Tech giants boost Capex again! What's the outlook for future stock prices?

Amazon Earnings Preview: Will AWS Growth Acceleration Outweigh Free Cash Flow Concerns?

$Amazon (AMZN.US)$Amazon will announce its Q4 2025 financial results after the US stock market closes on February 5.

Core Financial Indicators

– Market expectations for Amazon’s Q4 2025 revenue stand at $211.23 billion, representing a year-over-year growth of 12.48%. The company previously guided Q4 revenue between $206 billion and $213 billion, implying a year-over-year growth rate of 9.7% to 13.4%.

– Earnings per share are projected to be $1.96, reflecting a 5.35% increase year over year.

– In terms of profitability, Amazon previously forecasted Q4 operating profit to range from $21 billion to $26 billion. Typically, Amazon's operating profit tends to be closer to the upper limit, which implies a growth rate of 22.6%.

Three key areas of focus

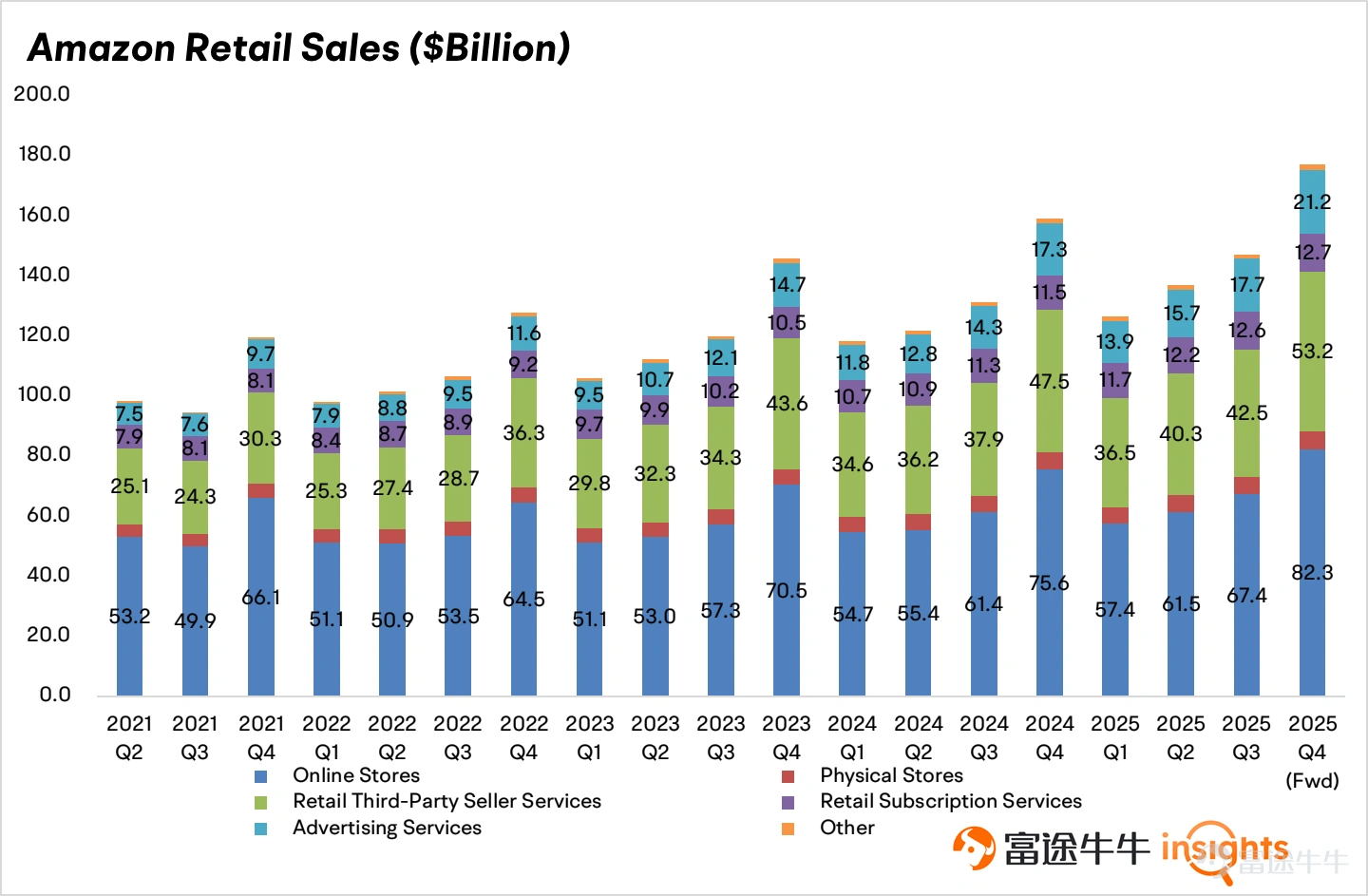

Global Retail Business

In the previous quarter, Amazon's North America retail business grew by 11%, while other regions saw a 14% increase. Last year, Amazon continued enhancing its same-day delivery capabilities, expanded its grocery category, and increased geographic coverage for deliveries. These efforts are expected to further boost Amazon’s e-commerce penetration in the US retail market.

