Jinxing Brewery's Push for a Hong Kong IPO: Surprise Dividends Exceed USD 42 Million, Enriching Zhang Tieshan and Zhang Feng Father-Son Duo

Recently, Henan Jinxing Brewery Co., Ltd. (hereinafter referred to as 'Jinxing Brewery') submitted an IPO application to the Hong Kong Stock Exchange, officially kicking off its listing process in Hong Kong.

In the long-term competition within the beer industry, the key lies in winning frequent repurchases from consumers, securing continuous channel support, capturing shelf space at retail outlets, while strictly maintaining a balance between cost and quality. Weakness in any aspect will quickly impact financial performance.

It is against this backdrop that the series of operations undertaken by Golden Star Brewery prior to its IPO have drawn attention, especially the frequent dividend payouts, which can be described as a 'fire-sale style dividend.' The prospectus reveals that Golden Star Brewery announced dividend distributions three times in 2025, totaling over 300 million yuan.

Specifically, Golden Star Brewery announced and paid out a cash dividend of 102 million yuan in March 2025, declared another 127 million yuan dividend in May 2025 which was paid in June 2025, and announced an additional 100 million yuan dividend in October 2025. As of September 30, 2025, the total amount of dividends paid reached 229 million yuan.

In terms of equity structure, the bulk of the large-scale dividend payout flows to Zhang Tieshan and his son Zhang Feng. Zhang Tieshan holds 9.94% of shares, while Zhang Feng holds 8.95%. Together, they control 74.56% of the shares via Golden Star Holdings, bringing their combined stake to approximately 93.45%. Currently, Zhang Tieshan serves as Chairman of Golden Star Brewery, with his son Zhang Feng acting as General Manager.

This push for an IPO has led many to view Chinese craft beer as the core driver of growth for Golden Star Brewery. However, the high dividend payouts before the listing, along with the rapid shift in business focus, also highlight potential challenges in the brewery's current growth trajectory. While heavily relying on the high margins from Chinese craft beer supports short-term profits, long-term development remains uncertain.

I. Chinese Craft Beer Shifts from Growth Driver to Core Focus

In the beer industry, what truly determines valuation flexibility is not just selling beer but rather what kind of beer is being sold and how it is priced. Chinese craft beer is at the heart of what is propelling Golden Star Brewery forward.

According to the prospectus, Golden Star Brewery reported no revenue from its Chinese craft beer category in 2023, but by 2024, this category accounted for 51.7% of revenue. By the first nine months of 2024 (i.e., the first three quarters), this figure stood at 9.3%, rising to 78.1% in the first three quarters of 2025.

Source: Jinxing Beer Prospectus

This is no longer merely about launching new products; it reflects a wholesale shift in the company's operational focus. Behind the rapidly increasing figures lies a significant transformation of Chinese craft beer from a niche offering to a core strategy. The sharp rise in revenue contribution has primarily rewritten Golden Star Brewery’s gross margin landscape. By product category, during the first three quarters of 2025, the gross margin for Chinese craft beer was 52.0%, compared to 33.1% for '1982,' 22.6% for 'New Generation,' 26.8% for 'Pure Draft,' and 35.4% for 'Other Beers.'

Source: Jinxing Beer Prospectus

When high-margin products become the primary source of revenue, the quality of profitability becomes paramount, and companies should leverage brand premium to secure greater growth potential. As the center of revenue shifts, the role hierarchy of Golden Star Beer's product lineup has also been rewritten. For instance, in the first three quarters of 2025, Chinese craft beer accounted for 78.1% of total revenue, '1982' for 11.5%, 'New Generation' for 5.1%, 'Pure Draft' for 3.0%, and 'other beers' for 1.2%. The significance of these figures does not lie in old products being subpar, but rather where the company allocates resources. When a new product surges to account for 78.1% of revenue, will other products be marginalized? Will corporate growth increasingly rely on the performance of Chinese craft beer? These are questions worth considering.

And challenges lurk as well. The rapid rise of Chinese craft beer's share ties operational volatility closely to the market performance of this new product. According to the prospectus, the product displayed significant fluctuations across different periods: it was at 9.3% in the first three quarters of 2024, and then surged to 78.1% in the same period of 2025. This means that whether Chinese craft beer can stabilize is not just a growth issue. If there are changes in demand, channel progress, or supply-side fluctuations, the revenue structure could be reshuffled.

More crucially, once Chinese craft beer takes center stage, whether other products can still play roles in diversifying revenue streams and serving as defensive moats becomes another key question. In 2023, before the launch or mass adoption of Chinese craft beer, '1982' accounted for 42.2% of revenue, 'New Generation' for 36.1%, 'Pure Draft' for 11.0%, and 'other beers' for 9.2%. At this stage, revenue was more evenly distributed across multiple sources.

Once Chinese craft beer becomes the main driver, the company gains a more prominent growth engine, but it also faces the buffering effect of a multi-product portfolio. Any changes in taste preference, repurchase rates, or channel sales could lead to earnings volatility. The high margins brought by Chinese craft beer—whether driven by pricing power or temporary product mix tilts—can indicate trends via the gross margin structure in the prospectus, though no direct answers are provided.

