As geopolitical risk premiums fade and Waller turns hawkish, when will precious metals hit bottom?

IPO Preview | Global leader in photovoltaic conductive paste with 27% market share, Juhé Material (688503.SH) targets “A+H” dual listing

As the cost logic of the photovoltaic industry completes a structural shift from 'hoarding silicon as king' to 'reducing silver as key,' and domestic substitution of semiconductor materials enters a critical phase, advanced material companies are facing the dual challenge of upgrading their core businesses while achieving cross-industry breakthroughs.

On January 14, Changzhou Juhé New Material Co., Ltd. (hereafter referred to as “Juhé Material,” 688503.SH), the global leader in photovoltaic conductive silver paste, $Changzhou Fusion New Material (688503.SH)$ officially submitted its listing application to the Main Board of the Hong Kong Stock Exchange, with Huatai International and Jefferies acting as joint sponsors. This company, already listed on the A-share market, is now targeting the “H+A” dual capital platform. In addition to securing funding to strengthen its leading position in the photovoltaic sector, it also aims to build momentum for cross-sector expansion into semiconductor materials.

Global leader in photovoltaic conductive paste, leveraging technological iteration to seize the opportunity for silver reduction

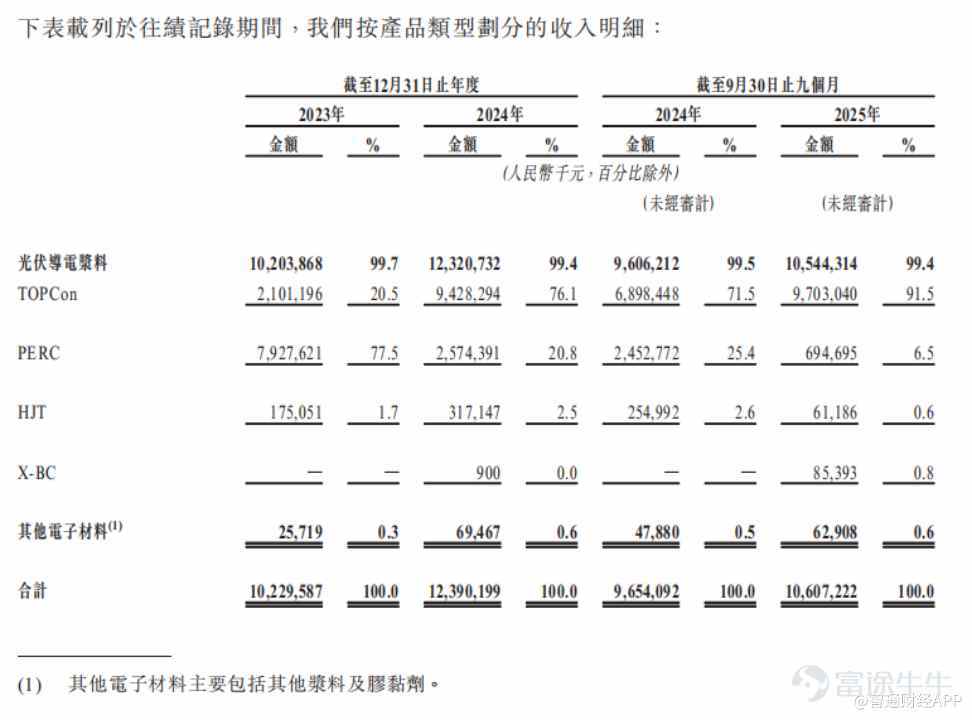

The prospectus shows that Juhé Materials was established in 2015 as a research-driven advanced materials company. Its products mainly include photovoltaic conductive materials and other electronic materials. In the field of photovoltaic conductive paste, Juhé Materials has built a product matrix covering all mainstream technologies such as TOPCon, PERC, HJT, and X-BC. Against the backdrop of N-type batteries becoming the market mainstream, the company's product portfolio is highly aligned with industry trends. By September 2025, revenue from the company’s TOPCon series paste accounted for 91.5% of total revenue. According to CIC Consulting data, for the nine months ended September 30, 2025, the company ranked first globally in sales revenue for photovoltaic conductive paste among all manufacturers, with a market share of 27%.

