remains relatively stable, showing no obvious signs of being significantly impacted by AI. However,given the possibility of being completely disrupted with a 'go-to-zero' outcome, Dolphin still prefers to maintain a wait-and-see attitude in the short to medium term. As the saying goes, 'A prudent man avoids danger.'

3. Overall, unlike other SaaS targets, even if AI does not truly disrupt them later on, overvalued SaaS stocks inherently have significant downside potential. Salesforce, which is already mature, has the advantage of not being highly valued, leaving limited room for further pure valuation declines, especially given strong buyback support.

Therefore, existing investors need not overly worry about the risk of further sharp declines. However, on the flip side, it’s currently unclear what upward momentum may emerge.

Below are the core financial charts and a brief overview of operations:

1. Brief Introduction to Salesforce's Business & Revenue

Salesforce is a pioneer in the CRM industry (Client Relationship Management) across the US and globally, being the first to propose the SaaS concept, or software-as-a-service. The key feature of this model is the use of cloud-based services rather than on-premise deployment, and subscription-based payments instead of perpetual licensing.

Therefore, Salesforce’s business and revenue structure primarily consists of two main categories: ①Over 95% of its revenue comes from various types of SaaS service subscriptions.;② The remaining approximately 5% is comprised of expert service income derived from activities such as project consulting and product training.。

A closer look reveals that the predominant component isSubscription revenue consists of five key categories of SaaS services.with each segment contributing roughly equal revenue volumes.,Includes:

① Sales Cloud:CRM, the most central and earliest business of the company, primarily includes process management tools for various stages of enterprise sales, such as client contact, quotations, and closing deals.

② Service Cloud: Another core business line, mainly including various functions related to customer service, such as customer information management and online customer support.

③ Marketing & Commerce Cloud: Among these, Marketing Cloud refers to the functionality of conducting marketing systematically through various channels such as search, social media, and email; Commerce Cloud mainly includes functions required for e-commerce, such as virtual mall construction, order management, payment processing, etc.

④ Data & Sharing (Integration & Analytics):Salesforce's integrated internal database services and business analytics tools are mainly composed of MuleSoft and Tableau.

⑤ Platform Cloud (Platform & Others):The infrastructure and services on which other Salesforce SaaS offerings rely, similar to PaaS (Platform-as-a-Service), also include team collaboration SaaS services like Slack, akin to Microsoft Teams.

Second, revenue growth appears to be accelerating, but in reality, it is average.

Second, leading indicators show a similar trend, appearing strong but slightly below expectations.

Third, gross margin is under pressure and declining.

Fourth, expenses have significantly increased.

Fifth, profits have seen almost no growth.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

1