Second, channels determine the upper limit of growth, and distribution remains the backbone.

Channels define the boundaries of growth and significantly affect a brand’s control over pricing and end-user experience.

For Chinese craft beer aiming to enhance premium positioning, the channel model is especially critical. From the sales network perspective, Golden Star Beer’s revenue still primarily comes from distribution. In 2023, distribution accounted for 97.6% of revenue, 89.4% in 2024, and 94.8% in the first three quarters of 2025. Meanwhile, direct sales accounted for 9.4% in 2024 and fell to 4.1% in the first three quarters of 2025. This data clearly shows that direct sales have not consistently increased, and distribution remains the backbone of Golden Star Beer’s shipments.

Source: Jin Xing Beer Prospectus

The variable here is that, based on industry common sense, Chinese craft beer generally emphasizes branding, pricing, and consumer experience, which are key to enhancing premium value. However, relying heavily on distribution may mean that terminal reach, display resources, and sales momentum depend more on the willingness and capability of the sales network. While the distribution model can scale up operations, ensuring consistent brand messaging and consumer experience poses a greater challenge for businesses.

Furthermore, regarding the percentage of offline distribution revenue relative to total revenue, the prospectus shows that it was 87.6% in 2023, 81.0% in 2024, and 78.1% in the first three quarters of 2025. When Chinese craft beer needs to communicate its premium pricing through effective branding, online channels often hold an advantage in terms of expression and outreach. However, Golden Star Beer’s current growth still mainly relies on offline expansion, making it one of the company’s key priorities to quickly bolster its online sales network.

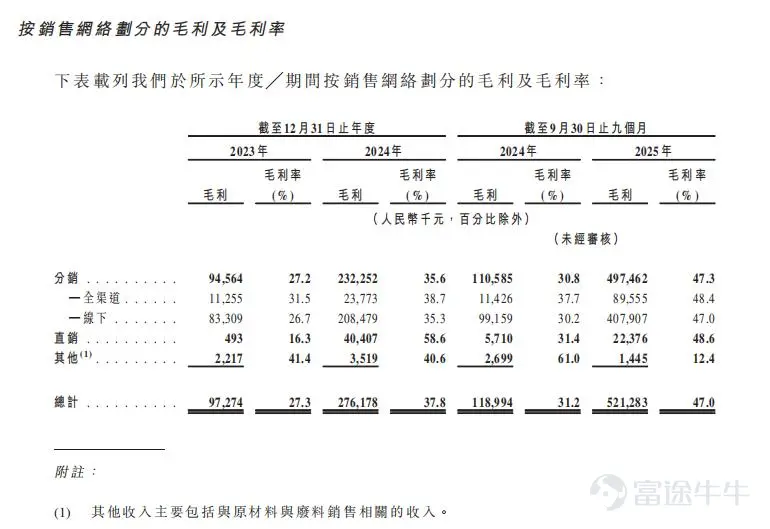

Who exactly takes the gross profit is another more realistic variable brought by the current sales network structure for Golden Star Beer. By sales network, its distribution gross margin was 27.2% in 2023, 35.6% in 2024, 30.8% in the first three quarters of 2024, and 47.3% in the first three quarters of 2025.

Source: Jinxing Beer Prospectus

The prospectus shows that in the first three quarters of 2025, the direct sales gross margin was 48.6%, slightly higher than the distribution gross margin of 47.3%, but direct sales revenue accounted for only 4.1%. If higher margins are mainly from direct sales scenarios, then with distribution still dominating, whether Golden Star Beer's high margin for Chinese craft beer can be maintained at a larger scale remains a question.

Looking further at channel concentration, revenue contributed by the top five customers accounted for 10.9% in 2023, 6.5% in 2024, and 6.2% in the first three quarters of 2025. The largest customer’s revenue share was 2.8% in 2023, 1.7% in 2024, and 2.4% in the first three quarters of 2025. This indicates that the distribution network does not rely heavily on a few customers, showing stronger resilience against fluctuations from any single customer, which aligns with the beer industry’s common practice of multi-point networking.

However, one issue is that having non-concentrated customers does not necessarily mean stronger channel control. On the contrary, when channels are highly fragmented, companies need stronger terminal execution and brand coordination to maintain consistent pricing discipline and consumer experience across different cities, terminals, and consumption scenarios. With distribution still accounting for 94.8%, achieving such consistency cannot solely rely on willingness to cooperate; it may test Golden Star Beer’s channel management and collaboration abilities even more. In short, while Chinese craft beer needs to establish a perception of 'worthiness,' the distribution network focuses more on 'volume.' Coexistence of both requires higher operational capability to ensure product value is not diluted during scale expansion.

III. Cost and Development Challenges under High Profit Margins

Among Golden Star Beer's key financial ratios, the gross margin was 27.3% in 2023, 37.8% in 2024, and 47.0% in the first three quarters of 2025. Net profit margins were 3.4% in 2023, 17.2% in 2024, and 27.5% in the first three quarters of 2025.