Behind its leading competitiveness lies the company’s strong R&D innovation capabilities and supply chain integration abilities. In terms of R&D investment, as of September 30, 2025, the company had 236 R&D personnel, accounting for 32% of the total workforce. From 2023 to the first nine months of 2025, the company invested over 2 billion yuan cumulatively in R&D, holding 141 domestic patents and 247 international patents, forming an end-to-end R&D system covering organic material synthesis, formulation design, and manufacturing processes.

Facing cost pressures from the high volatility of silver prices, the company took the lead in developing low-silver and silver-free technological breakthroughs, building a differentiated competitive advantage. In March 2025, silver-coated copper conductive paste achieved ton-scale mass production and began commercial shipments. Pure copper paste for TOPCon and HJT cells has also completed R&D, trial production, and small-batch delivery. For emerging perovskite solar cells, the company is developing ultra-low temperature curing paste and silver-coated copper paste with silver content below 40%.

The company has further strengthened supply chain stability through vertical integration. After acquiring Jiangsu Juyou Silver in 2023, it launched a kiloton-scale industrialization project for electronic-grade silver powder, making it the largest supplier of silver powder among domestic photovoltaic conductive paste companies, achieving autonomous supply of key raw materials. This not only ensures supply chain security but also enhances cost control capabilities. On the production side, photovoltaic conductive paste is mainly produced at manufacturing facilities in Changzhou, Jiangsu Province, and Yibin, Sichuan Province. With annual production capacity exceeding 2,500 tons, it ranks first globally.

In terms of industry potential, the global photovoltaic conductive paste market still exhibits robust growth prospects. According to CIC Consulting, the global photovoltaic conductive paste market size grew from 14.7 billion yuan (RMB) in 2020 to 50.4 billion yuan in 2024 and is expected to increase further to 114.5 billion yuan by 2029, with a compound annual growth rate (CAGR) of 16.2% from 2025 to 2029. Among this, overseas markets, driven by the expansion of photovoltaic production capacity into Southeast Asia, the Middle East, India, and other regions, are becoming significant growth drivers. The market size reached 3.9 billion yuan in 2024 and is projected to grow to 17.4 billion yuan by 2029, with a CAGR as high as 36.3%, providing ample room for Juhé Materials’ global expansion.

Expanding into the semiconductor sector to create a second growth curve

On the foundation of a solid photovoltaic core business, Juhé Materials is extending into the semiconductor materials field through strategic acquisitions, aiming to build a dual-growth engine driven by 'photovoltaics + semiconductors.'

In September 2025, the company announced plans to acquire the blank photomask business of South Korea’s SK Enpulse Co., Ltd. (“SKE”) for 68 billion Korean won (approximately 3.45 billion yuan), further penetrating the semiconductor materials sector and supporting the national strategy for semiconductor self-reliance. According to the prospectus, the acquisition has completed the spin-off of the target assets, establishing a new company, LuminaMask Co., Ltd., with the acquisition expected to conclude in the first quarter of 2026 or around that time. Upon completion, the company plans to build new production facilities in Shanghai to accelerate the localized mass production of blank photomasks.

Juhé Materials stated in its prospectus that this acquisition is a core component of its long-term strategy to become a globally leading advanced materials technology enterprise. It is expected to accelerate the company's strategic layout in the semiconductor field, expanding its business scope beyond conductive paste. To address the growing importance of supply chain autonomy and resilience, this acquisition is expected to drive the localization of high-end semiconductor materials such as blank photomasks, breaking through key bottlenecks in the industry value chain. Additionally, the company aims to leverage the scarcity of the target business and its proven technological advantages to tap into the semiconductor customer base, creating strong commercial synergy with its existing business and product portfolio.

