Dongguan's 'Pork Rong' makes a decade-long IPO comeback: Expands to 3,000 Qian大妈 stores by 'not selling overnight meat'

In the eyes of most people, selling fresh produce is a typical 'tough' business.

This industry is characterized by weak branding, low profit margins, high spoilage, and low entry barriers. After all, consumers can easily access vegetables, meat, and fruits.

However, a leading player in this sector has recently emerged in the capital markets.

On January 12, Qian大妈 International Holdings Limited officially disclosed its prospectus on the Hong Kong Stock Exchange.

For residents of South China, 'Qian Da Ma' is no longer an unfamiliar name.

The slogan 'No overnight meat sold' helped it grow from a small street shop in Guangdong to expand to 3,000 stores within a decade; by 2024, its Gross Merchandise Volume (GMV) reached 14.8 billion yuan, ranking first in China's community fresh produce chain for five consecutive years.

So, when selling vegetables reaches such a scale, can it rewrite the tough business playbook of the fresh produce industry?

Still earning hard-earned money

The Qian Da Ma story began in 2012 at a farmers' market in Dongguan, Guangdong, with founders Feng Jisheng and Feng Weihua starting out in pork retail.

From a business model perspective, similar to most bubble tea shops, reaching thousands of stores usually hinges on one key term: franchising.

According to the prospectus, as of September 30, 2025, Qian Da Ma had 2,938 stores nationwide, of which 2,898 were franchise stores, with only 40 directly operated stores, making the franchise proportion as high as 98.6%.

The advantages of the franchise model are very clear.

The most obvious advantage is that it allows for rapid expansion with light assets, as headquarters almost doesn't bear heavy asset costs like store rent, labor, utilities, etc.

Source: Prospectus

The company’s profit model, similar to how tea brands mark up raw material costs, lies in Qian Da Ma selling vegetables to franchisees, with the core being the supply chain.

According to the prospectus, Qian大妈 currently relies on 16 integrated warehouses, with a total storage area exceeding 220,000 square meters, and dispatches over 800 refrigerated transport vehicles daily on average.

The more franchisees there are, the faster Qian大妈's supply chain 'flywheel' spins. Currently, this portion of income accounts for over 95% of the company’s total revenue.

In addition, similar to tea beverage brands, Qian大妈 also charges franchisees franchise fees, including one-time franchise fees, management service fees, and so on.

Source: Prospectus

In terms of profitability, the prospectus shows that in the first three quarters of 2023-2025, the company achieved adjusted net profits of 116 million yuan, 193 million yuan, and 215 million yuan, respectively.

At first glance, it seems profitable, but a closer look at the financial structure reveals emerging issues.

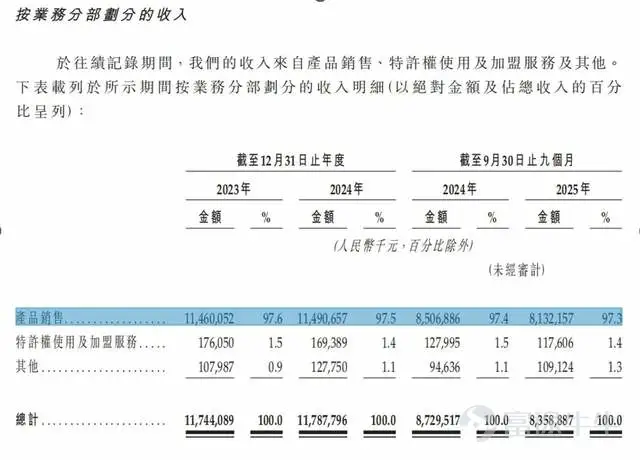

The prospectus shows that in the first three quarters of 2025, Qian大妈's revenue reached 8.359 billion yuan, but the gross profit margin of product sales was only 9%, which slightly improved compared to 2024, but still remains far below the 15%-25% average level of traditional supermarkets.

Therefore, Qian大妈 has yet to escape the dilemma of low gross profit margins in the fresh food sector.

More notably, a significant part of its gross margin improvement comes from an increased proportion of non-fresh categories (such as pre-made meals, cooked foods, and packaged foods). The prospectus also mentions an increase in the sales contribution of products with relatively higher gross margins. In fact, core basic fresh categories like pork and vegetables still have very thin margins.

In other words, Qian大妈's business model, or profit logic, is essentially driven by scale-based 'low-profit high-volume,' rather than efficiency or brand premium.

Once expansion slows down and per-store output declines, profits will immediately come under pressure.

And all of this is built on what appears to be a perfect, but in reality, brutal operating mechanism—"Daily Clearance."

Who pays for the "Daily Clearance"?

One of the core innovative strengths, or perhaps the "foundation" of Qian大妈's success so far, is the "Daily Clearance."

The so-called "Daily Clearance" means that every day at 7 PM, stores offer discounts every half hour (10% off → 15% off → 20% off...), until any remaining products are given away for free at 11:30 PM.

Many consumers choose Qian大妈 for its promise of "freshness."

Through this approach, Qian大妈 not only attracts consumers, but more importantly, reduces the loss rate of fresh produce, significantly improving inventory turnover efficiency.

But who bears the cost? It’s the franchisees.

In fact, Qian大妈 franchisees have almost no pricing power; the discount schedules are enforced by headquarters through a mandatory system, and there are no subsidies for the discounts.

Therefore, in order to meet the "clearance KPI," it’s common for franchisees to sell products at a loss around 8 or 9 PM.