Advertising represents another rapidly growing segment for Amazon, with quarterly revenues maintaining a growth rate of over 20%. Meta’s Q4 performance highlighted strong demand for online advertising, which will benefit Amazon's e-commerce and streaming advertising businesses as well.

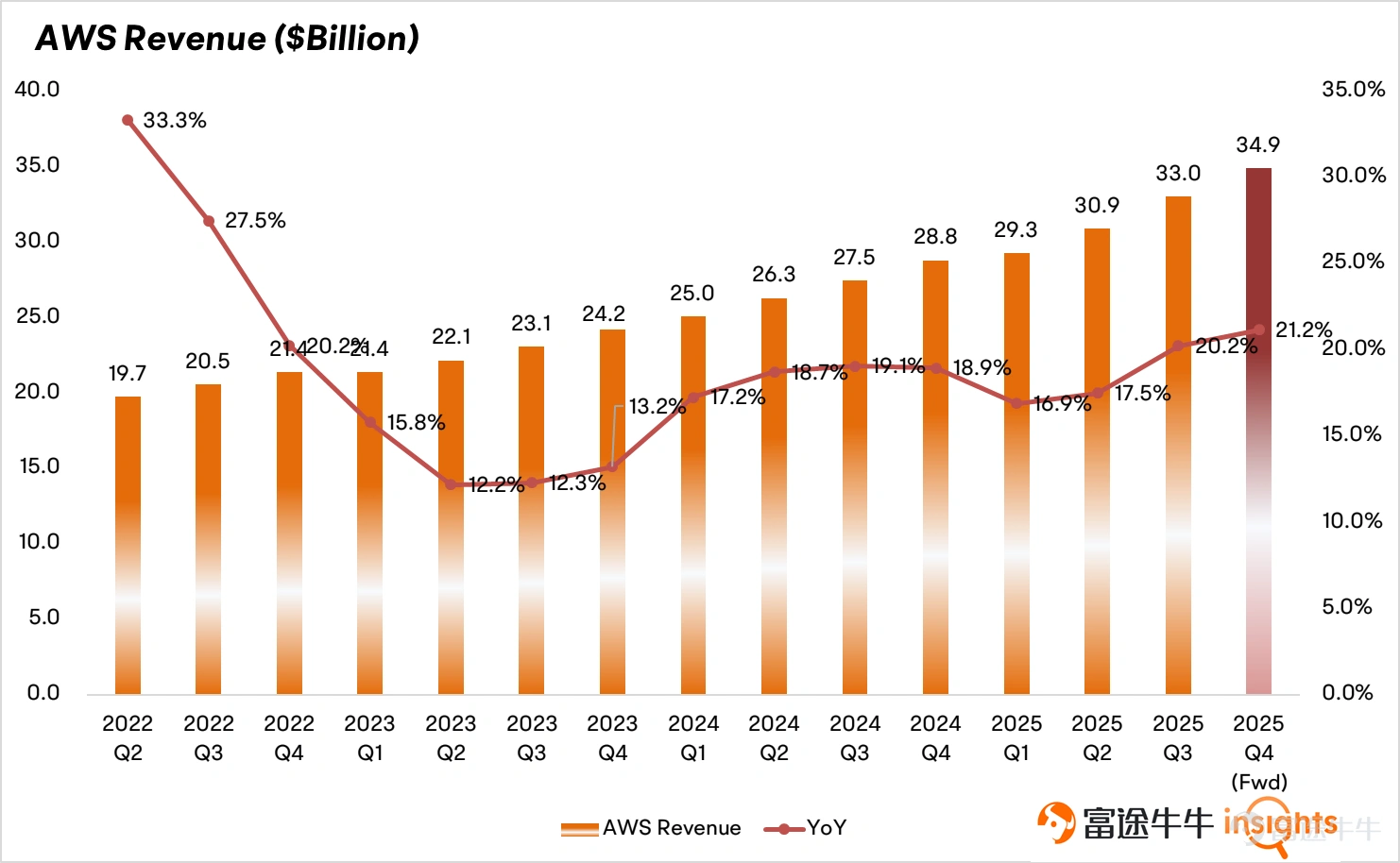

AWS Cloud Services

During the Q3 2025 earnings call, Amazon stated that its AWS cloud service capacity is 'expected to double from the Q3 2025 level by 2027,' marking a notable shift from previous quarters where supply constraints persisted. During the Q3 2025 conference call, management also noted that artificial intelligence demand continues to outpace supply, stating, 'We can currently convert new data center capacity into revenue immediately upon deployment.' The market generally expects AWS revenue to grow slightly above 20%; however, investors should remain cautious about potential margin pressure on the cloud business.