The prospectus shows that photomasks are a core material in the photolithography process, accounting for 13% of semiconductor material costs, making them the third-largest semiconductor material after silicon wafers and electronic specialty gases. In the manufacturing process of photomasks, blank photomasks, as the cornerstone of the upstream industry chain, not only concentrate the most value but also possess extremely high technical barriers. Key indicators such as substrate flatness, film uniformity, and surface defect density directly determine the precision of downstream lithographic pattern transfer, thereby affecting chip process yield and performance. In terms of market space, China's blank photomask market size is expected to reach 2.9 billion yuan in 2024 and increase to 7.6 billion yuan by 2029, with a compound annual growth rate of 25.1% from 2025 to 2029.

Steady business growth but profit pressure persists; liquidity and profitability balance yet to be resolved

In addition to the dual highlights of business layout, the company’s financial fundamentals demonstrate steady revenue growth but emerging profit pressure. On the revenue side, for the fiscal years 2023 and 2024, and the nine months ended September 30, 2025, the company's revenues were approximately 10.23 billion yuan, 12.39 billion yuan, and 10.607 billion yuan, respectively. Growth momentum primarily came from increased demand for TOPCon paste and rising silver prices driving up product selling prices.

On the profitability side, there is a gradual increase in pressure. During the same period, the company's gross margins were 9.2%, 7.8%, and 6.5%, respectively, while net margins dropped from 4.3% in 2023 to 2.2% in the first nine months of 2025. Net profit for the first nine months of 2025 was 234 million yuan, representing a 44% decrease compared to 420 million yuan in the same period last year.

The decline in profitability was mainly influenced by two factors: a significant rise in silver prices, leading to increased costs for core raw materials, and intensified industry price competition, which pressured the downstream photovoltaic sector to cut costs, squeezing profit margins in the paste segment. However, thanks to the 'cost-plus' pricing mechanism and hedging measures like self-supply of silver powder and advancements in low-silver technologies, the company has maintained stable competitiveness for its core products.

In terms of cash flow and debt structure, affected by the unique settlement model in the photovoltaic industry, the company’s operating cash flow remained negative. For the periods 2023 to the first nine months of 2025, net operating cash flow was -2.67 billion yuan, -900 million yuan, and -3.46 billion yuan, respectively. This was mainly due to cash prepayments required for raw material purchases, while customer payments predominantly used bank acceptance bills with credit periods of 30-60 days. To cover working capital gaps, the company relied on financing methods such as discounted bank acceptance bills, with net cash flow from financing activities reaching 3.477 billion yuan in the first nine months of 2025. As of September 2025, total liabilities amounted to 6.81 billion yuan, and the capital-to-debt ratio rose to 58.5%, warranting attention to liquidity pressures.

Moreover, high customer and supplier concentration is a common issue in the industry, and Juhé Materials is no exception. From 2023 to the first nine months of 2025, revenue from the top five customers consistently exceeded 53%, while procurement from the top five suppliers ranged between 60.4% and 86.5%. Major clients included the world’s top ten photovoltaic cell manufacturers. Although the company stabilized supply chains through a “sales-driven procurement” model and long-term cooperation, losing a key client, disruptions in silver powder supply, or sharp fluctuations in silver prices could still significantly impact performance.

Overall, Juhé Materials’ listing in Hong Kong marks a strategic choice amid industry transformation and the trend of domestic substitution. Post “A+H” listing, expanded financing channels will support business expansion and facilitate global deployment.

For investors, three core variables deserve close attention moving forward: First, the commercialization progress and customer certification status of low-silver products like pure copper paste, which directly impacts cost control and profitability improvements. Second, the acquisition progress and integration effectiveness of SKE’s blank photomask business, particularly domestic capacity construction and the development of top-tier wafer fab clients. Third, the ability to improve cash flow conditions by optimizing business structure and broadening financing channels to alleviate liquidity pressures. If these core variables materialize successfully, Juhé Materials could achieve synergistic development across dual tracks, evolving into a diversified leader in advanced materials.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2