Source: Jinxing Beer Prospectus

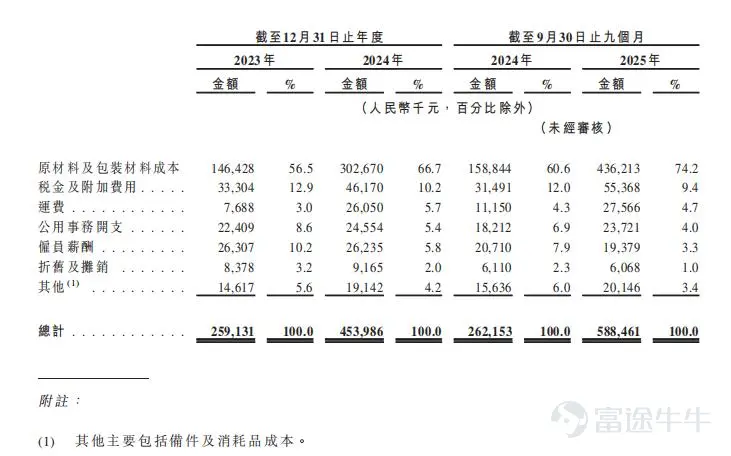

These figures are impressive but also nerve-wracking because the jump in net profit margin from 3.4% to 27.5% suggests significant changes in operating conditions. What will sustain this change and whether this level of profitability can remain stable over a longer period is uncertain. Costs are also shifting, directly impacting profits. Analyzing the composition of sales costs, raw material and packaging costs accounted for 56.5% in 2023, 66.7% in 2024, 60.6% in the first three quarters of 2024, and 74.2% in the first three quarters of 2025. When raw materials and packaging reach 74.2% of total costs, supply chain stability, packaging price volatility, and raw material quality consistency become crucial operational variables, as they are no longer 'minor costs' but the main cost drivers.

Source: Jin Xing Beer Prospectus

The concentration on the supply side has, to a certain extent, reduced single-source risk. According to the prospectus, the procurement proportion of its top five suppliers was 37.8% in 2023, 33.4% in 2024, and 31.7% in the first three quarters of 2025. Among them, the procurement share of the largest supplier was 10.6% in 2023, 11.8% in 2024, and 9.4% in the first three quarters of 2025. A decline in supplier concentration typically makes procurement more flexible and aligns better with the risk preferences of scaled operations. However, it is also important to see the other side: when products rely more on consistent flavor and texture, does having more suppliers mean greater stability? The key lies in whether quality standards can be uniformly enforced.

As for capacity utilization, it serves as more of a footnote to whether the supply side can keep up. Significant differences are evident in capacity utilization rates across different years and periods at Jinxing Beer's main production bases. For instance, the Zhengzhou base had a rate of 45% in 2023, 65% in 2024, and 76% in the first three quarters of 2025.

Image source: Jin Xing Beer prospectus

When Chinese craft beer accounts for 78.1%, the task on the supply side is not just about 'making more' but rather 'making things consistently.' Rising capacity utilization usually indicates better economies of scale. However, this also implies higher requirements for process, quality control, and supply chain coordination. If consistency issues arise, the brand and premium pricing will be the first to suffer.

Notably, another set of data highlights a dramatic shift in Jinxing Beer's financial status. The debt-to-equity ratio, calculated by dividing total interest-bearing bank loans by total equity, stood at 2250.0% in 2023, 98.7% in 2024, and 11.1% in the first three quarters of 2025. As the ratio of interest-bearing bank loans to total equity rapidly declines, scrutiny over profit sources and sustainability inevitably intensifies.

Such changes, while not uncommon among companies rushing toward an IPO, amplify external attention on the 'quality of profits.' As the debt-to-equity ratio drops quickly and financial flexibility improves, the company may find it easier to gain investor patience. However, this also raises a practical question: Can future growth maintain stable profitability, or will expansion and competition erode margins? The foundation for sustained profit growth hinges on maintaining a stable product mix, channel discipline, and supply consistency. Any deviation in these three areas could cause high net margins to retreat.

Conclusion

The high gross margin of Chinese craft beer indeed paints an attractive financial picture for Jinxing Beer, but this growth comes at a cost. Behind higher pricing lies a corresponding upgrade in cost structure. From raw material procurement and brewing techniques to channel maintenance and brand building, each link requires ongoing capital investment. High gross margin is the result, but sustaining it demands equal or even greater cost resilience.

Data from the prospectus shows that Chinese craft beer has become a new pillar driving Jinxing Beer’s growth. However, this growth did not emerge out of thin air; instead, as the proportion of Chinese craft beer increased, revenue contributions from other categories declined. Both the classic unfiltered series and the once-popular 'next-generation beer' saw significant drops in their revenue share. This indicates a profound shift in growth structure rather than across-the-board expansion.

As Chinese craft beer becomes the core of operations, the real challenge for Jinxing Beer in its IPO push is whether it can maintain product pricing and premium under larger-scale, more complex channels and stricter cost constraints while also winning favorable valuation and value recognition from investors. This is the key proof needed for the company’s listing ambitions.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment