Taiwan Semiconductor's strong earnings ignite the US semiconductor sector!

Taiwan Semiconductor's Capex guidance exceeded expectations, and the semiconductor 'bullwhip effect' is being transmitted to the equipment side!

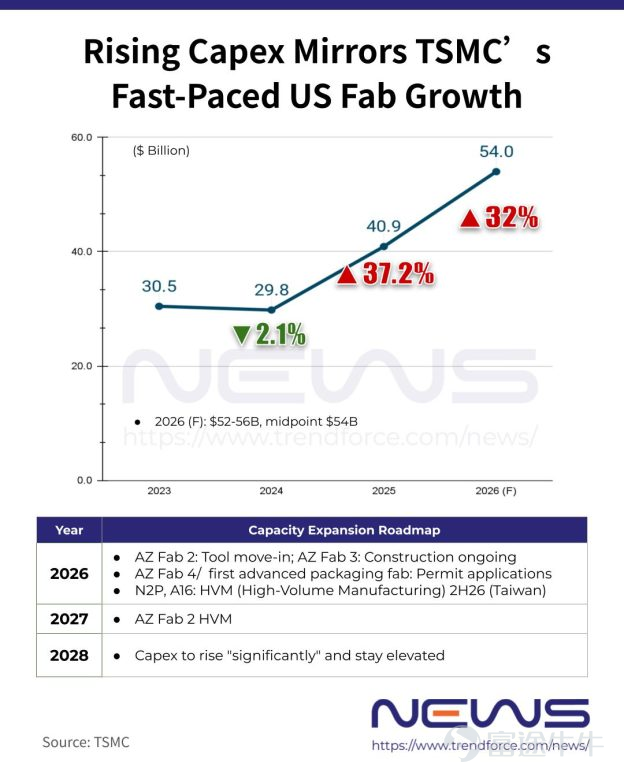

Taiwan Semiconductor, in its latest earnings report, raisedits 2026 capital expenditure forecast to $52-56 billion, and given the continuity of its capacity expansion roadmap, the market has reason to view this round of production expansion as alonger-term investment. This demonstrates Taiwan Semiconductor’s strong confidence in expanding production, and also serves as a typical 'pricing the industry's prosperity with real money' signal.

More importantly, wafer foundry is a typical capital-intensive industry (high depreciation, long payback period), and Taiwan Semiconductor’s management has historically been cautious. They only press the expansion button fully when they believe demand will be more sustainable and order visibility is stronger.

For the equipment sector, this often means:The 'bullwhip effect' is moving from end markets/chip makers, to fab capital expenditures, and then further down to equipment orders and revenue recognition. This article will analyze specific investment logic for the equipment sector based on Taiwan Semiconductor’s Capex allocation ratio.

2026 Capital Expenditure (CapEx) allocation ratio disclosed by Taiwan Semiconductor

70%–80%: Advanced process technologies

10%–20%: Advanced packaging, testing, mask making & others

Approximately 10%: Specialty technologies

A) 70%–80% allocated to advanced process technologies: The main battleground for equipment Alpha lies in 'complexity'

The high proportion of advanced process technologies essentially reflects two things happening simultaneously:Expansion in leading-edge nodes + Continued increase in process complexityThis will shift equipment revenue from 'cycles' to 'intensity' (with more, costlier, and tougher steps required per wafer).

A very 'tradable' conclusion was reached in a research report released by Bank of America on the 12th of this month: by CY26,Process control (metrology/inspection) share rises to 13% of WFE.andCombined etch/deposition share expands to 42%.Driven byNAND, HBM, and 2nm GAAand other structurally more complex processes.

In terms of materials and cleanliness control,The intensity attribute that follows 'advanced degree/yield requirements': The more advanced the node, the more complex HBM/advanced packaging becomes, leading to stricter purity/particle control standards, with higher material and filtration costs often incurred per wafer.

Corresponding beneficiary target:

– Etch/Deposition benefits from both 'share gain + intensity' boost: $Lam Research (LRCX.US)$ 、 $Applied Materials (AMAT.US)$

– Lithography remains important, but near-term focus is on delivery and timing: $ASML Holding (ASML.US)$ It’s still the most direct leverage for advanced process nodes, but research notes that CY26 lithography share might briefly give way, followed by recovery driven by high-NA/low-NA EUV orders.

– Metrology/Inspection (Process Control) priority increased (the more complex it gets, the more testing and inspection are required): $KLA Corp (KLAC.US)$ 、 $Nova (NVMI.US)$

– Advanced materials + micro-contamination control: $Entegris (ENTG.US)$、 $Air Products & Chemicals (APD.US)$

B) 10%-20% allocated to advanced packaging/testing/masks: This is not a trivial segment, but the second growth curve

In$520–560 billionIn CapEx, corresponding toApproximately $52–112 billionthe 'non-front-end core CapEx pool.' This volume is sufficient to change the order curves of multiple sub-sector equipment companies.

Bank of America believesAdvanced packaging has evolved from being 'negligible' to becoming a key driver enabling mainstream semiconductor equipment companies to outperform the broader semiconductor equipment sector; and pointed out that sales related to advanced packaging in the past yearincreased by 22% YoY, approximately twice the overall WFE growth rate. More critically, Bank of America observedstrong growth among process control vendors in relation to advanced packaging (KLAC/NVMI up +85%/+75% YoY for the year), and expects CY26-28 to continue outperforming.

Corresponding beneficiary target:

– The 'hidden winners' of advanced packaging often lie in metrology/inspection (increased packaging complexity = more inspection/metrology points): $KLA Corp (KLAC.US)$ 、 $Camtek (CAMT.US)$ 、 $Onto Innovation (ONTO.US)$ (Increased packaging complexity = more inspection/measurement points)

C) About 10% specialty process: a 'bottom support' for the equipment cycle, but not the main focus of this cycle

About 10% specialty processes (analog, power, MCU, CIS, etc.) indicate:More dispersed, stable demand, but typically less explosive than leading-edgeIt acts more like the 'baseline demand' in the equipment sector, providing some buffer during market volatility, rather than the strongest Beta/Alpha source in this cycle.

Attached is the pre-market performance of the 15-day semiconductor index components:

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

75

227