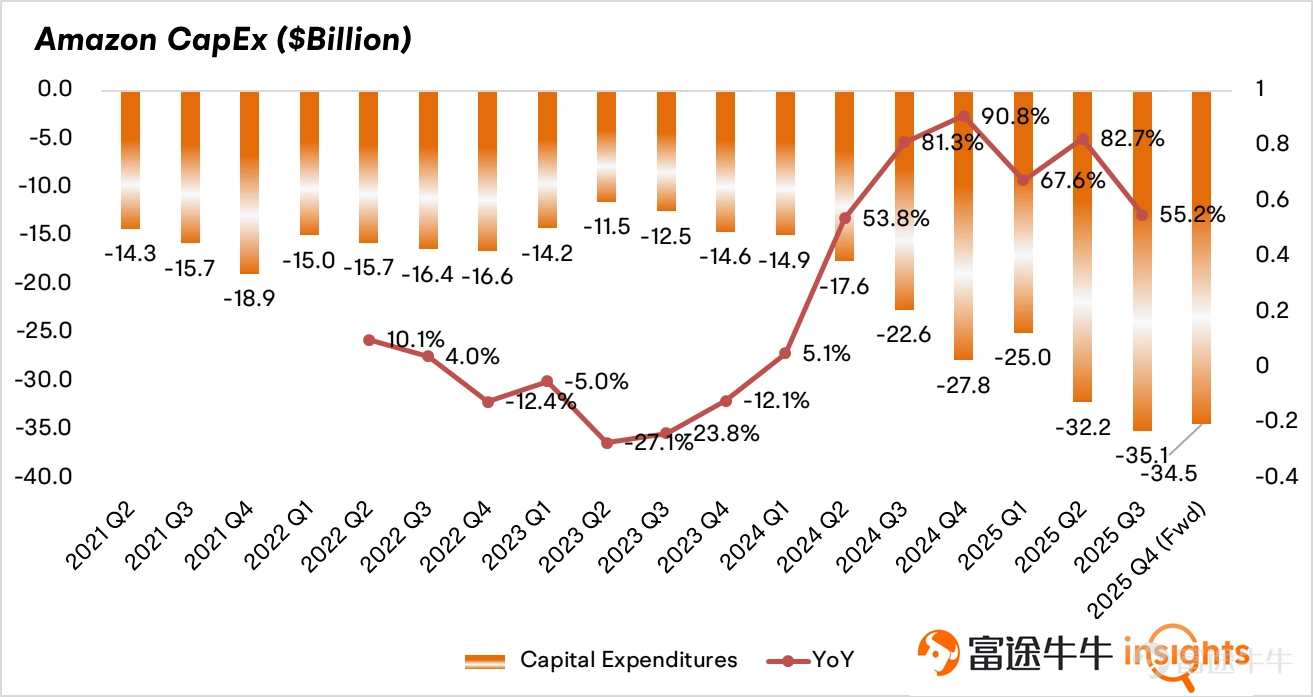

Capital expenditures

Amazon's capital expenditure in the third quarter of 2025 increased by 55.2%. The market had previously adjusted downward the shipment volume of Amazon’s Trainium chips, the second largest player in the ASIC industry, for 2026 based on Taiwan Semiconductor’s capacity arrangements. As a result, Amazon will have to rely more heavily on external suppliers like NVIDIA for AI chips, further constraining its free cash flow.

Options market signals

The put/call ratio for Amazon options is currently at 0.72, lower than the level during the previous earnings season, indicating a weakening of bearish momentum. Implied volatility (IV) data shows a volatility of 46.74%. On the first trading day after past earnings announcements, the stock price has averaged a fluctuation of 6.22%.

Catalysts & Risk Warnings

- Potential positive factors: Recovery in the advertising industry; Strong demand for cloud services

- Risks to watch: Macroeconomic slowdown

- Valuation: Amazon’s price-to-earnings ratio is 33.7 times, standing at the 39th percentile of its historical range over the past five years.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

14

14