[2026 Outlook] Plan Ahead! Share the Investment Opportunities You Are Optimistic About

Eastspring's View: The Investment Value of Japan Amid a Stronger Yen and Rising Yields (Part 2)

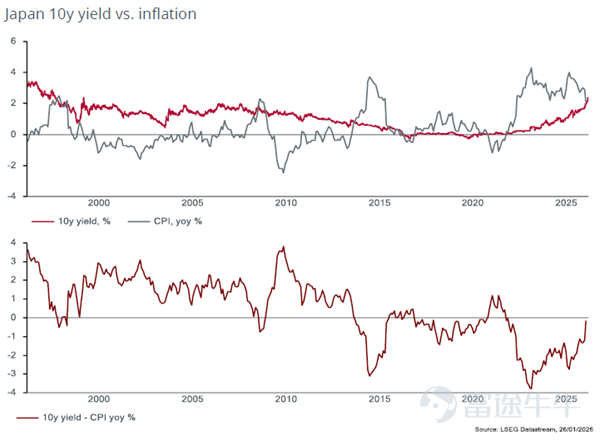

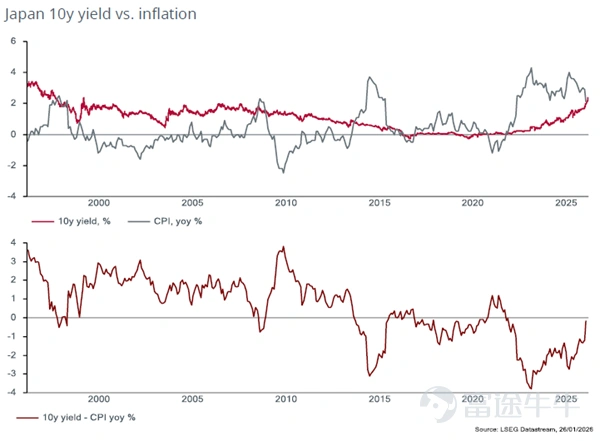

So, what about the rise in Japanese government bond yields? As we pointed out in November last year, we believe that Japanese bond yields still have room to rise further, and we maintain this view. However, compared to many investors in the market, we are less concerned about the impact of higher yields.

As we noted last year, we believe the rise in long-term bond yields is a necessary adjustment by the market to Japan’s inflation returning to higher levels.

The chart below shows that prior to the Bank of Japan's large-scale and sustained purchases of Japanese government bonds (JGBs) starting in April 2013, JGB yields were close to current levels and about 1%-2% above inflation. We expect Japan’s inflation to be around 2% this year, with the Bank of Japan raising the policy rate by 50 basis points to 1.25%, and the 10-year JGB yield rising to near 2.8%.

Nevertheless, the chart below shows that Japanese equities are rising in tandem with government bond yields. This is because rising yields reflect a recovery in Japan’s nominal GDP growth and improved corporate profitability.

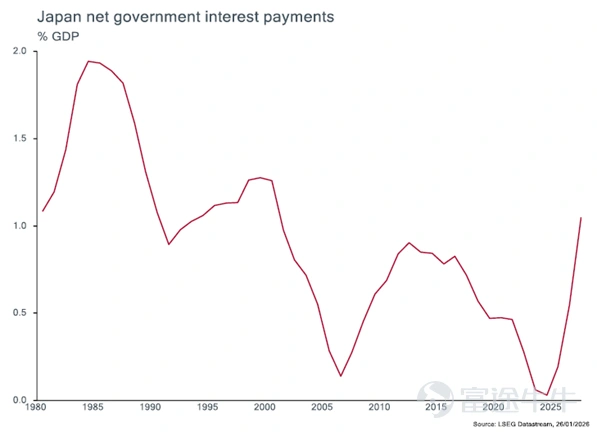

We also disagree with concerns held by some that rising yields could trigger a fiscal crisis in Japan. First, the government’s net interest expenditure as a percentage of GDP remains far below the peak levels seen in the early 1980s (see chart below).

Second, Japan’s primary deficit (fiscal balance excluding interest payments) has narrowed significantly over the past few years, markedly improving long-term fiscal sustainability. More critically, the budget for fiscal year 2026 passed by the Koike Cabinet will bring Japan its first narrow primary surplus in 28 years, keeping new bond issuance below 30 trillion yen for the second consecutive year, while reducing the bond dependency ratio to 24.2%, the lowest level in more than a decade.

The result of faster nominal GDP growth and a shrinking primary deficit is that Japan’s public debt-to-GDP ratio (both gross and net) has declined by 37 percentage points and 51 percentage points respectively since its peak in 2000. We expect the debt-to-GDP ratio to continue to gradually decline in the coming years.

Japan Equity Team's View

Overall, the impact of an early election on the market is likely to be concentrated in the short term, and whether it is the election outcome (as demonstrated by Masako Koike’s unexpected victory last October), or its impact on the long-term market, both remain difficult to predict. In our view, the overall macro backdrop for Japanese equities remains constructive: real wage growth is expected to turn positive later in 2026, corporate return on equity continues to improve, and ongoing corporate governance reforms should support shareholder returns. Some of our holdings in the industrial sector could benefit from Koike’s growth policies, while we have selectively allocated to some resilient food staples and retail companies.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1