In 2021, CCTV Finance released an exposé titled "CCTV Exposes the Inside Story of Qian大妈 Franchisee Losses, with Some Franchisees Losing 400,000 Yuan in a Year," and the next day, Qian大妈 trended on Weibo.

According to CCTV Finance, the aggressive discounting approach by Qian大妈 has directly led to losses for some franchise stores. Some consumers have developed the habit of deliberately waiting for the discount period to shop, causing the more vegetables the stores sell, the greater their losses become.

In the report, a franchisee stated that as an operator, he has no control over how much stock to purchase or what price to sell at. From the first day of operation, Qian大妈’s brand owner set a minimum limit on daily purchases and strictly restricted the sales prices, only allowing price reductions. If the franchisee does not comply with price management, they face fines or even suspension of supplies. Another franchisee claimed, 'After operating for about a year, the loss reached 300,000-400,000 yuan. I’ve already closed the store and am in the process of shutting it down. Just paying the Qian大妈 company cost me 340,000 yuan.'

Source: CCTV.com

Subsequently, Qian大妈 responded in an official statement that the 'franchisees' poor operations' mentioned in the report are not a widespread issue.

However, judging from the number of stores, this seems to have become a turning point in Qian大妈’s development process.

In fact, according to First Financial, as of October 2021 at its peak, Qian大妈 had opened up to 3,700 stores. Compared to fewer than 3,000 stores now, there has been a significant decline.

Looking at the number of franchisees in recent years, franchisees are indeed fleeing on a large scale.

The prospectus shows that in 2023 alone, 572 franchisees terminated their cooperation; in 2024, 376 were lost; and in the first three quarters of 2025, another 211 were lost. Over three years, a total of 1,159 franchisees have been lost, far exceeding the number of new additions.

Source: Prospectus

More dangerously, the company's performance has shown clear signs of fatigue. Financial data indicates that revenues for the full years of 2023 and 2024 were 11.744 billion yuan and 11.788 billion yuan respectively, almost unchanged; revenue in the first three quarters of 2025 dropped by 4.2% year-on-year to 8.359 billion yuan.

Although it is impossible to view relevant data on Qian大妈’s GMV for 2025, it can be proven that it’s becoming increasingly difficult for Qian大妈 to sell products to franchisees.

The franchisees found it hard to cope, and ultimately returned to the current state of operations.

In summary, the essence of 'the more you sell, the more you lose' is a structural flaw in Qian大妈's business model, which uses 'loss pressure' to achieve scale expansion but passes the cost on to franchisees.

Now, the collective departure of franchisees has become the biggest hidden danger before Qian大妈's IPO, raising questions about whether its so-called scale is merely an illusion.

The real challenge

Having discussed how Qian大妈 generates profits and the current situation of franchisees, from a development perspective, there are still two major problems that Qian大妈 needs to solve.

Problem one: How to break through in the market.

Currently, Qian大妈's stores are mainly concentrated in the southern region. According to the prospectus, in Q3 2025, the southern market contributed 65.9% of revenue, and store density is approaching saturation.

The opening of new stores in the south diverts customer traffic from older stores, while attempts at national expansion have repeatedly failed.

Take Beijing as an example: Qian大妈 entered Tongzhou, Beijing, in December 2020 but withdrew completely after only 13 months.

The core reason lies in northern consumers’ habit of bulk shopping on weekends and stockpiling goods. Additionally, the dry climate makes them less sensitive to 'evening discounts'.

However, for Qian大妈 to enter the northern market, it is not as simple as opening stores; rather, it involves supply chain investment. The company currently operates 16 integrated warehouses, most of which are located in core cities in South China such as Dongguan, Zhongshan, Guangzhou, and Shenzhen. Its supply chain advantage is not present in the northern market.

Conclusion Two: The conflict between low-price consumer perception and profitability needs.

"Freshness + affordability" is the cornerstone of Qian大妈's brand, but in order to maintain its "daily clearance" pricing system, core categories have consistently low profit margins.

In fact, for the majority of ordinary people, sensitivity to pork, egg, and vegetable prices is extremely high. If consumers discover they've purchased overpriced vegetables today, they will switch to other stores downstairs tomorrow.

For Qian大妈 to increase product gross margin and enhance profitability, this can only be achieved by increasing sales of prepared dishes and similar products.

Source: Prospectus

However, these products currently contribute less than 15% to the company’s total revenue and have shown slow growth in recent years, failing to become a major revenue driver.

In other words, Qian大妈 has almost no pricing power in the fresh produce market, caught in the long-term dilemma of losing customers if prices rise or earning minimal profits if they don’t.

Finally, let’s discuss market competition. Grocery shopping is a high-frequency activity, so capital is also eyeing this sector. DingDong has turned losses into profits through refined operations in the Yangtze River Delta, while Hema has built a mid-to-high-end barrier with its "store-warehouse integration" model. Compared to these players, Qian大妈’s digital capabilities are relatively backward, and its supply chain system is slow to respond, which is undoubtedly a weakness in today’s front warehouse-dominated model.

Conclusion

Qian大妈's model is quite representative in China’s community fresh produce industry. It uses "daily clearance" to solve the problem of high spoilage in fresh produce and leverages franchising to drive billions in GMV.

But the real test is now surfacing.

How to reconstruct the profit distribution mechanism amidst a large-scale closure crisis among franchisees? How to break the "South China dependency" and verify cross-regional replication capabilities? And how to escape the low gross margin困境 and build a sustainable second growth curve?

Thus, while everyone says the fresh food business is 'tough going,' it seems that Qian大妈 also struggles to solve this problem.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment