Inflation surprise heats up! US January PPI accelerates beyond expectations

Global Weekly Review | US Q4 GDP Misses Expectations, China's January Aggregate Financing Up YoY

United States: Q4 GDP Misses Expectations, Core PCE Exceeds Expectations, Tariff Policy Faces Setbacks

Last week, the US focused on Q4 GDP, core PCE, and tariff policy.Q4 real GDP annualized quarterly growth rate was 1.4%, far below the expected 2.8%,a significant drop from 4.4% in Q3, with the government shutdown dragging GDP by about 1 percentage point; full-year 2025 GDP growth at 2.2%, slightly below 2024. Structurally, personal consumption and AI-related investments provided support, partially offsetting negative impacts. December core PCE month-over-month at 0.4% exceeded expectations, leading to a slight pullback in Fed rate cut expectations.On tariffs, the US Supreme Court ruled 6-3 that Trump's tariffs implemented under the International Emergency Economic Powers Act were illegal,Trump signed an executive order on the same day terminating the tariff measures under that law, potentially requiring refunds of over $175 billion in previously collected tariffs. Subsequently, Trump first announced a 10% tariff on global goods for 150 days under Section 122 of the Trade Act of 1974 as a replacement for the illegal tariffs,then on the 21st announced an increase in the 'global import tariff' rate from 10% to 15%, effective immediately,while indicating that new legal tariff measures would be announced in the coming months, and existing US national security-related and specific trade law tariffs would remain in effect.

China: January social financing increased year-over-year, financial data highlights policy efforts, credit demand remains differentiated

China's January social financing scale increased year-on-year, with government bond financing becoming the main supportMonetary policy continues to be moderately loose, but credit demand in the real economy remains differentiatedJanuary's social financing scale increase was 7.22 trillion yuan, a year-on-year increase of 166.2 billion yuan, with the stock of social financing growing by 8.2% year-on-year; government bond financing saw a significant year-on-year increase, accounting for 13.5% of the social financing increase, reaching a new high for the same period since 2021. In terms of money supply, M2 grew by 9.0% year-on-year, with the growth rate rebounding from the previous month, mainly driven by the base effect and capital market trendsOn the loan side, the RMB loan balance grew by 6.1% year-on-yearInclusive small and micro-enterprises, as well as medium- and long-term loans in the service sector, grew faster than the overall level, but RMB loans saw a year-on-year decrease. The reduction in medium- and long-term loans to enterprises reflects insufficient investment confidence, while the increase in household loans was mainly due to pre-Spring Festival consumption and interest rate cuts, with mortgage demand remaining sluggishSubsequent fiscal and monetary policies will continue to take effect, supporting a stable economic start

[Market Performance]

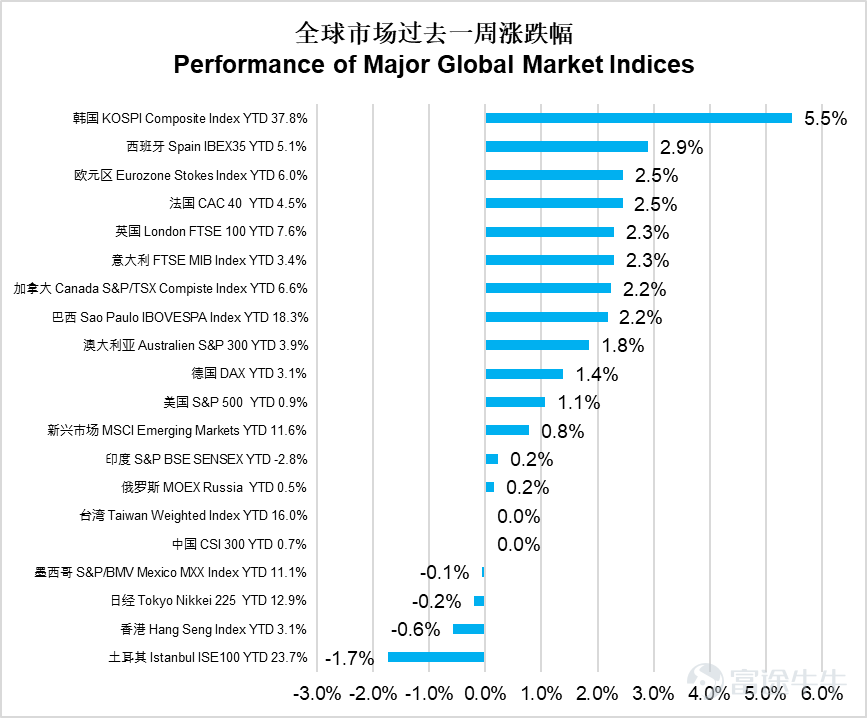

Global markets generally rose over the past week, with South Korea’s KOSPI index leading the way with a 5.5% surgeSpain’s IBEX35 rose 2.9%, while the Eurozone STOXX and France’s CAC40 both gained 2.5%. Emerging markets overall rose by 0.8%, with Brazil’s IBOVESPA gaining 2.2%. Turkey’s ISE100 fell 1.7%, performing the worstThe Hang Seng Index fell 0.6%, while the Nikkei 225 edged down 0.2%The US S&P 500 rose by 1.1%. The Chinese market was closed for the Lunar New Year holiday.Overall, the European and South Korean markets performed exceptionally well.

Data source: Wind

The US communication services sector rose by 2.3%, making it the top-performing sector, while both the industrial and consumer discretionary sectors increased by 1.7%.Both the information technology and financial sectors rose by 1.5%. The energy sector increased by 0.5%, and real estate remained flat. However, the consumer staples sector fell by 2.3%, healthcare dropped by 0.6%, utilities declined by 0.5%, and the materials sector edged down by 0.3%. The market exhibited a divergence, with communication services leading gains and defensive sectors under pressure.

Data source: Wind

The Hong Kong energy sector rose by 3.9%, making it the best performer, while the raw materials industry climbed by 3.0%.The industrial sector rose by 1.3%. Healthcare gained 0.9%, telecommunications increased by 0.5%, and both finance and utilities rose by 0.3%. Real estate and construction inched up by 0.1%. However, non-essential consumption fell by 3.0%, the Hang Seng Tech Index dropped by 2.8%, and the information technology sector declined by 2.2%. Consumer staples fell by 1.3%, and conglomerates dropped by 0.4%. The market showed a pattern of energy and raw materials leading gains, while technology and consumption led declines.

Data source: Wind

[Market Outlook]

Although the US Supreme Court ruled that Trump had no authority to impose reciprocal tariffs through the International Emergency Economic Powers Act (IEEPA), the market had already fully anticipated this outcome. In our previous weekly review, we had presciently judged that even if the Supreme Court's decision went against Trump, he could still use other acts to achieve the purpose of imposing tariffs. As of the latest news, Trump quickly announced that he would invoke Section 122 to impose a temporary 10% tariff globally starting on the 24th of this month, subsequently announcing an increase to 15%. This provision has a maximum duration of 150 days, during which it is expected that measures such as Section 301 will be used to initiate investigations against relevant countries, ultimately aiming to impose additional tariffs on countries contributing to the US trade deficit. For the capital markets, the issue of how to handle approximately $175 billion in tariffs collected since 2025 remains unresolved. The Supreme Court’s ruling did not address this portion. Since November 2025, we have observed numerous US companies filing lawsuits against the US government's imposition of tariffs in international trade courts, with over a thousand cases currently pending. The market currently expects that the tax refund process may last several years, with the final refund amount potentially approaching half of the current collected amount. This scenario is expected to have limited short-term market impact. Additionally, for countries that had previously reached trade agreements with the US, particularly those with tariff rates above 15% (such as India and Southeast Asian nations), whether they will seize this opportunity to initiate new trade negotiations with the US also warrants close attention. In summary, the market has reacted relatively calmly to the events that have occurred thus far. The unresolved issues are likely to be one of the key factors influencing market trends in the near term.

Key economic data releases next week:

The US will release December durable goods orders data on Monday;

China will announce the LPR interest rate on Tuesday;

The US will release January PPI data on Friday.

Disclaimer: The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Investment involves risks, and fund prices can rise or fall. Past performance is not indicative of future results. Before investing, investors should carefully read the fund prospectus (including the “Risk Factors” section) to understand the investment risks associated with the fund. This report may only be distributed within certain jurisdictions. In any jurisdiction where the distribution of such information or making of any invitation or recommendation is prohibited, or if distributing this report or making an invitation or recommendation to any person would be illegal, this report does not constitute such distribution, invitation, or recommendation. This document has been exempted from prior review and approval by the Hong Kong Securities and Futures Commission (SFC), and has not been reviewed by the SFC. SFC recognition does not imply a recommendation or endorsement of the scheme, nor does it guarantee the commercial merits or performance of the scheme, nor does it represent that the scheme is suitable for all investors, or endorse its suitability for any particular investor or category of investors. All rights reserved.©️ 2026. E Fund Asset Management (Hong Kong) Co., Ltd.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

5

1